Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

Customized financing to consolidate high-interest debt or fund major purchases or expenses.

About BHG

Programs

Sign in

Personal Loans

Say goodbye to one-size-fits-all funding with a personal loan

Our tailored personal loans adapt to your needs and unlock financial flexibility for life's pivotal moments.

How much are you looking to finance?

No application fees, commitment, or impact on personal credit to check your rate.

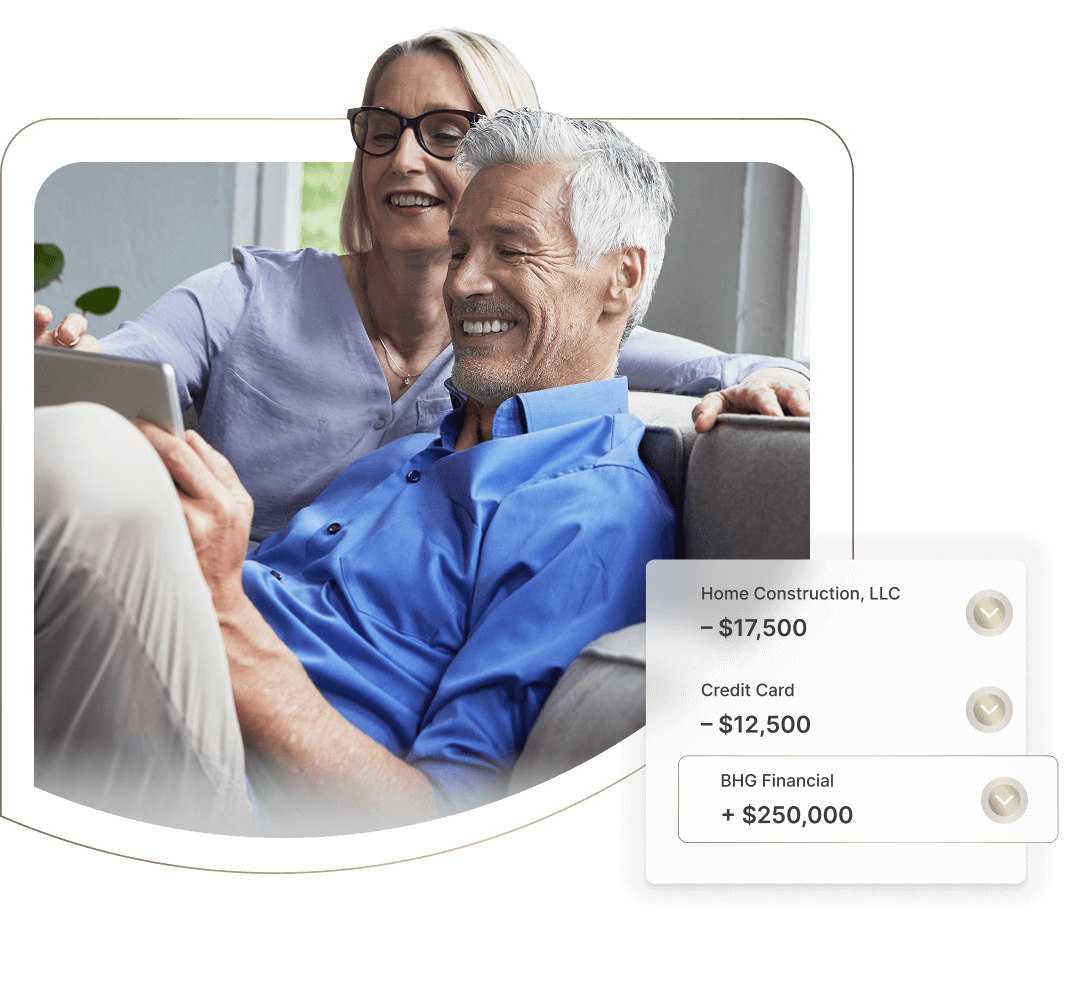

Image is an example only and does not reflect actual customer information.

WHY CHOOSE BHG FOR A PERSONAL LOAN

-

Large loan amounts up to $250K1

-

Fixed payments up to

10 years1,2

-

Fast funding in as few as

5 days3

-

U.S.-based loan

concierge service

Experience the BHG Financial Difference

One loan for all your financial goals

At BHG Financial, we're committed to supporting you throughout your financial journey with tailored personal financing to experience all of life's milestones.

-

Large amounts: Finance multiple goals with up to $250,0001

-

Flexible funds: Use the loan your way

-

Customized offers: Choose the best offer and term for you

|

|

Max loan amount |

Max term |

|---|---|---|

|

$250,0001 |

120 months1,2 |

|

SoFi |

$100,000 |

84 months |

|

LightStream |

$100,000 |

84 months |

|

Upstart |

$75,000 |

60 months |

|

LendingClub |

$60,000 |

84 months |

|

Discover |

$40,000 |

84 months |

SOURCE: Discover, NerdWallet - Accessed on 03/01/26

Yearly Savings Comparison Example

Based on a loan for $50,000 (with an APR of 14.25%)

Traditional Loan

Term (60 mo)

$1,170/mo

BHG Financial

Max Term (120 mo)

$784/mo*

Yearly Savings

(monthly payments)

$4,632

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* BHG monthly payment based on BHG’s minimum available APR for a 10-year term, which is 14.25% as of 05/13/26 and includes an origination fee. Your actual loan size, loan term, and monthly payment amount may vary based on your individual credit profile and other information provided in your loan application. Terms subject to credit approval.

Your finances—simplified

By taking advantage of our fixed rates and extended repayment terms1, you can reduce your payments and free up funds to accomplish your personal goals.

A HASSLE-FREE PROCESS

How our debt consolidation personal loans work

As a busy professional or business owner, your time is valuable. At BHG Financial, we’ve streamlined the application process to get you funded fast3 so that you can get back to business.

01

Start an application

Unlike other lenders, we won't ask for unnecessary paperwork. It’s easy and there’s no impact to your credit score to apply.4

02

Get a funding decision

Approval decisions can take as little as 24 hours.3 A dedicated finance manager will review your application and qualifications, tailoring a loan solution for your financing needs.

03

Receive funds fast

If approved, you will receive your funds in one lump sum in as few as 5 days.3

LEARN MORE

Personal loans FAQs

A personal loan is financing provided by a lender (such as an online financial services provider, a bank, or a credit union) that is intended to cover personal expenses and must be paid back over a predetermined period.

BHG Financial personal loans provide loan amounts up to $250,0001 and extended terms up to 10 years,1,2 making monthly repayment options affordable to fit your lifestyle.

A personal loan is intended for personal use. Examples include consolidating personal credit card debt, improving your home, planning for a family, or covering other personal major purchases.

Applying for our personal loans will not impact your personal credit.4 We only perform a soft pull of your credit when you apply, so your score will remain intact. At the funding stage, we will perform a hard credit inquiry, which may affect your credit score.

BHG Financial Personal Loans have fixed APRs, meaning that your monthly payments will remain the same throughout the repayment period.

Yes, BHG Financial gives you the flexibility to add a co-borrower at the beginning of the application or during the application process.

To apply for a personal loan from BHG Financial, you'll typically need a minimum credit score of 640 and a minimum annual income of $100,000. However, credit score is not the only factor included in approval decisions.

BHG Financial’s personal loans are unsecured loans. You do not need to provide personal collateral in order to secure funding.

Credit cards come with an annual percentage rate (APR) that is generally higher than the APR of a typical personal loan. Additionally, credit card APRs are usually variable, increasing during economic downturns and having a substantial effect on your budget.

Consolidating your personal credit card debt with BHG Financial’s personal loan can provide you with a fixed APR and a predictable, low monthly payment, saving you money in the long run.

BHG Financial offers an online payment calculator, which you can use to view your offers in seconds with no impact to your credit score.4

At this time, BHG does not offer a direct-to-creditor payment option.

25+ years

Lending experience

A+ Rating

Better Business Bureau

$28 Billion+

Loans funded

CUSTOMER TESTIMONIALS

Why professionals choose us

“BHG catered to my small business needs. The process was easy, and the team was highly responsive. ”

Eric C., BHG Customer

January 2025

“BHG consolidated my personal debt under one monthly payment. I wish I would’ve applied sooner!”

Imeldo A, BHG Customer

October 2024

“I’ve had experience with many lenders, and BHG stood out for their exceptionally organized and expeditious process. ”

Garrett H., BHG Customer

January 2025

“BHG provides tailored financing for small business owners, prioritizing time, integrity, and results.”

Michele C., BHG Customer

December 2024

See real offers fast

There is no cost, commitment, or impact on personal credit to view your loan offer.4

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

Annual percentage rates (APRs) for personal loans range from 6.49% to 28.89%, with terms from 2 to 10 years.

3 This is not a guaranteed offer of credit and is subject to credit approval.

4 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

Testimonial(s) based on unique customer experience. Individual customer experiences may vary.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

IMPORTANT INFORMATION ABOUT ESTABLISHING A NEW CUSTOMER RELATIONSHIP

To help the government fight the funding of terrorism and money laundering activities, Federal law requires all financial institutions to obtain, verify and record information that identifies every customer. What this means for you: When you apply for a loan, we will ask for your name, address, date of birth, social security number and other information that will allow us to identify you. We may also ask to see your driver's license or other identifying documents. If all required documentation is not provided, we may be unable to establish a customer relationship with you.