Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

Customized financing to consolidate high-interest debt or fund major purchases or expenses.

About BHG

Programs

Sign in

Personal Loan for Debt Consolidation

Manage high-interest debt with a debt consolidation loan

We provide tailored financing to help you consolidate existing personal loans and high-interest credit cards.

How much are you looking to finance?

No application fees, commitment, or impact on personal credit to check your rate.

Image is an example only and does not reflect actual customer information.

Why Choose BHG for A Personal Loan

-

Large loan amounts up to

$250K1

-

Fixed payments up to

10 years1,2

-

Fast funding in as few as

5 days3

-

U.S.-based loan

concierge service

Seamless Experience

Financial self-care means paying off high-interest debt

Paying off debt can be challenging—we can make it easier. We provide flexible debt consolidation loans with minimal paperwork and no personal collateral requirements.

|

|

|

Balance transfer credit card |

|---|---|---|

|

Balance transfer fee |

N/A |

Up to 5% of transfer amount |

|

Amount |

Up to $250,0001 |

May be capped to 75% of total credit limit |

|

Rate changes |

Fixed rate |

Rate will likely go up after intro period expires |

|

Type of debt transferrable |

Applicable to all unsecured high-interest debt |

Only applicable to credit card debt with some issuers |

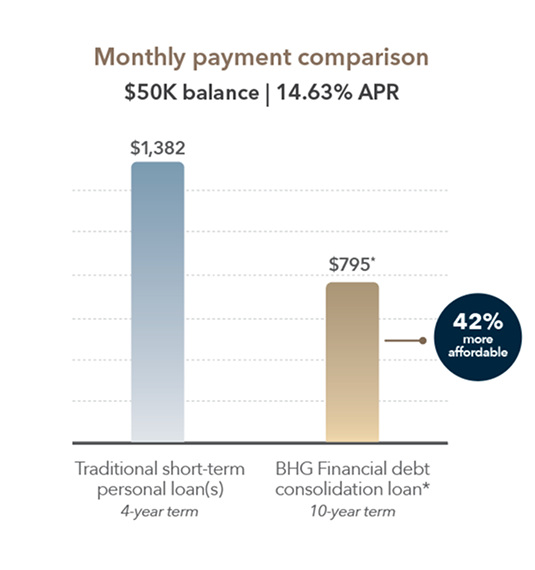

SOURCE: Bankrate, Investopedia, Accessed on 03/14/25

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

*BHG monthly payment based on APR of 14.63% as of 11/01/25 and includes an origination fee. Your actual loan size, loan term, and monthly payment amount may vary based on your individual credit profile and other information provided in your loan application.

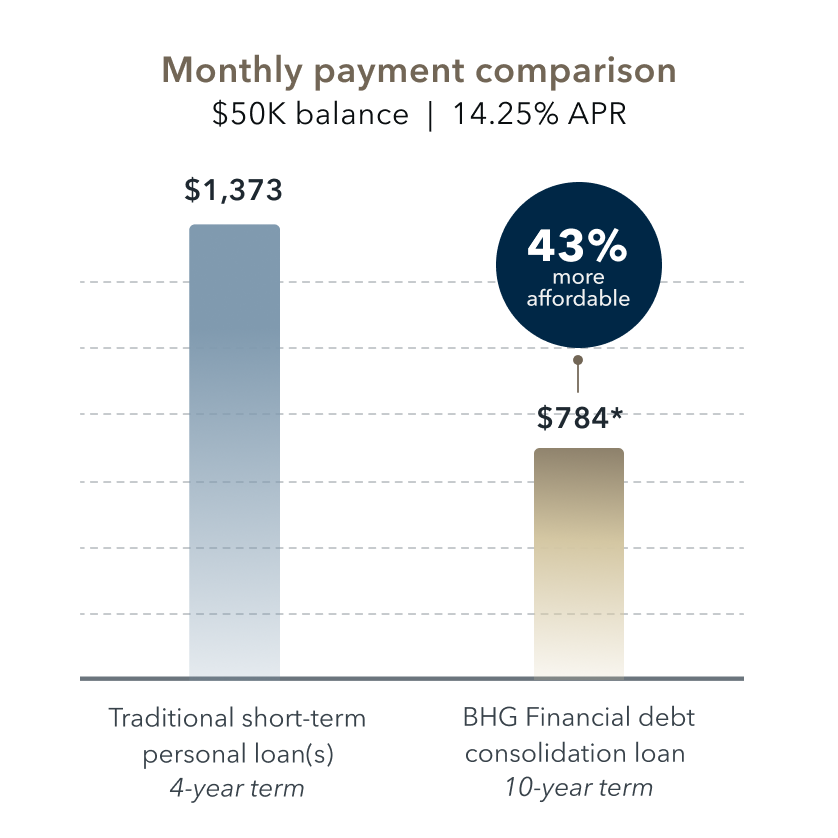

Terms subject to credit approval.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* BHG monthly payment based on BHG’s minimum available APR for a 10-year term, which is 14.25% as of 05/13/2026 and includes an origination fee. Your actual loan size, loan term, and monthly payment amount may vary based on your individual credit profile and other information provided in your loan application. Terms subject to credit approval.

Your finances—simplified

Consolidate multiple debts into a new loan with better terms, including a fixed rate, a flexible repayment period1, and one low monthly payment.

-

Instant offers: If approved, see personalized loan offers in seconds 3

-

Debt payoff: Eliminate high-interest credit card debt

-

Low payments: Reduce the cost of debt and boost your budget with up to 10 year repayment terms 1,2

A HASSLE-FREE PROCESS

How our debt consolidation personal loans work

As a busy professional or business owner, your time is valuable. At BHG Financial, we’ve streamlined the application process to get you funded fast3 so that you can get back to business.

01

Start an application

Unlike other lenders, we won't ask for unnecessary paperwork. It’s easy and there’s no impact to your credit score to apply.4

02

Get a funding decision

Approval decisions can take as little as 24 hours.3 A dedicated finance manager will review your application and qualifications, tailoring a loan solution for your financing needs.

03

Receive funds fast

If approved, you will receive your funds in one lump sum in as few as 5 days.3

LEARN MORE

Debt Consolidation Personal Loan FAQs

Yes, you can get a personal loan to consolidate debt. We offer Debt Consolidation Loans with affordable monthly payments.

Debt consolidation is the process of combining multiple debts into one new loan. This new loan and its APR replace the original debts. Our debt consolidation loans give borrowers peace of mind by providing one affordable monthly payment that’s easy to manage.

Many lenders require a certain credit score for applicants to be approved for funding, and this minimum score varies by lender.

At BHG Financial, the minimum credit score needed to apply is 640. We also look at additional attributes beyond your score to assess your financial situation and help you find the right financial solution for your needs. However, credit score is not the only factor included in approval decisions.

Yes. Qualified borrowers may use a BHG Financial personal loan for debt consolidation. Consolidating multiple balances into a single fixed monthly payment may simplify your finances—especially if your existing debts carry higher or variable interest rates, and you qualify for a lower fixed rate. Find out if you qualify for a debt consolidation loan through BHG Financial.

Debt consolidation through a personal loan can simplify your debt into a single fixed monthly payment. This can be beneficial if the interest rate(s) of your previous debt was high and/or variable.

Personal debt consolidation loans may impact your personal credit during the initial credit inquiry that the lender performs following your application or before funding. In any case, if you keep up with your monthly payments, you could build up your credit over time.

At BHG Financial, your credit score will not be impacted during the application process.4

Typically, debt consolidation loans will stay on your credit report for seven years. As long as the account is reported to the credit bureaus, it will remain on your report.

At BHG Financial, we only perform a soft pull of your credit when you apply, so your score will remain intact.4

25+ years

Lending experience

A+ Rating

Better Business Bureau

$28 Billion+

Loans funded

CUSTOMER TESTIMONIALS

Why professionals choose us

“BHG catered to my small business needs. The process was easy, and the team was highly responsive. ”

Eric C., BHG Customer

January 2025

“BHG consolidated my personal debt under one monthly payment. I wish I would’ve applied sooner!”

Imeldo A, BHG Customer

October 2024

“I’ve had experience with many lenders, and BHG stood out for their exceptionally organized and expeditious process. ”

Garrett H., BHG Customer

January 2025

“BHG provides tailored financing for small business owners, prioritizing time, integrity, and results.”

Michele C., BHG Customer

December 2024

See real offers fast

There is no cost, commitment, or impact on personal credit to view your loan offer.4

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

Annual percentage rates (APRs) for personal loans range from 6.49% to 28.89%, with terms from 2 to 10 years.

3 This is not a guaranteed offer of credit and is subject to credit approval.

4 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

Testimonial(s) based on unique customer experience. Individual customer experiences may vary.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

IMPORTANT INFORMATION ABOUT ESTABLISHING A NEW CUSTOMER RELATIONSHIP

To help the government fight the funding of terrorism and money laundering activities, Federal law requires all financial institutions to obtain, verify and record information that identifies every customer. What this means for you: When you apply for a loan, we will ask for your name, address, date of birth, social security number and other information that will allow us to identify you. We may also ask to see your driver's license or other identifying documents. If all required documentation is not provided, we may be unable to establish a customer relationship with you.