Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

$150,000 Personal Loan from BHG Financial for Debt Consolidation

Table of Contents

- Overview of BHG Financial personal loans

- Eligibility requirements for a $150,0001 personal loan

- Flexible repayment terms and competitive APRs

- Application process and funding timeline

- Benefits of using BHG Financial for consolidation

- Important considerations and fees

- How to maximize your loan for debt consolidation

- Let BHG help you regain control

- Check my rate

- FAQs

When debt starts to feel fragmented and inefficient, a $150,0001 personal loan can be a practical way to regain control without tapping home equity or liquidating savings. BHG Financial specializes in large, unsecured personal loans for high-income borrowers seeking flexible solutions and predictable repayment schedules.

With loan amounts reaching up to $250,000,1 BHG offers $150,0001 personal loans that help qualified borrowers consolidate multiple high-interest debts into a single, manageable payment. BHG's tailored debt consolidation loan is designed to simplify repayment, improve cash flow, and create long-term financial breathing room.

Overview of BHG Financial personal loans

While many banks and traditional lenders cap unsecured personal loans at around $50,000 to $100,000, BHG offers one of the largest high-limit personal loan solutions in the market. Loan amounts are available up to $250,000,1 with $150,0001 unlocking enough funds to handle comprehensive debt consolidation, not partial fixes.

BHG loans are unsecured, meaning no collateral, such as a home, vehicle, or investment account, is required. Approval is based primarily on:

- Credit profile

- Income and cash flow

- Overall financial health

This structure appeals to professionals who want to preserve assets while still accessing meaningful borrowing power. Many BHG borrowers earn strong incomes but experience uneven cash flow, making fixed payments and flexible terms especially valuable.

BHG’s specialized underwriting approach is built for these realities. Instead of relying solely on traditional lending formulas, it considers the full financial picture of high earners, recognizing that income complexity doesn’t automatically equal repayment risk.

Maximize your cash flow

Check your rates and explore fixed-payment loan options

Eligibility requirements for a $150,0001 personal loan

Because BHG focuses on large loan amounts1, its eligibility standards are designed to ensure borrowers can comfortably manage monthly payments.

Typical minimum requirements include:

|

Requirement |

Minimum standard |

|---|---|

|

Annual income |

$100,000+ |

|

Loan amounts |

Up to $250,0001 |

|

Employment |

Stable professional or business income |

|

Collateral |

None required |

Beyond credit scores, BHG evaluates factors such as professional credentials and long-term earning potential. Supporting documentation typically includes recent tax returns, income statements, and bank statements to confirm overall financial stability.

Flexible repayment terms and competitive APRs

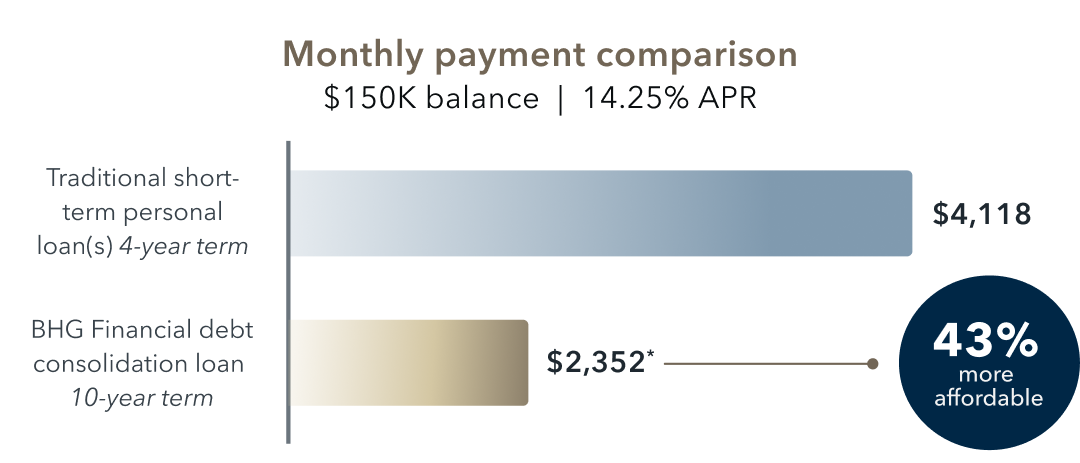

BHG Financial structures our personal loans with flexibility in mind, offering extended repayment terms from three to 10 years.1,2 This range, which is among the longest in the industry, allows borrowers to balance monthly payment affordability with total interest costs. Choose shorter terms to minimize interest or longer terms to preserve monthly cash flow.

The Annual Percentage Rate (APR)—the total yearly cost of borrowing, including interest and fees—ranges from 6.49% to 28.89% depending on creditworthiness, income, loan amount, and term length. All rates are fixed, so payments never change over the life of the loan.

Rate and term features:

- Fixed interest rates for predictable payments and simpler budgeting

- No prepayment penalties, allowing borrowers to pay off personal loans early without additional costs.

- Extended terms up to 10 years1,2 to lower monthly payments.

- Shorter terms available for those focused on minimizing total interest.

Why extended terms matter

Longer terms can significantly reduce monthly payments, even if total interest paid increases over time. For many professionals, the goal isn’t the lowest possible interest cost—it’s sustainable cash flow.

Lower monthly payments can create room in the budget for emergency savings, retirement catch-up contributions, or home improvements.

*BHG monthly payment based on BHG’s minimum available APR for a 10-year term, which is 14.25% as of 05/13/2026 and includes an origination fee. Your actual loan size, loan term, and monthly payment amount may vary based on your individual credit profile and other information provided in your loan application. Terms subject to credit approval.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only

Application process and funding timeline

BHG Financial has streamlined its application process to respect the schedules of busy professionals. It balances speed with personalization, with funding available in as few as five days after approval.3

How it works:

- Online prequalification: Prequalify and submit basic financial information to explore loan offers. BHG will perform an initial soft credit inquiry that does not impact your credit score.4

- Complete online application: If you decide to move forward, upload income verification, identification, and financial documents to complete your application.

- Personalized assessment: Let a dedicated loan specialist review your application and financial profile.

- Loan options: Receive customized loan options3 with specific terms, rates, and conditions.

- Final approval and signing: If approved, complete any additional verification and sign the loan documents.

- Funding: BHG will conduct a hard credit inquiry at this stage. Receive funds directly deposited into your bank account.

You’ll also work with a dedicated loan specialist throughout the process—someone who can answer questions, discuss your options, and help keep things moving. The goal is to make the experience feel straightforward, not overwhelming.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Benefits of using BHG Financial for debt consolidation

Choosing BHG Financial for debt consolidation delivers multiple advantages for high-income professionals managing complex financial obligations.

Primary benefits:

- Simplified repayment: Replace multiple credit card payments or other debts with a single monthly payment. Plus, fixed rates and terms eliminate payment uncertainty.

- Potential interest savings: Personal loan APRs are generally lower than credit card rates, especially for prime borrowers.

- Improved liquidity: Free up monthly cash flow by extending repayment terms or reducing interest costs.

- Credit score improvements: Paying off revolving balances lowers the credit utilization ratio, which can support higher scores.

- Easier budgeting: The predictable payment structure supports long-term financial planning, whether for retirement or wealth-building strategies.

For many borrowers, consolidation also provides mental relief. Reducing multiple payment obligations to a single, manageable monthly commitment often reduces financial stress and creates mental space—so borrowers can focus on their careers, families, and long-term goals instead of managing debt logistics.

Read more: The Hidden Cost of Success: How Debt Stress Affects High Earners

Important considerations and fees

When taking out a large personal loan, choosing a reputable lender matters. Transparency around costs, flexibility in repayment, and clear communication should be a priority.

When comparing lenders, look for:

- Upfront disclosure of origination fees: Know what you’re paying and why.

- No prepayment penalties: The flexibility to pay off your loan early if your income allows.

- No hidden fees: Clear terms with no surprises after funding.

- Accessible support: Specialists who can walk you through scenarios and tradeoffs.

Origination fees typically range from 3% to 8% of the loan amount, depending on the borrower's credit profile and the lender. BHG’s origination fees range on the lower side of 3% to 5%. On a $150,0001 loan, that’s approximately $4,500 to $7,500, deducted from the loan proceeds at funding.

Before committing, review your loan agreement in full, so you understand total repayment costs, monthly obligations, and flexibility options. BHG loan specialists can help model different terms to support an informed decision that fits your financial goals.

How to maximize your loan for debt consolidation

The most effective consolidation strategies treat the loan as a reset—not just a payment swap. Pair your $150,0001 personal loan with a clear plan for building intentional habits that help support lasting control.

Simple strategies to get the most value from your debt consolidation loan:

- Prioritize high-interest debt: Focus consolidation on credit cards and other obligations carrying APRs above 15%.

- Prequalify and compare offers: Ensure your consolidated rate saves money compared to the current weighted average interest rates.

- Choose a payment you can sustain: Ensure your monthly payment suits your budget. Consider automating payments to stay consistent and protect your credit.

- Avoid new balances: Build a budget that prevents credit cards from creeping back up.

- Build emergency reserves: Direct any monthly savings from consolidation toward an emergency fund.

- Consider strategic prepayments: Apply bonuses or windfalls to your principal when possible.

Let BHG help you regain control

A high-limit personal loan from BHG Financial offers a structured solution for professionals who want clarity, predictability, and a chance to build momentum.

By consolidating debt into one fixed payment with a defined endpoint, borrowers can simplify their finances, protect liquidity, and move forward with confidence—on their terms.

Ready to explore your options for a $150,0001 loan?

Check my rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

FAQs

What credit score and income are needed to qualify for a large personal loan?

BHG Financial typically requires a minimum FICO credit score of 640 and an annual income of at least $100,000 to qualify for large personal loans.

How quickly can I receive loan funds after approval?

Approved loans can be funded in as few as five days.4

Are there any fees or penalties for early repayment?

No, BHG Financial does not charge prepayment penalties for paying off your personal loan early.

Does applying for a loan affect my credit score?

The initial application involves only a soft credit check that does not impact your credit score4; a hard inquiry occurs only when you proceed with a formal loan offer.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 This is not a guaranteed offer of credit and is subject to credit approval.

4 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829