Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

How to Improve Your Credit Score: Tips to Boost Your Credit

Your credit score is a powerful tool that helps you access better loan rates, easier approvals, and more financial opportunities. The higher your scores—ideally in the high 700s and above—the greater your borrowing power.

Building a credit history and improving your score takes time and effort. Below, we’ll provide tips to quickly raise your credit score, putting you on the path to a more secure financial future.

Key takeaways

- Your credit score is a reflection of your financial responsibility, directly impacting your ability to access credit.

- Timely payments and smart credit management are crucial for rapid credit score improvement. Regularly checking your credit report for errors can also help protect your financial standing.

- Building good credit isn't an overnight process—steady, smart financial habits will pay off.

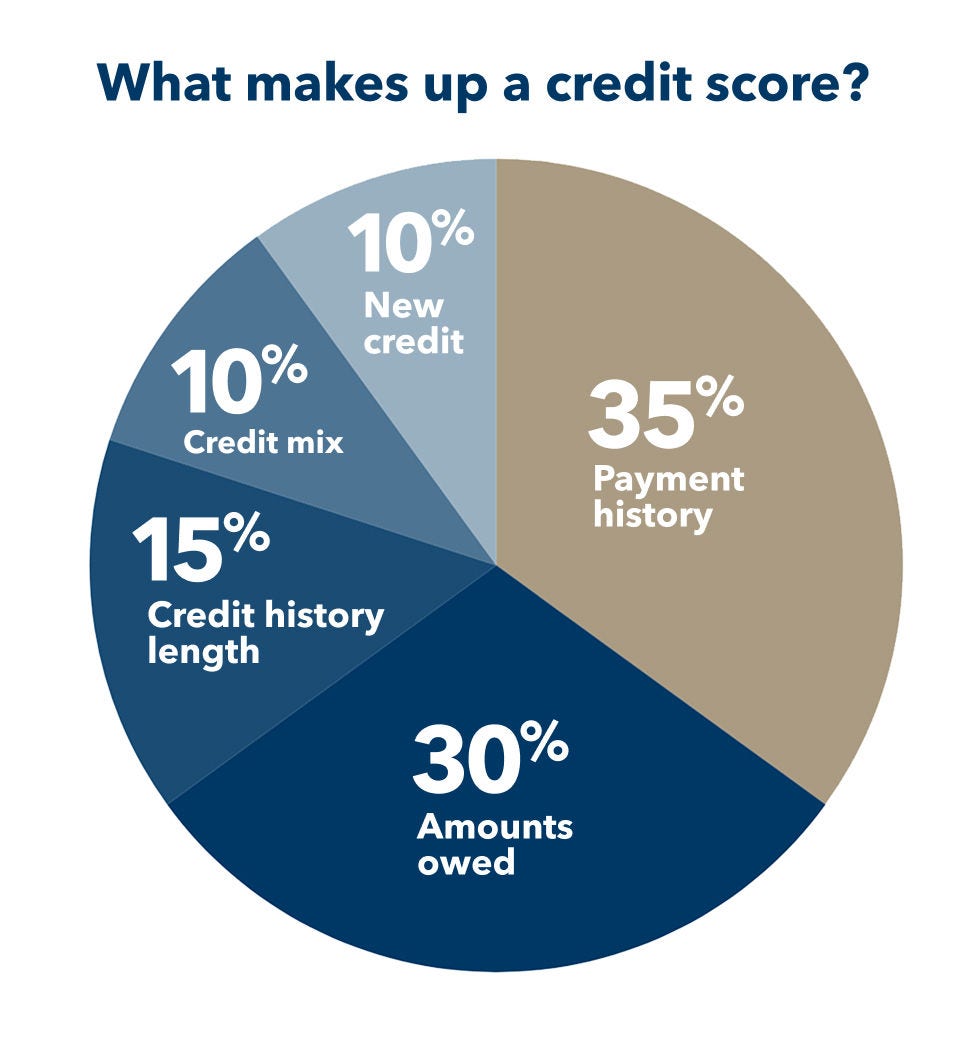

How is your credit score determined?

Credit scoring systems like FICO® Score and VantageScore® weigh your financial habits to create a three-digit number that lenders use to assess your creditworthiness. FICO® Score is more common.

The three major credit bureaus, including Equifax, Experian, and TransUnion use the following factors to determine your credit score.

- Payment history: Whether you’ve paid your past credit accounts on time

- Amounts owed: The amount of available credit you are using

- Length of credit history: How long you've had your credit accounts

- Credit mix: The different types of credit accounts you have

- New credit: The frequency of credit inquiries and new account openings

In 2025, the Federal Housing Finance Agency expanded its use of VantageScore 4.0 in certain mortgage‑related evaluations, and adoption is growing across consumer lending, auto financing, and credit card issuance.

Now, lenders can use both FICO and VantageScore 4.0 to more accurately assess how borrowers are managing debt over time. VantageScore 4.0’s expanded framework also unlocks broader access to credit, thanks to its ability to score consumers with limited credit histories.

How to raise your credit score quickly

Here are six strategies that may help you improve your score:

1. Make on-time payments

Payment history is the biggest factor influencing your credit score, making up 35% of your FICO score. This means that paying your bills on time, every time, is the single most effective tip to raise your credit score. Even one late payment can cause your score to drop significantly.

Setting up automatic payments with each card company can help ensure you don’t miss a due date that could hurt your score.

2. Reduce your credit utilization

Credit utilization strategies are essential for a healthy credit score. This refers to the amount of credit you're currently using relative to the total credit you have available.

For example, if you have a credit card with a $20,000 limit and a balance of $7,000, your utilization is 35%. Experts generally recommend keeping this ratio at or below 30%.

Decreasing your credit card balances shows potential lenders that you're responsible with credit. By actively managing your balances and paying off debt, you can significantly improve your score. The debt avalanche or snowball method of repayment can help you pay off your credit card debt.

Instead of making just one payment per month, consider multiple payments throughout the month to keep your credit utilization low. Strategically paying your credit card bill can increase your credit score: If your balance is lower at the time your statement is issued, it will be reflected in your credit report.

You may be able to ask your card issuer to increase your credit limit if your income has recently increased, or you’ve built up a history of on-time payments and responsible credit use. A higher credit limit can help lower your credit utilization rate, and in turn, improve your score.

3. Consolidate your debt

If you’re carrying balances across multiple high‑interest credit cards, debt consolidation can be a powerful way to improve your credit score while simplifying repayment. A debt consolidation loan allows you to combine several credit card balances into a single loan—often with a lower interest rate and a fixed monthly payment.

By paying off your cards in full, you immediately reduce your revolving credit balances, which can lower your overall credit utilization rate and positively impact your score.

In fact, most borrowers who consolidate credit card debt through BHG improve their FICO score by 30 points or more within a few months of funding.*

Plus, streamlining your finances into one predictable payment makes it easier to stay on track and reduces the risk of missed or late payments.

Most borrowers who consolidate debt through BHG improve their FICO score by 30 points or more within a few months of funding.*

4. Regularly check your credit reports

Regularly reviewing credit reports for errors is a vital step in maintaining good financial health. Your credit report contains detailed information about your borrowing history, and mistakes can happen. Monitoring your report also helps you understand what triggers fluctuations and know when you might qualify for better offers.

Register with a service like Credit Karma to monitor your credit score and accounts. Checking your own credit score is considered a “soft credit check,” which doesn’t impact your score. You can also request one credit report a week for free from each of the three main credit reporting agencies: Equifax, Experian, and TransUnion.

If you find an error, you can dispute it by contacting the reporting company online, by phone, or by mail, and providing documentation that supports your dispute.

5. Maintain a healthy credit history

You may feel inclined to close accounts you aren’t using, but it’s beneficial to keep older accounts open. This is because closing inactive accounts can increase your credit utilization rate, take away from your credit mix, and shorten your overall credit history—two things you want to avoid to maintain a healthy score.

When building credit history, keep your oldest accounts open as long as you can. Using an old card for small balances (that you pay off in full when it’s due) helps it remain active and contribute positively to your score.

While keeping older accounts open is helpful, avoid opening too many new credit accounts in a short period of time. New applications can trigger hard inquiries and lower the average age of your credit history, which may cause temporary dips in your score. Instead, focus on managing your existing accounts responsibly and only apply for new credit when it supports a clear financial goal.

If you pay rent, consider using rent reporting services as a way to establish a credit history and improve your credit mix by adding a different type of credit in your file. Companies like RentReporters or Experian Boost can report your monthly rent payments to the credit bureaus, allowing you to build credit on payments you're already making and build a more diverse credit history over time.

6. Become an authorized user

Becoming an authorized user on someone else’s credit card can help build or strengthen your credit, especially if you're newer to credit or are actively trying to rebuild it. When you’re added to a well‑managed account, the card’s payment history and credit limit may appear on your credit report, potentially improving your utilization and overall profile.

This approach works best when the primary cardholder has a long history of on‑time payments and low balances. You don’t need to use the card to benefit—but it’s important to choose carefully, since missed payments or high balances on the account could negatively affect your score as well.

How a debt consolidation loan through BHG Financial can help you improve your credit score

With on-time payments and credit utilization being two of the most significant factors that affect your credit score, paying off high-interest debt can be a way to improve your score faster.

BHG offers personal loans for debt consolidation that help you manage existing obligations more effectively. Our personal loans are tailored to your needs, with amounts up to $250,0001 and flexible terms of up to 10 years.1,2

Here’s how BHG can help:

- A way to compare offers without hurting your credit score3: Our initial review process does not affect your credit score, allowing you to check your eligibility for loan offers and estimate your payment using a soft credit inquiry.

- The ability to leverage earnings: When reviewing a loan application, we consider both your credit score and income. Higher earners may also be able to secure financing through BHG, even if their debt-to-income ratio is elevated.

- Flexible terms and predictable payments: We can offer extended repayment options, keeping your monthly payments manageable. A good score can also qualify you for lower, fixed rates, saving you interest over the life of the loan.

Plus, making consistent on-time payments on credit products like personal loans can actually improve your score over time. Most borrowers who consolidate debt through BHG Financial improve their FICO score by 30 points or more within a few months of funding.*

Ready to see what’s possible? Explore your personalized loan options in just seconds.4

Check my rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

How to improve credit score FAQ

How can I raise my credit score in 30 days?

In the short term, the fastest way to improve your credit score is to lower your credit utilization by paying down credit card balances and making all payments on time. Most borrowers who consolidate debt through BHG Financial improve their FICO score by 30 points or more within a few months of funding.*

What brings your credit score up the fastest?

Reducing revolving credit balances typically has the quickest impact on your credit score, especially if your utilization is currently high. By consolidating credit card debt into a single personal loan, most borrowers working through BHG Financial have improved their credit score by 30+ points* through lower utilization and more consistent payment behavior.

Can paying off debt lower my credit score?

While paying off a loan or credit card often helps improve your credit score, it’s possible that you could see your credit score drop temporarily after fulfilling your payment obligations. Typically, the long-term impact of paying off debt is positive.

How often should I check my credit report?

The three national credit reporting agencies—Equifax, Experian, and TransUnion—now let you check your credit report at each of the agencies once a week. You can request free copies of your report at AnnualCreditReport.com. Reviewing your reports at least once a year, and ideally every few months, is good practice to ensure accuracy and monitor your credit health.

Does closing a credit card affect my score?

Yes, closing a credit card can negatively impact your credit score. This is because closing an account reduces your total available credit, which can increase your utilization ratio. It also shortens the average age of your credit accounts, which impacts your credit history length.

Not all solutions, loan amounts, rates or terms are available in all states.

*Based on internal data, most BHG debt consolidation borrowers may improve their FICO® score by 30+ points within 2 months. Credit scores depend on many factors and individual results may vary based on personal spending habits.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

4 This is not a guaranteed offer of credit and is subject to credit approval.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829