Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Debt Consolidation in a High-Rate Economy: Is It Still Worth It?

Table of Contents

- The Current Economic Landscape: Why Rates Are So High Today

- What Is Debt Consolidation—and How Does It Work in 2025

- When Debt Consolidation Still Makes Sense—Even In A High-Rate Environment

- Why High-Earners Are Using Personal Loans for Debt Consolidation

- Comparing Today’s Debt Consolidation Loan Rates to Credit Cards

- How to Choose the Right Debt Consolidation Loan in This Economy

- Final Thoughts: Debt Consolidation in a High-Rate Economy—Smart Strategy or Misstep?

Interest rates are up. Credit card debt is climbing. Even high-income professionals are feeling the pinch. In today’s economy, where borrowing costs remain elevated, many are wondering if debt consolidation still makes sense. For the right borrower, it absolutely can.

Debt consolidation has long been a strategic move to streamline payments, lower total interest paid, and simplify monthly budgeting. But with average personal loan rates higher than they were just a few years ago, the value of consolidation depends on your specific financial profile—especially your credit score and cash flow.

For high earners juggling significant obligations, consolidating multiple debts into a single fixed-rate personal loan can still be a smart financial decision. More than just reducing your interest rate, consolidation is about regaining control and finding relief in a structured repayment plan.

Let’s break down the current economic landscape and uncover when and why consolidation makes sense today.

The Current Economic Landscape: Why Rates Are So High

The Fed’s fight against inflation

Since 2022, the Federal Reserve has been actively working to combat persistent inflation. To do this, it raised the federal funds rate significantly, making borrowing more expensive across the board.

While the Fed has been aggressive with rate hikes, there's always a possibility for changes. Two cuts by the end of 2025 are still on the table, but it's not a sure thing. This makes it even more important for borrowers to find potential savings and streamline their finances now.

Prime rates, credit cards, and borrowing costs are all up

When the prime rate rises, so does the interest you pay on everything from your mortgage to your car loan to your credit cards. Even those with excellent credit aren’t immune to the effects.

In 2021, personal loans with fixed repayments over two years had an average interest rate of 9.38%, according to Federal Reserve data. The current rate is now 11.57%. Annual percentage rates on credit cards have also increased steadily over the past few years. The average APR on all credit card accounts was 21.16% as of May 2025, a big jump from 14.6% in 2021.

What this means for high-income borrowers

Six-figure earners are often perceived as financially secure—but rising rates affect borrowers across all income brackets. Professional obligations, family expenses, and social and familial expectations to “live up” to success all put pressure on monthly budgets.

That said, high earners typically benefit from better credit scores and stronger financial profiles, which qualify them for larger loans with lower interest rates and better terms. This opens the door to debt consolidation strategies that put you on the path to a more secure future.

What Is Debt Consolidation—and How Does It Work in 2025?

Traditional definition and benefits

At its core, debt consolidation involves taking out one new loan to pay off multiple high-interest debts. Instead of juggling multiple balances, you get just one fixed payment each month. The benefits of debt consolidation include:

- Potentially lower interest rates.

- Simplified debt repayment strategy

- Possible credit score boost (improved credit utilization and on-time payment history)

How consolidation works in a high-rate economy

Despite the current elevated-rate environment, personal loans for debt consolidation can still offer lower interest rates than high-interest credit cards. Transitioning from multiple payments to a single, streamlined payment can also significantly simplify your financial life.

If you're carrying high-rate debt as a prime borrower, chances are a consolidation loan will still save you money and reduce stress.

Fixed vs. variable debt: Predictability is key

When times are uncertain, predictability matters. Switching from variable-rate debt—like credit cards or business lines of credit—to a fixed-rate personal loan creates a sense of security. Variable interest rates fluctuate with the market, making monthly payments unpredictable.

With a fixed-rate loan, your payment amount stays the same each month, allowing you to budget confidently and plan for the long-term—no matter what the future brings.

When Debt Consolidation Still Makes Sense—Even in a High-Rate Environment

You have strong credit and qualify for competitive loan rates

If you have a strong credit history and a good credit score, you are considered a "prime borrower." This is a significant advantage in any economic climate, especially when rates are high.

Prime borrowers often qualify for personal loan rates that are much lower than the rates on their existing high-interest debts, such as credit cards. While credit card rates can ebb and flow with economic factors, a fixed-rate personal loan offers a stable, more affordable APR.

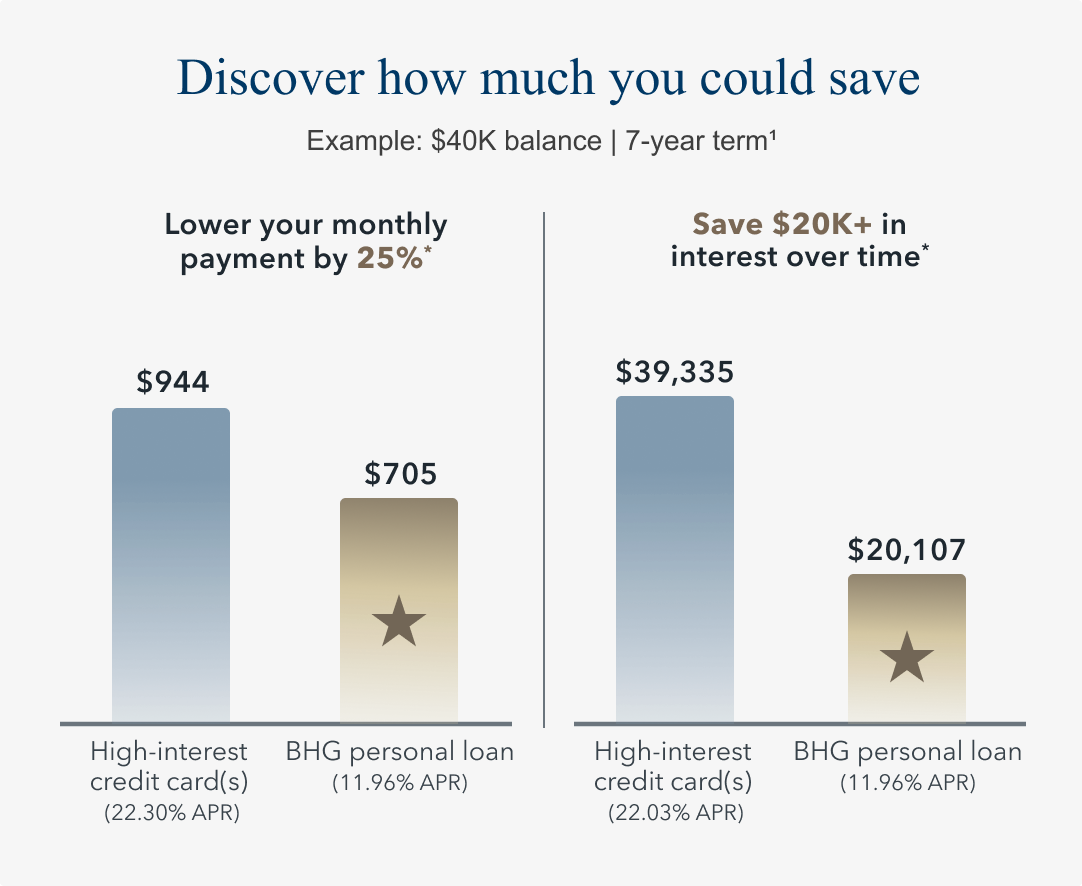

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $40,000 balance over 7 years on both a credit card with a minimum monthly payment of $944 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $705 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

You’re juggling multiple high-interest accounts

Juggling multiple credit cards with different due dates and interest rates can be overwhelming. Debt consolidation simplifies this process by combining all your debts into one monthly payment, reducing stress and helping you avoid missed payments.

You want to free up monthly cash flow

Personal loans—especially those with longer terms—can lower your monthly payment. This improves your immediate cash flow and allows you to allocate funds to other important areas of your life.

FYI: BHG Financial offers extended repayment terms up to 10 years,1,2 which are longer than those offered by most other lenders.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Why High-Earners Are Using Personal Loans for Debt Consolidation

Liquidity struggles despite high income

Just because you earn a lot doesn’t mean you always have cash on hand.

Rising living costs, business expenses, tax bills, education fees—these obligations all chip away at liquidity. Many professionals carry balances on credit cards to stay flexible, but those balances come with high costs.

A consolidation loan can restore liquidity by reducing monthly payments and interest charges.

Smart debt management as a strategic move

For high earners, debt consolidation is about more than just staying afloat—it's a smart strategy to manage debt better, improve cash flow, and build long-term financial stability. It turns expensive, unpredictable debt into a more manageable and often more affordable form of financing.

Why BHG Financial stands out

At BHG Financial, we understand the unique financial realities of high-income professionals. Our personal loan solutions are designed to support complex situations, using the following features:

- High loan amounts (up to $250K)1: We offer significantly higher loan amounts than many competitors, so you can consolidate debt, cover major expenses, or work toward multiple goals at once.

- Longer terms for lower payments: Our flexible repayment terms extend up to 10 years.1,2 This can help keep your monthly payments low and manageable.

- No personal collateral required: Our personal loans are unsecured, meaning you don't need to put up any personal assets, like your home or car, as collateral.

- Soft credit inquiry for prequalification: You can compare offers for a loan and see your potential rates without impacting your credit score.3

Comparing Today’s Debt Consolidation Loan Rates to Credit Cards

Average personal loan rates for prime borrowers

Average personal loan APRs currently range from 10% to 15% for borrowers with excellent credit. While these rates are higher than they were a few years ago, they are still competitive, especially when compared to credit card APRs.

Average credit card APRs have surpassed 20%

The average APR on all credit card accounts is more than 21%. If you carry a balance month to month, you’ll pay a steep premium.

This significant difference means that consolidating high-interest credit card debt into a personal loan could translate to thousands in annual savings, especially when consolidating larger balances.

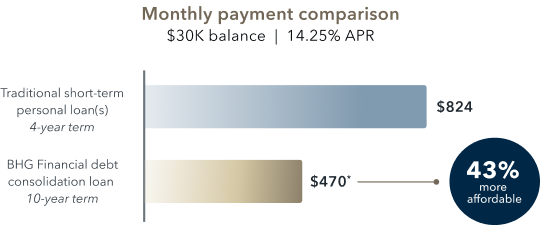

Consolidation example: A professional with $30K in credit card debt

Dr. Smith, a high-earning medical professional, carried $30,000 across multiple credit cards with an average APR of 24%. His minimum payments exceeded $900 per month, straining his cash flow.

For a better borrowing solution, Dr. Smith explored loan options for consolidating his high-interest debt, but the repayment terms differed. His current lender offered Dr. Smith a debt consolidation loan with a four-year term. With these terms, Dr. Smith would have a monthly payment just shy of $830—too high for his budget. Instead, Dr. Smith chose to consolidate with a BHG Financial personal loan with a longer 10-year term.1,2 The option to spread out repayment terms helped reduce his monthly payment to just $477, a 42% savings.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* BHG monthly payment based on BHG’s minimum available APR for a 10-year term, which is 14.25% as of 05/13/26 and includes an origination fee. Your actual loan size, loan term, and monthly payment amount may vary based on your individual credit profile and other information provided in your loan application. Terms subject to credit approval.

In a high-rate environment, choosing a structured, longer-term solution allowed Dr. Smith to reduce financial pressure and increase his purchasing power each month.

How to Choose the Right Debt Consolidation Loan in This Economy

Focus on total cost, not just monthly payment

While a lower monthly payment can be very appealing for cash flow, extending your loan term may increase the total interest paid. Consider the total cost of the loan over its entire term, and choose terms that allow you to balance immediate cash flow relief and long-term interest costs.

Determining a budget for your loan may also be easier when you switch from variable interest rates to a loan with a fixed rate because you won’t need to worry about rising rates due to future economic shifts.

Understand all fees and loan terms

Before signing any loan agreement, make sure you thoroughly understand all fees and terms. At BHG Financial, we take pride in our transparent structure, with no prepayment penalties or hidden fees. Your loan agreement outlines every detail, helping you maintain control of your financial decisions and avoid any unwelcome surprises down the road.

Choose lenders that understand your financial reality

Not all lenders serve high-income professionals with complex financial obligations. BHG specializes in loans for borrowers with unique financial goals, offering customized solutions that go beyond one-size-fits-all lending.

Our loan products are specifically designed for individuals who may carry significant debt but have the income and prime credit to manage it responsibly. When evaluating applications, we look at more than just your credit score and consider your overall financial picture.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Final Thoughts: Debt Consolidation in a High-Rate Economy—Smart Strategy or Misstep

Yes, interest rates are high. But credit card APRs are even higher. Prime borrowers can still come out ahead with the right debt consolidation strategy.

If you have strong credit, consolidating your debts into a fixed-rate personal loan from BHG can offer structure, stability, and cash flow—especially when juggling multiple accounts.

Ready to see what’s possible? Use our quick and easy payment estimator to get your personalized loan estimate in just seconds.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 This is not a guaranteed offer of credit and is subject to credit approval.

3 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829