Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

High-Income Personal Loans for Debt Consolidation and Lifestyle Balance

Table of Contents

- Understanding debt challenges for high-income professionals

- What is a high-income personal loan?

- How personal loans help consolidate debt

- Benefits of using a personal loan for debt consolidation

- Preserving your lifestyle while managing debt

- Key considerations before applying for a personal loan

- How to use a high-income personal loan strategically

- Empowering debt management without sacrifice

- Check your rate

- FAQs

High-income professionals often face a unique financial paradox: despite earning well above the national average, many juggle multiple high-interest debts that limit cash flow and disrupt long-term goals. A debt consolidation loan for high-income professionals offers a practical way to simplify debt, lower total interest, and maintain the lifestyle you’ve worked hard to achieve.

Instead of managing several credit card payments at variable rates, a single unsecured personal loan for debt consolidation can streamline your obligations into one predictable monthly payment—with a clear payoff date in sight.

Understanding debt challenges for high-income professionals

Earnings alone don’t insulate anyone from financial complexity. Between variable income streams and high living costs, even six-figure professionals can face mounting credit card balances and fragmented debt—this, while also navigating rising living costs and economic uncertainty alongside the rest of America.

Collectively, Americans owe a record $1.23 trillion on their credit cards, according to the Federal Reserve Bank of New York, with average interest rates nearing 22%. Well-paid individuals often carry higher-than-average balances because their available credit limits are larger, and their expenses—like travel or family costs—are greater.

When debt is significant, income fluctuations can make it harder to stay on top of payments or stick to a consistent budget month after month.

The emotional toll of complex debt

Debt management can also be an emotionally challenging process A 2023 report by the American Psychological Association found that 63% of adults cite money as a significant source of stress, and debt consistently ranks among the top three financial worries.

Those aged 44 to 64 also say that they worry about money more than both the economy and their health. For high performers accustomed to control and progress, financial stress can spill into professional life and affect decision-making confidence.

When debt starts affecting both your financial and emotional bandwidth, it’s a signal that the system—not you—needs to change. With the right structure (i.e., a single, tailored loan with predictable terms) you can restore clarity and focus.

Read more: Less Stress, More Control: The Emotional Payoff of Debt Consolidation

What is a high-income personal loan?

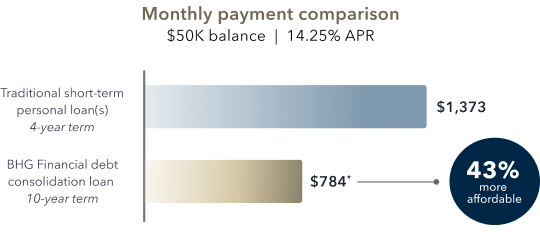

A high-income personal loan is an unsecured loan designed for professionals with strong credit and substantial annual income (typically $100,000+). These loans feature larger amounts and extended repayment flexibility that allow borrowers to manage high-value debts or consolidate multiple obligations more efficiently.

For example, at BHG Financial, qualified borrowers can access loan amounts up to $250,0001 with terms as long as 10 years,1,2 one of the most flexible options in the prime lending space.

Core benefits of a high-income unsecured personal loan include:

- Larger loan amounts: Designed for substantial debt consolidation or liquidity management.

- Predictable payments: Fixed rates and consistent monthly payments simplify planning.

- Extended terms: Choice of repayment lengths, ensuring maximum affordability.

- Flexible use of funds: Use these loans for debt consolidation, cash flow management, major purchases, or other financial needs.

- No collateral required: Protect your assets while securing significant funds.

For busy professionals time and trust matter. That’s why BHG pairs premium loan terms with concierge-level service, handling the heavy lifting while you stay focused on your goals. Approval decisions can happen in as little as 24 hours,3 with funds available in as few as 5 days.3

How personal loans help consolidate debt

Debt consolidation allows you to use one personal loan for consolidating debt to pay off multiple high-interest accounts. Instead of managing several payments with unpredictable rates, you’ll have a single, fixed-rate payment and a clear end date.

This structure not only simplifies your finances but can also lower your total interest costs and free up monthly cash flow. For those with strong credit, consolidating with an unsecured personal loan for debt consolidation also creates opportunities for significant cost savings and improved financial planning.

Plus, most personal loan lenders offer repayment terms ranging from 2 to 10 years, giving you the ability to tailor your payoff periods to match your income patterns and financial goals. Choose shorter terms to minimize total interest paid or longer terms to maintain comfortable monthly payments that preserve cash flow for other priorities.

|

Before consolidation |

After consolidation |

|---|---|

|

Multiple payments due at different times |

One monthly payment |

|

Average APR: about 22% (for credit cards) |

Average APR: about 11% to 15% (for prime credit borrowers) |

|

Revolving credit lines vary monthly |

Fixed repayment schedules |

|

No defined pay-off date |

Clear debt-free timeline |

Benefits of using a personal loan for debt consolidation

1. Lower interest rates compared to credit cards

Credit card APRs have reached near-record highs in recent years. Average personal loan interest rates are roughly half those of credit cards, which often carry rates of 18% to 28% or higher. In contrast, prime credit borrowers can often qualify for personal loan APRs between 11% and 15%.

That difference translates to thousands saved over time—especially for high-income professionals carrying larger debt balances. For example:

|

|

Credit cards |

Personal loan |

|---|---|---|

|

Balance |

$50,000 |

$50,000 |

|

APR |

23.99% |

12.44% |

|

Monthly payment |

$1,233 (variable, 7-year term) |

$894 (fixed, 7-year term) |

|

Total interest paid |

~$53,612 |

~$25,133 |

By consolidating high-interest credit cards into a single fixed-rate loan, you can reduce your total interest cost and move toward debt-free living more methodically.

2. Simplified single monthly payment

High earners often manage multiple financial obligations with different billing cycles. A consolidated loan replaces that complexity with a single manageable payment. This structure:

- Minimizes missed payments and late fees.

- Reduces mental fatigue from juggling due dates.

- Makes it easier to automate repayment.

- Promotes consistent, on-time payments that may positively impact your credit profile.

Predictability also supports better budgeting—especially when your income fluctuates due to bonuses, commissions, or variable business revenue.

3. Predictable fixed payments

Most credit cards have variable rates, meaning your cost of borrowing rises with interest rate increases. A fixed-rate personal loan locks in stability, ensuring your monthly payment stays the same for the entire term.

You can confidently budget for other priorities, knowing exactly what your debt service will cost each month throughout the repayment period.

4. Flexible loan amounts and terms

Large personal loans are better suited to address higher debt balances while providing repayment flexibility that matches your budget.

Lenders typically offer terms from 2 to 7 years, with some specialized personal loans for high-income professionals extending up to 10 years 1,2 (like BHG Financial). This range lets you structure your payments around your current finances or major financial milestones—like saving for your children's college tuition, buying a home, or expanding a business—without compromising cash flow.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* BHG monthly payment based on BHG’s minimum available APR for a 10-year term, which is 14.25% as of 05/13/26 and includes an origination fee. Your actual loan size, loan term, and monthly payment amount may vary based on your individual credit profile and other information provided in your loan application. Terms subject to credit approval.

5. Improved financial planning and cash flow

Lowering your interest rates and extending repayment terms can unlock monthly breathing room, giving you the flexibility to:

- Build an emergency fund

- Contribute more to retirement accounts

- Make strategic investments

By freeing up capital each month, you can pay off debt without sacrificing lifestyle, maintaining the balance that supports your long-term financial health.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Preserving your lifestyle while managing debt

A debt consolidation loan for high-income professionals helps you maintain financial momentum while eliminating high-interest debt strategically. With lower, fixed payments, you can continue investing in your priorities—family, travel, or professional development—without compromising your financial progress.

Avoiding new debt during repayment

Consolidation is most effective when paired with disciplined habits. The goal is to break the cycle of accumulating debt rather than simply moving it around.

Once you pay off your existing high-interest debts with the personal loan proceeds, commit to a realistic budget that limits credit card use to essentials you can pay in full each month. This will likely help decrease your debt-to-income ratio and strengthen your credit profile over time.

This discipline ensures that your consolidation efforts lead to genuine financial improvement rather than temporary relief.

Using consolidation as a foundation for future growth

The savings and structure created through consolidation can become a launchpad for long-term financial goals, such as retirement savings, investment portfolios, or major purchases.

By reducing the cost and complexity of your debt obligations, you create more room in your budget for wealth-building activities that can accelerate your progress toward financial independence.

Read more: Should You Dip Into Savings or Use a Loan?

Key considerations before applying for a personal loan

Creditworthiness and qualification criteria

Lenders evaluate your credit score, income potential, and debt-to-income ratio (DTI) to determine eligibility. The lowest APRs on personal loans are reserved for borrowers with excellent credit, so it's important to understand where you stand before applying.

High-income borrowers often qualify for competitive terms because of their strong financial profile and verifiable earnings. Most lenders prefer lower debt-to-income ratios, but some will still work with borrowers who earn more—even if their ratio is higher.

Understanding loan terms and costs

Carefully review all loan terms and costs before committing to a loan. Before signing, review:

- APR: Includes both interest rate and any fees, providing the most accurate measure of the loan's total cost.

- Loan term: The length of your repayment term impacts the monthly payment and total interest paid.

- Prepayment options: Though rare these days, prioritize lenders who don’t charge prepayment penalties, so you can pay off your loan early and without fees.

- Fast decisions and funding: With BHG, you can receive an approval decision in as little as 24 hours3, with funds delivered in as few as 5 days3—helping you take control quickly and move forward with confidence.

How to use a high-income personal loan strategically

Before consolidating, make a full list of your debts—balances, interest rates, and due dates—and compare total costs before and after consolidation.

Then, prequalify with potential lenders to understand your options without impacting your credit score.4 This initial step provides the information you need to make informed decisions about whether consolidation makes financial sense for your situation.

Next, align your loan offers with your broader financial goals. For example:

- Choose a shorter term (3–5 years) if you want to minimize total interest.

- Choose a longer term (7–10 years) if you prefer lower monthly payments and maximum flexibility.

If you decide to get a personal loan to pay off debt, periodically check in on your progress toensure you’re reducing your debt responsibly, so that you protect your future borrowing power.

In addition, consider connecting with financial advisors who understand the complexities of debt management for high-income professionals and can provide tailored guidance for your specific situation.

Empowering debt management without sacrifice

For professionals who value both progress and balance, a personal loan for high-income professionals offers an effective path to manage debt while maintaining financial stability. You’ve built success through focus and discipline—your financial tools should reflect that same standard.

Consolidation through a trusted partner like BHG Financial delivers:

- Simplified, predictable payments

- Competitive fixed rates

- Unsecured loans up to $250,0001

- Flexible terms up to 10 years1,2

- Concierge-level service from U.S.-based specialists

- Fast funding with minimal paperwork

Ready to explore the possibilities? Use our quick and easy payment estimator to get your personalized loan offer in just seconds.3

Check your rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

High-income personal loan for consolidation FAQs

How does a personal loan simplify debt consolidation?

A personal loan combines multiple high-interest debts into a single loan with one fixed monthly payment, often at a lower interest rate than your existing debts. You’ll have one due date and a defined payoff schedule, making it easier to manage your debt while potentially saving money on interest costs.

What risks should I be aware of when consolidating debt?

The primary risks include the temptation to accumulate new debt on paid-off credit lines and potential fees associated with the consolidation loan. Avoid overspending after consolidation and address the underlying financial habits that lead to debt accumulation.

Additionally, extending your repayment period may result in paying more total interest over time.

What qualifications are needed for a personal loan?

Lenders typically require an excellent credit score (usually 700 or higher), substantial and verifiable income, and a manageable debt-to-income ratio to qualify for a personal loan to secure the best rates. You’ll also need to provide documentation of income, employment history, and existing financial obligations during the application process.

Wil consolidating debt with a personal loan affect my credit score?

Applying for a personal loan may cause a temporary small decrease in your credit score due to the hard credit inquiry. However, successfully consolidating debt and making consistent on-time payments can improve your credit score over time by reducing your credit utilization ratio and demonstrating responsible debt management.

Recommended articles

Debt Consolidation

7 Key Factors That Determine Eligibility for High‑Limit Debt Consolidation Loans

January 12, 2026 | 7 min read

Debt Consolidation

Tax Implications of Debt Consolidation: What High-Credit Consumers Need to Know

February 12, 2025 | 6 min read

Debt Consolidation

How High-Earners Can Use Personal Loans to Manage Large Tax Bills Efficiently

April 2, 2025 | 10 min read

Debt Consolidation

Why the Most Affluent People Avoid High-Interest Debt (And How You Can Too)

April 18, 2025 | 8 min read

Debt Consolidation

When to Pay Credit Card Bill to Increase Credit Score

August 28, 2025 | 7 min read

Debt Consolidation

How Consolidating Debt Can Free Up Cash for Bigger Goals

November 6, 2025 | 6 min read

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 This is not a guaranteed offer of credit and is subject to credit approval.

4 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

No application fees, commitment, or impact on personal credit to estimate your payment.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829