Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Stretch the Term, Shrink the Stress: Why Longer Loan Terms Can Make Sense

Table of Contents

- The common misconception about longer loan terms

- The math behind longer terms and lower stress

- When choosing a longer loan term makes strategic sense

- BHG’s Personal Loan: Designed for flexibility and financial strategy

- Don’t just look at the interest—look at the outcome

- Ask yourself: Is a longer loan term right for you?

- Final thought: Flexibility now creates freedom later

- Check my rate

When you’re considering a personal loan, the instinct is often choosing the shortest possible term to minimize interest. But focusing only on total interest paid can overshadow a more important factor: your monthly liquidity.

Choosing longer personal loan terms is an intentional move that protects your cash flow and supports your long-term momentum. A personal loan for high-income borrowers should work with your goals—not against them.

Key TAKEAWAY

A longer personal loan term can provide significantly lower monthly payments, giving you the financial space to manage high-interest debt, invest in higher-return opportunities, and keep your broader wealth-building plans on track.

The common misconception about longer loan terms

Yes, you may pay more in interest over time—but that’s not the whole picture

It’s true that stretching a loan over a longer period means you will pay more in total interest. This is the figure that most traditional lenders emphasize. But for high earners with complex financial priorities (i.e., simultaneously contributing to retirement, supporting aging parents and adult children, and managing strategic debt), the real challenge is monthly liquidity.

By locking up a significant portion of your monthly income into a higher, short-term payment, you might reduce your total loan cost, but you also severely limit your available cash. This pressure can force you to use up savings, pause critical investments, or even take on new short-term, high-interest debt when an unexpected expense arises.

For high earners, monthly flexibility often matters more

If you earn a substantial income, the question usually isn’t whether you can make the payment; it’s what else you could be doing with the money.

By choosing a longer personal loan term, you deliberately free up monthly capital that you can redirect toward other, more significant financial priorities like:

- Building more cash reserves

- Having capital available to seize a timely investment opportunity

- Funding college tuition, childcare, and/or healthcare costs

- Maintaining liquidity to manage large tax bills or fluctuations in income

And if you’re among the millions of Americans simultaneously supporting children and aging parents, this type of flexibility can be the difference between stress and control.

Read more: The Sandwich Generation: Balancing Family, Finances, and the Future

The math behind longer terms and lower stress

How monthly payments shrink when you stretch the term

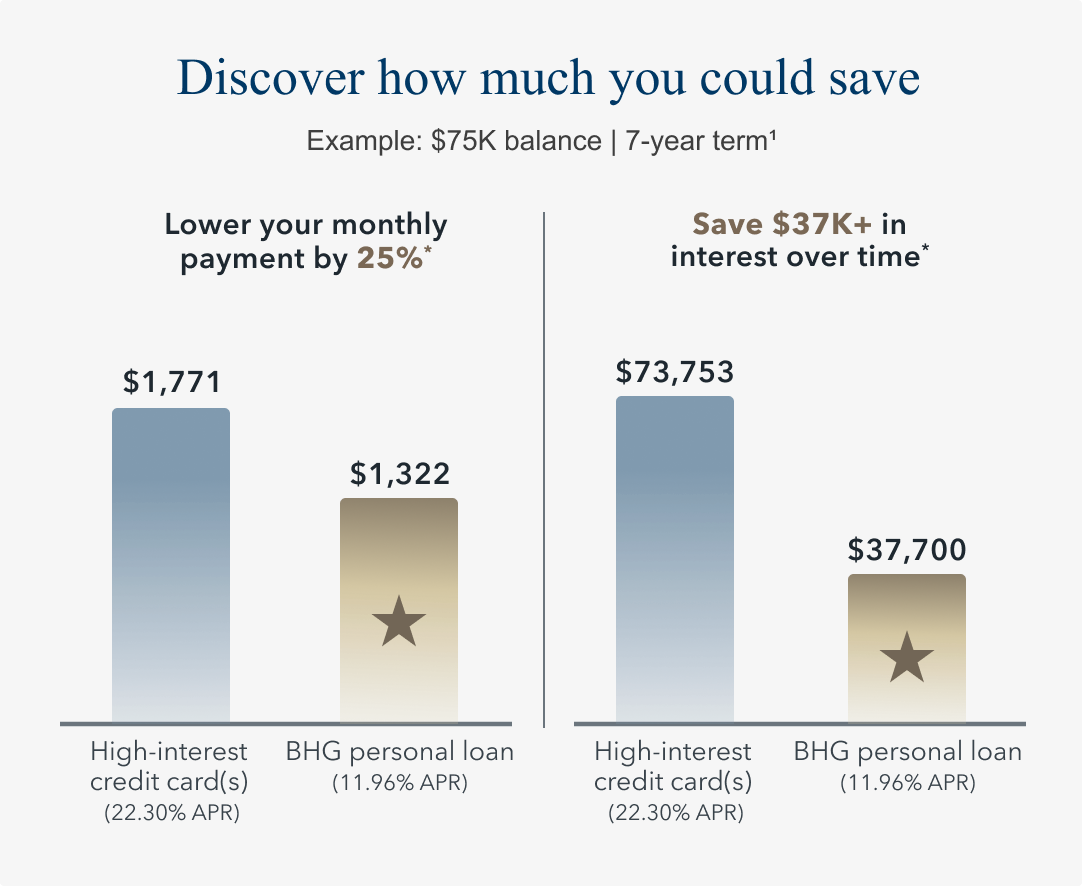

Stretching your repayment period is a smart long-term strategy designed for control over your monthly finances. Here’s an example of your monthly obligations for a $75,000 personal loan with a 12.44% APR:

- 3-year term1: $2,507 per month

- 7-year term1: $1,342 per month

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $75,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,771 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $1,322 and minimum available APR for a 7-year term, which is 11.96% as of 05/13/26 and includes an origination fee.

The “opportunity cost” concept

Opportunity cost is the value of what you give up when you choose one option over another (i.e., what you could do with your money if it weren’t tied up in a high monthly payment).

For high earners, this matters because every dollar of freed-up cash flow can be redirected toward something with a higher return, such as retirement contributions or strategic investments.

In the example above, choosing longer personal loan terms gives you more than $1,000 per month that can be invested, saved, or used to strengthen your liquidity, rather than locking it into an aggressive repayment schedule.

The psychological value of margin

Beyond the measurable financial benefits, adding a monthly payment buffer provides invaluable emotional relief. High earners, despite their success, often feel significant financial pressure—money is still the top source of stress for U.S. adults, after all.

Lower monthly payments reduce that daily pressure, leading to greater peace of mind and supporting better, more rational financial decision-making. When you feel in control, you stop simply reacting to your debt and start proactively managing your financial future.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

When choosing a longer loan term makes strategic sense

Not everyone benefits from stretching a loan term. However, for many high-income professionals, there are specific circumstances in which a longer term makes financial sense.

You’re carrying high-interest credit card debt

The Federal Reserve reports that credit card interest rates are averaging about 21% to 22%. Carrying high-rate debt can drain cash flow quickly, especially when you’re juggling multiple balances. A personal loan for high-income borrowers allows you to replace high, variable-rate debt with a predictable, fixed-rate payment.

Strategic consolidation can also have a positive impact on your credit score by reducing your credit utilization ratio and improving your future borrowing power.

You’re planning a large financial move

By opting for a longer term, you keep your monthly overhead low, freeing up flexible capital for higher-priority expenses with a greater potential return. This allows you to make smart, intentional financial decisions that enhance your standing while preserving your cash reserves.

You’re experiencing cash flow strains

A longer personal loan term is a smart way to manage your monthly budget. You get the immediate benefit of paying down high-interest debt while keeping more cash readily available for unexpected expenses or everyday costs of living.

This helps you avoid the strain of aggressively paying off loans and allows you to maintain balance, even during periods of economic uncertainty where inflation is affecting borrowers across every income bracket.

BHG’s Personal Loan: Designed for flexibility and financial strategy

High loan amounts + longer terms = Better options

We offer one of the largest unsecured loans for qualifying clients—up to $250,0001—paired with one of the industry’s most flexible loan terms, up to 10 years.1,2 This combination is ideal for consolidating large balances or managing multiple obligations at the same time.

FYI: Credible named BHG Financial the best large debt consolidation loan because we offer one of the largest loan amounts in the industry—up to $250,000.1 This allows prime borrowers to access their full requested amount or more1 to consolidate debt and handle major expenses—fulfilling multiple goals at once.

Tailored for professionals with strong credit and ambitious goals

BHG’s personalized, data-driven underwriting goes beyond a simple credit score. We understand that your professional history, income streams, and financial goals create a broader picture of your creditworthiness.

That’s why we offer longer-term loan structures that give high earners the control and flexibility they need to manage complex finances with confidence.

Prequalification with no credit impact

We respect your time and your credit. You can estimate your monthly payment and prequalify for a personal loan for high-income borrowers in just seconds.3 Your credit score stays protected until you choose to move forward.4

If approved, a funding decision can be made in as little as 24 hours,3 and you can receive your funds in one lump sum in as few as five days.3 Our concierge-style, U.S.-based loan specialists are available around your busy schedule to do the heavy lifting.

Don’t just look at the interest—look at the outcome

Interest alone doesn’t define the right loan. When designing your loan term strategy, consider the full picture, including cash flow, stress reduction, and opportunities to advance your financial goals.

|

|

Shorter term |

Longer term |

|---|---|---|

|

Interest paid |

Lower total interest |

Higher total interest |

|

Monthly stress |

Higher pressure due to larger payments |

Lower pressure thanks to more manageable payments |

|

Financial flexibility |

Limited monthly liquidity |

More breathing room and cash flow |

|

Impact on goals |

Can strain other financial priorities and reduce the ability to capitalize on opportunities |

Frees capital to invest, save, or fund strategic opportunities, supporting long-term planning |

FYI: BHG’s U.S.-based loan concierge team will guide you through your options and help you identify a loan structure that works for you.

Ask yourself: Is a longer loan term right for you?

A longer term is often an advantage for borrowers who value cash flow, stability, and strategic planning. Ask yourself:

- Do you have a high income but limited liquidity month-to-month? If you often feel financial pressure despite your earnings, more breathing room may help.

- Are you carrying large balances and juggling multiple goals? A consolidation loan, combined with a longer term, can free up your budget and simplify your life.

- Would lower payments reduce stress and open new opportunities? If reduced pressure helps you invest, save more, or support your family, you may be lacking financial peace of mind.

If you answered yes to any of these, a longer-term personal loan may be the exact solution you need to regain control of your finances.

Final thought: Flexibility now creates freedom later

Stretching the term isn’t about dragging out debt—it’s about designing a smarter repayment plan that fits your goals, lifestyle, and long-term ambitions.

See how a BHG personal loan with a longer term1 can reduce your stress and maximize your strategy. Prequalify in minutes,3 with no impact to your credit score.4

Check your rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 This is not a guaranteed offer of credit and is subject to credit approval.

4 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829