Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Why High Earners Over 50 Are Consolidating Debt Before Retirement

You’ve reached your peak earning years, but even with a high income, you aren’t immune to financial pressure heading into retirement. Mortgages, your children’s tuition, and other obligations can strain cash flow, prompting many professionals over 50 to rely on credit cards or loans to keep pace.

Consolidating debt before retirement is a smart way to take control: it can lower interest costs, simplify repayment, and free up cash flow—giving you the breathing room to focus on what matters most in your next chapter.

The retirement debt dilemma—even for high earners

Debt after 50 is more common than you think

Carrying debt into your 50s or 60s isn’t unusual—even for those making six figures. Americans in their 50s carry an average of more than $97,300 in debt.

This figure includes everything from mortgages and home equity lines to credit cards and even lingering student debt. For high-income professionals, that total can easily be higher due to investments or other substantial financial obligations.

Having debt at this stage of life doesn’t signal poor planning. More accurately, it often reflects a lifetime of investing in your career, your family, and your future.

Rising expenses, delayed milestones, and big goals

Many professionals over 50 are part of the sandwich generation: helping adult children through college, supporting aging parents, and maintaining multiple properties—all while trying to ramp up retirement contributions.

These overlapping priorities often push major financial milestones later in life, leaving high earners juggling both short-term obligations and long-term goals. By their 40s and 50s, many professionals are earning more than at any other point in their careers, yet these peak earning years often feel the most financially demanding.

That’s why simplifying debt and improving cash flow through consolidation has become an important step toward regaining financial control before retirement.

The problem isn’t income—it’s interest

When cash flow tightens, many high-income professionals turn to credit cards and other forms of financing to bridge the gap—especially when most of their wealth is tied up in illiquid assets like investments, retirement accounts, or real estate. It’s a temporary fix that can quickly backfire if not managed responsibly.

A professional earning a six-figure salary could still lose significant ground if much of that income is used to service revolving debt with double-digit APRs. Even a few months of carrying balances can erode liquidity and delay financial independence. Over time, this reliance on high-interest credit can trap otherwise successful professionals in a cycle of expensive borrowing.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Why consolidating debt is a smart pre-retirement move

Streamline and reduce monthly payments

Debt consolidation simplifies your finances by combining multiple debts into one fixed-rate personal loan. For high-income borrowers, that often means trading several variable, high-interest balances for a single predictable payment—usually at a lower rate.

This consistency creates breathing room. Lower monthly obligations can help redirect cash flow toward retirement catch-up contributions or strategic investing. Even saving an extra $1,000 per month can make a six-figure difference over the final decade before retirement.

Save on interest and simplify planning

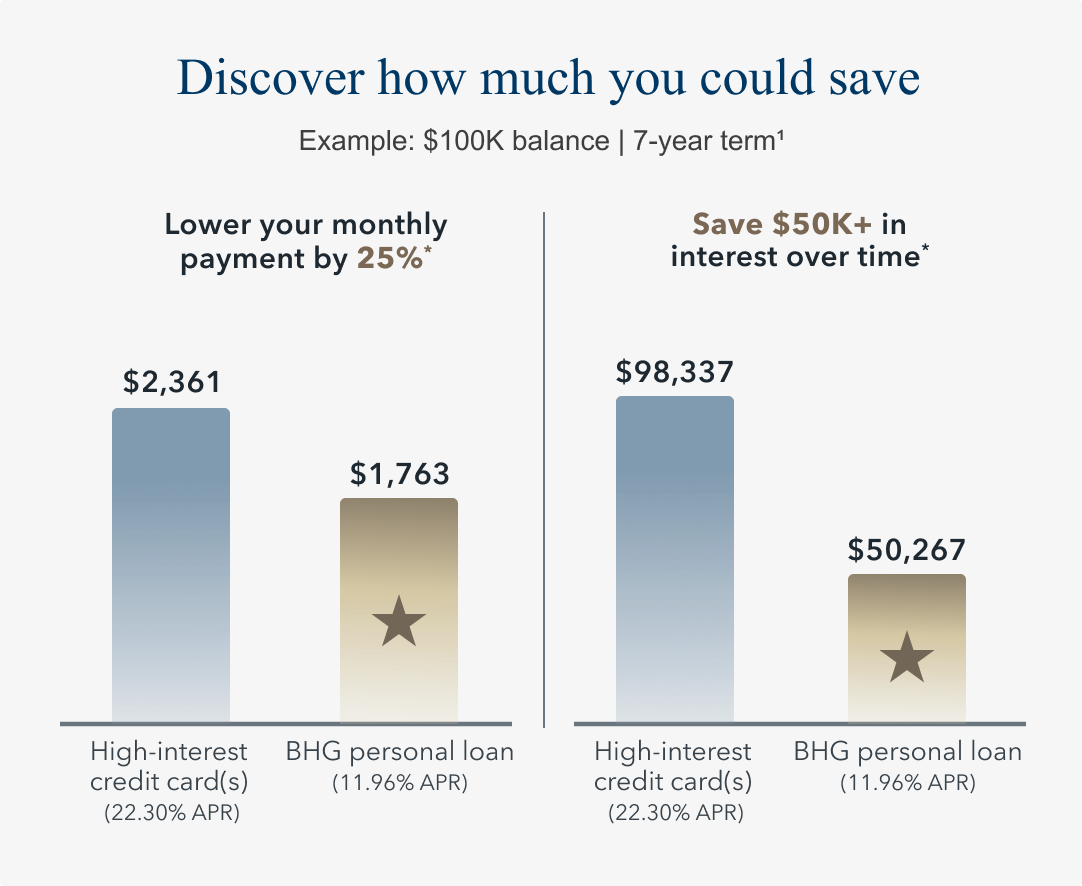

Consolidating debt with a fixed-rate personal loan can significantly reduce the total interest you pay compared to variable-rate credit cards.

For example, shifting $100,000 in combined debt from an average 24% interest rate to a fixed 12% could save more than $56,000 over a seven-year term. More importantly, predictable payments and a clear payoff date make planning easier as you approach retirement.

This streamlined structure is particularly valuable for financial planning over 50, when economic volatility and uncertainty around future cash flow can make high-interest debt even riskier.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $100,000 balance over 7 years on both a credit card with a minimum monthly payment of $2,361 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $1,763 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

Improve cash flow to boost retirement contributions

The money you save by becoming debt free in your 50s can compound quickly, allowing you to optimize your remaining earning years. Consolidating high-interest obligations into one manageable monthly payment can unlock the liquidity to:

- Maximize 401(k) or IRA contributions, including catch-up limits.

- Build an HSA for future healthcare expenses.

- Reinvest in income-generating assets such as real estate or brokerage accounts.

How BHG’s personal loan supports retirement prep for high earners

Tailored for high-income professionals with strong credit

Unlike traditional lenders, BHG Financial takes a comprehensive view of your financial picture—not just your credit score. That means your professional success, cash flow, and overall creditworthiness all factor into your offer.

BHG provides tailored debt solutions for high-income professionals that help simplify repayment and improve financial flexibility before retirement. Whether you’re consolidating high-interest credit cards, other personal loans, or medical debt, BHG offers a tailored approach that fits your financial goals.

Higher loan amounts, longer terms

High earners often have complex finances and considerable debt. That’s why BHG provides unsecured personal loan amounts up to $250,0001 and repayment terms as long as 10 years1,2—among the most flexible in the industry.

These extended terms can significantly lower your monthly payments, giving you room to maintain contributions, preserve liquidity, and prepare for future milestones without financial strain.

Quick, confidential, and credit-safe

BHG’s concierge loan process is designed for busy professionals who value both efficiency and privacy:

- No impact on your credit score to prequalify.3

- Approval decisions in as little as 24 hours.4

- Funds deposited in as few as five days.4

You’ll also work with a dedicated, U.S.-based loan specialist who helps ensure a smooth experience from application to funding.

Debt consolidation over 50: strategy, not sacrifice

As retirement approaches, debt consolidation can shift your focus from managing payments to maximizing possibilities. Instead of feeling burdened by debt, you can feel in control of your next chapter.

- Freeing up resources for what’s next: With lower monthly payments and reduced interest, you can redirect funds toward what matters most: travel, second careers, healthcare planning, or legacy-building.

- Better debt profile = better retirement readiness: Consolidating high-interest balances can improve your credit utilization ratio, which may strengthen your credit score and overall borrowing power. A stronger credit profile gives you more options if you decide to refinance your home, buy investment property, or access future financing at a lower rate.

- Emotional confidence going into retirement: Fewer bills, predictable payments, and a clear payoff timeline reduce mental load and financial stress.

Key questions for high earners nearing retirement

Should you carry debt into retirement?

Most experts agree that carrying high-interest debt into retirement can make even modest balances feel heavy. When income slows and savings need to last, paying more than necessary in interest can quickly add up.

It’s important to have a plan to address outstanding debt in retirement, including setting a budget and prioritizing a responsible payoff solution. Consider the following questions. If you answer yes to any, debt consolidation could be a smart move.

- Are you losing money to high APRs? Compare your current rate(s) to what you could secure through a fixed-rate consolidation loan. Getting an APR even just a few percentage points lower can translate to thousands of dollars saved for your future.

- Could you be saving more if you consolidated? Ask yourself: what could you achieve with that extra cash each month? Make more contributions to your retirement accounts, build a bigger emergency fund, or capitalize on strategic investments? By aligning debt management with your retirement goals, consolidation becomes a way to regain control of your finances.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Final thought: Consolidate now, retire with confidence

Consolidating debt before retirement isn’t about cutting back—it’s about moving forward with clarity and control. By streamlining payments, reducing interest, and freeing up liquidity, high earners can make the most of their peak earning years while positioning for a smoother, more confident transition into retirement.

If you’re 50 and older and planning for retirement, explore how a BHG personal loan can streamline your debt, reduce interest, and help you save more. Prequalify in minutes, with no impact to your credit.3

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

4 This is not a guaranteed offer of credit and is subject to credit approval.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829