Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

6 Financial Blind Spots for High-Earners (and How to Fix Them)

Table of Contents

- The hidden risk of being a high earner

- Blind spot #1: Assuming high income means you don’t need a plan

- Blind spot #2: Underestimating debt’s drag on your wealth

- Blind spot #3: Overconfidence in financial knowledge

- Blind spot #4: Thin or nonexistent emergency savings

- Blind spot #5: Neglecting retirement and your “future self”

- Blind spot #6: Misunderstanding your true net worth

- 10-point financial blind spot audit: A checklist for high earners

- Check my rate

- Know what you’re really worth

Sarah, a successful mid-career professional, earns over $200,000 a year, drives a nice SUV, lives in a desirable neighborhood, and vacations semi-regularly. But when she stops to actually add up her finances—credit card balances, outstanding student loans, her mortgage, ongoing renovation expenses—she’s shocked at how little cash flow remains. On paper, she appears “affluent.” In reality, she’s just keeping up.

This disconnect is the hallmark of a financial blind spot: areas of your finances you assume are fine but have never truly measured or managed. Many people have them, but for high earners with larger responsibilities, higher taxes, and more at stake, these blind spots can be even more costly—unless you learn how to spot them early.

In this article, we break down the six most common blind spots affecting high-income professionals: what they are, why they matter, and the steps you can take to fix them before they limit your long-term wealth.

For high earners, financial blind spots are especially dangerous. Why? Because the more you make, the more complex your financial responsibilities—larger bills, variable bonuses, higher debt obligations, and greater tax exposure. Without intentional management, it’s easy to overestimate stability while underestimating risk.

The true state of six-figure finances reveals a confidence gap

A false sense of security due to substantial earnings can mask serious gaps, such as not knowing your true net worth, total debt, or whether you’re saving enough for retirement.

Recent research shows financial confidence is declining nationwide:

- BHG Financial’s 2026 Consumer Debt & Finances Survey shows that while 80% of high‑income Americans feel optimistic about their financial future, nearly two in five still say they’re likely to miss a debt payment in the next six months—highlighting a gap between confidence and cash‑flow reality.

- In 2025, only 70% of Americans felt confident they could support the lifestyle they want, and just 61% felt confident about meeting their retirement savings goals—both figures trending downward since 2020, according to an Allianz retirement study.

- Despite this uncertainty, only 41% of Americans work with a financial advisor, per Gallup polling, even though guidance becomes more valuable as income and financial responsibilities grow.

- This lack of structured planning may help explain why financial optimism continues to fade: in April, Gallup found that just 44% of Americans rated their finances as excellent or good, while a record 53% said their situation is getting worse.

If these trends reflect the general population, the risks run even deeper for high earners, whose blind spots often carry larger dollar consequences and leave them even more exposed.

Blind spot #1: Assuming high income means you don’t need a plan

It’s tempting to believe that a high salary will eventually fix any financial challenge (“I earn a lot, so I can spend, save, and invest without planning every detail”). But income alone rarely fixes poor structure. Without a clear plan, irregular income (like bonuses), unpredictable expenses, and untracked spending can chip away at long-term wealth faster than expected.

The Allianz survey found that nearly half of U.S. adults still don’t have a written financial plan, and BHG data reveals that 65% of Americans say today’s economic conditions make financial decisions harder.. When you’re not tracking goals or progress, it becomes easy to overspend, under-save, or make decisions that conflict with long-term priorities.

What this looks like in real life

- No written, measurable financial goals

- Unsure of annual savings rate

- Unable to quickly state net worth or debt totals

Depending on your profession, these signs may be amplified by erratic work hours, delayed bonus payments, cyclical revenue, or student-loan burdens, which can make it harder to plan your finances.

How to fix it

Having a plan makes it easier to commit to responsible, consistent money habits.

- Create a one-page financial plan outlining your 1-, 5-, and 10-year goals. Include target savings rates, debt payoff priorities, and projected net worth.

- Work with a financial advisor, planner, or use digital planning tools for more complex situations (e.g., tax planning, investments, multiple income streams, or equity compensation).

- Commit to quarterly “wealth reviews” just as you would professional performance reviews. Check in on your progress, adjust goals, and stay accountable.

Blind spot #2: Underestimating debt’s drag on your wealth

Many six-figure earners often carry large balances on credit cards and other forms of financing, usually to improve their financial situation without compromising their liquidity. According to BHG Financial, 13% of high‑income Americans say credit card debt is their largest expense, and nearly one in three used credit cards to cover essential living expenses during a financial shortfall.

Whether this use is strategic or necessary, high APRs make it expensive: interest rates in the 20% range can severely slow wealth accumulation and redirect money that could otherwise fuel long-term investing, saving, or wealth-building strategies.

To put it into perspective, you may put a family vacation on a credit card to split the cost over time. Accounting for interest, a $10,000 dollar vacation could easily morph into a $12,000-15,000 vacation. It may seem small, but that’s thousands of dollars that could have been used to build your wealth. It’s important to look at the big picture to see how debt can drag you down in the long run.

How to spot this blind spot

Watch out for:

- Multiple credit cards with balances and different due dates

- Card balances increasing over time

- Making only minimum payments rather than paying extra

- High utilization rates despite healthy income

- Difficulty tracking total monthly interest costs

If you don’t know exactly how much you pay in interest each month—or can’t easily calculate how long it will take to pay off the balances—you may be underestimating how much debt is draining your financial growth. Minimum payments won’t make a dent in your credit card debt balances, even if you stop using them. It can take as much as 30 years to pay off credit cards making only the monthly payment.

Debt consolidation as a smart fix for high earners

For high-income professionals juggling multiple high-interest debts, consolidation can turn several costly payments into one predictable payment with a structured schedule.

Debt consolidation means combining multiple debts (credit cards, other personal loans, student loans, etc.) into a single fixed-rate loan—ideally with lower interest and a set payoff schedule.

A BHG Financial personal loan offers qualified borrowers a solution for consolidating high-interest credit card or personal loan debt into a more affordable, fixed monthly payment.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

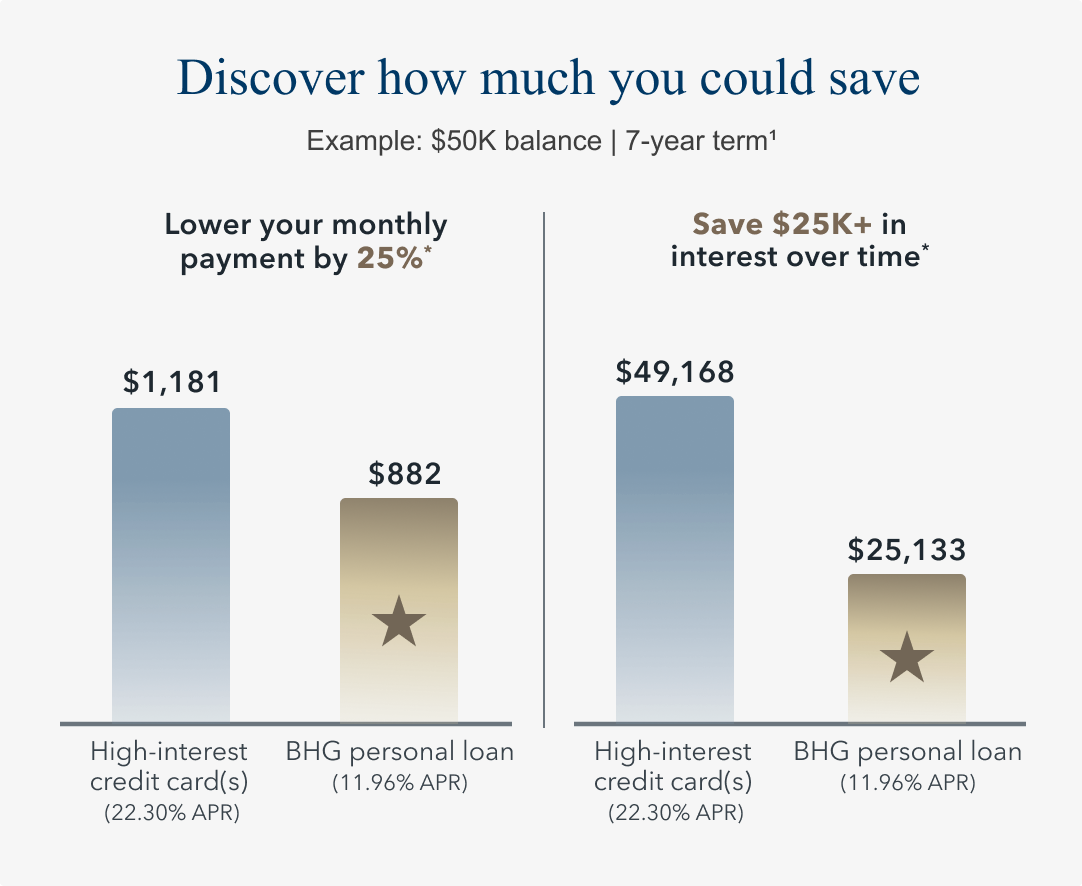

* Potential savings based off comparing repayment of a $50,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,181 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $882 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

Check your rate to determine whether consolidating your existing debt into a BHG personal loan could reduce interest costs and free up cash to deploy toward savings or investments. There’s no impact to your credit2 to explore debt consolidation loan offers.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Blind spot #3: Overconfidence in financial knowledge

Many assume that professional expertise naturally translates into financial know-how. But managing money requires a different skill set. BHG Financial research reveals that confidence doesn’t always equal clarity: while 78% of respondents say they have good credit, half incorrectly believe income affects credit scores, and nearly a quarter misunderstand how shared credit works.

Pew Research reports that only 45% feel confident creating an investment plan. That gap between perceived and actual knowledge can lead to costly mistakes.

Overconfidence—or even a lack of confidence—can affect how well you diversify, assess risk, protect your income, or plan for the future, making it one of the most costly blind spots.

Reality check: Where knowledge often falls short

Without proper planning and ongoing education, it’s easy to underestimate risks that affect long-term financial stability:

- Long-term retirement income planning: Failing to account for inflation, taxes on withdrawals, or rising healthcare costs may result in running out of money sooner than expected or needing to work longer than planned.

- Risk management: Inadequate insurance (i.e., life, disability, umbrella) or a lack of estate planning can leave your income, dependents, and assets vulnerable during emergencies.

- Tax optimization: Failing to structure compensation, deductions, retirement contributions, or business expenses efficiently can cause you to pay more taxes than necessary.

How to turn confidence into informed action

- Get periodic second opinions from a trusted financial professional experienced in optimizing complex portfolios.

- Use checklists to systematically evaluate your asset diversification, tax efficiency, and insurance coverage.

- Invest in reputable educational resources and avoid relying solely on peers or social media for financial advice.

Blind spot #4: Thin or nonexistent emergency savings

Not all six-figure earners have liquid cash reserves. In fact, many high earners under-save, relying instead on future income, bonuses, or the belief that “I can always earn more.” But this mindset can be risky.

While 73% of high-income Americans believe they have sufficient emergency savings (three to six months of expenses), 26% have less than $10,000 across their bank accounts, BHG found. Forty-four percent of all respondents said they don’t have enough saved to cover a major unplanned expense, such as an emergency surgery or home repair.

Why this is especially risky for high earners

High-earning households typically have higher fixed costs, which means a short disruption (loss of income, medical emergency, large home/auto repair) can be far more expensive.

Bonus-heavy roles or variable compensation magnify that risk: when your next paycheck is uncertain or delayed, a thin cushion can quickly become a source of financial stress.

Economic conditions also matter. In volatile markets, workforce layoffs or restructurings affect even white-collar professionals.

How to build a true safety net

Aim to save three to 12 months’ worth of essential expenses, ideally more if you have dependents or high fixed costs. Having a solid emergency fund strategy gives you breathing room when unexpected costs arise, without derailing long-term goals. Having access to a minimum level of liquidity can be more important than accelerating the paydown of high-interest debt.

To do this:

- Take a hands-off approach to the emergency fund so it’s available for an actual emergency.

- Automate regular transfers to a high-yield savings account, so your emergency fund grows while remaining accessible.

- Use the cash flow freed from consolidating high-interest debt (e.g., via a BHG personal loan) to accelerate savings.

- Stress-test your emergency plan once a year: Run through a “what if” scenario—job loss, caring for an aging family member, major home repair—and confirm you could cover expenses for your target number of months. Adjust transfers if the fund wouldn’t hold up.

Blind spot #5: Neglecting retirement and your “future self”

If you earn a sizable income, it’s easy to succumb to the idea that you’ll “catch up later” when it comes to retirement…maybe when income grows, the house is paid off, or kids are in college. But retirement is one area where delayed action often costs the most. BHG Financial research shows that only 45% of Americans are currently saving for retirement, and nearly one in five cite waiting too long as their biggest financial regret.

Without a clear retirement roadmap—including a target retirement number, savings rate, investment mix, and withdrawal strategy—high earners risk losing the benefits of decades of compounding growth.

A simple rule of thumb is that at a 10% annual growth rate, your money will double every 7 years. At that rate, $10,000 invested at age 25 would require nearly $80,000 to be invested at age 45 to have the same nest egg. The cost of delay is very steep.

Underfunding can also result in missing out on “free money,” via an employer contribution match through a 401k or similar account.

Read more: Why High Earners Over 50 Are Consolidating Debt Before Retirement

The high earner retirement trap

Some common pitfalls for high earners:

- Underfunding tax-advantaged accounts (e.g., 401(k), IRAs) or neglecting backdoor strategies because of income limits.

- Overreliance on future income or asset sales to fund retirement—a risky bet if market conditions or valuations change. Many small business owners fall into this trap.

- Not planning for future expenses such as healthcare, long-term care, taxes, or distribution requirements post-retirement.

All of these add up: without planning, you could reach retirement age with far less wealth than anticipated—even after decades of substantial earnings.

Fixing the retirement blind spot

Effective retirement planning for high earners requires structure, consistency, and the discipline to prioritize long-term goals over near-term demands. Calculate your target retirement number and required savings rate now.

Then:

- Max out tax-advantaged accounts, such as 401(k)s and IRAs each year. Where income limits apply, consider backdoor Roth strategies, with guidance from a tax-aware advisor.

- Coordinate debt payoff with retirement contributions by setting dual priorities. Similar to an emergency fund, it may not be the best choice to short-change your retirement contributions to try to pay off debt faster. You can’t borrow for retirement, after all, and it’s hard to make up for lost savings later in life. At the least, ensure you are contributing enough to capture full employer matches.

- Diversify income streams through investments, business ventures, or strategic passive income opportunities, so retirement isn’t solely dependent on salary or future earnings potential.

Blind spot #6: Misunderstanding your true net worth

Many high earners track income closely but rarely evaluate their full balance sheet. Knowing your assets, liabilities, and net worth trends is essential for understanding your progress.

Concentration & liquidity risk

An incomplete view of your net worth can lead to issues like:

- Declining net worth over time due to liabilities growing faster than assets.

- A high net worth but with very high leverage, leaving you more susceptible to market value adjustments (not uncommon with large real estate portfolios).

- A net worth heavily concentrated in employer stock, private practice/small business equity, or real estate.

- Limited liquid assets available for emergencies or opportunities.

This imbalance can leave you vulnerable during market changes, job transitions, or unexpected expenses. You also want your wealth to grow over time, not shrink, at least up until retirement.

How to see (and reduce) these risks

- Conduct an annual net worth review to look at year over year change, and then broken out by clear categories: liquid, semi-liquid, and liquid assets.

- Set targets for how much of your net worth should remain liquid for flexibility.

- Restructure high-interest balances with lower-cost debt, such as a strategic BHG Financial personal loan, to maintain liquidity for opportunities or emergency needs.

10-point financial blind spot audit: A checklist for high earners

- Do I have a written financial plan with specific goals (1, 5,10 years)?

- Do I know my current net worth and how it has changed over the last year or the last 5 years?

- How much high-interest debt do I carry, and at what rates?

- Could a debt consolidation strategy lower my interest costs or free up cash for savings/investment?

- How many months’ worth of essential expenses do I have in emergency savings?

- Am I on track with retirement savings based on my target lifestyle?

- Is my investment portfolio diversified across asset classes and tax buckets?

- Do I have appropriate insurance (life, disability, liability) to protect income and assets?

- Do I regularly review my finances with a professional or trusted advisor?

- When was my last “money date” with myself or my partner to review all the above?

How BHG Financial can support your next step

If any of the above blind spots feel familiar, a BHG Financial personal loan may help bring clarity and control. An unsecured, fixed-rate personal loan is ideal for:

- Consolidating multiple high-interest debts into one manageable payment, simplifying cash flow and reducing interest costs.

- Stabilizing cash flow while you align savings, investment, and retirement contributions—giving you breathing room to build an emergency fund or invest more aggressively.

- Funding strategic investments, such as continuing education, home renovation, or other timely opportunities, while responsibly managing personal debt.

If you’re evaluating whether a personal loan makes sense, consider reviewing BHG’s current rates, terms, and eligibility. You may also want to speak with a financial professional to see if a personal loan aligns with your broader net worth planning and long-term wealth-building strategies.

Check your rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Know what you’re really worth

Being a high earner doesn’t guarantee financial security. In many ways, it raises the stakes. Without clarity—on debt, savings, cash flow, risk exposure, and your long-term goals—the appearance of affluence can mask deeper issues.

The first step toward real wealth isn’t a bigger paycheck; it’s awareness. Review one financial blind spot this week. Map out your debts. Build a one-page plan. Open a high-yield savings account for an emergency fund.

And if you determine that strategic liquidity could help future-proof your finances, consider how a BHG Financial personal loan could become part of a broader, thoughtful approach to long-term wealth.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829