Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Can Debt Consolidation Improve Your Credit Score?

Table of Contents

- How to make credit work even harder

- How consolidation can improve a strong credit score

- When consolidation makes sense

- Why BHG is the strategic choice for high performers

- Other benefits of strategic debt consolidation

- Key questions for high earners considering consolidation

- Use consolidation to strengthen what you’ve already built

You’ve worked hard to build wealth using consistency and smart decisions—and your strong credit reflects it. However, many overlook the fact that having good credit is just the beginning. Strategic debt consolidation for high credit-score borrowers can help you optimize your financial profile even further, strengthening your score while simplifying how you manage debt.

Most borrowers who consolidate debt through BHG improve their FICO score by 30 points or more within a few months of funding.

Whether you’re preparing for a major investment, streamlining high-interest accounts, or simply ready to fine-tune your credit health, consolidation can be a smart next step. Here’s how to use consolidation to unlock even greater possibilities.

You’ve built strong credit—here’s how to make it work even harder

Why high earners still carry debt

Even with strong credit and stable income, many six-figure earners carry multiple balances across credit cards, personal loans, or business-related expenses. That’s not necessarily a problem—using revolving credit strategically can be a smart way to cover personal expenses, home improvements, or free up cash flow for investment opportunities.

But juggling multiple high-interest balances comes at a cost. Those accounts often carry variable rates, complex due dates, and utilization ratios that can hold your score back. And if you miss a payment, or carry a balance month to month, 20%+ APRs can undermine even the strongest credit profile.

Great credit doesn’t mean you’re fully optimized

Having excellent credit puts you ahead, but there’s still an opportunity to fine-tune. Consolidation helps lower revolving balances, simplify payments, and strengthen your overall profile. This is especially important if you’re planning a large financing move or major investment.

Lenders often reward creditworthy borrowers with a balanced, low-risk profile. The more disciplined and predictable your credit behavior appears, the stronger your negotiating position becomes.

Debt consolidation can position you for better terms on new and existing debt

Even with an excellent credit score, consolidation of debt can increase your score further by 40 to 50 points within 1 month of the consolidation. It’s a smart move to make if you will soon be seeking credit for a new car, new property, or student expenses, as it can potentially save thousands of dollars.

With an improved credit score after consolidating, borrowers should also explore taking advantage and refinancing any debts they did not consolidate. Consolidation can be used to kick off a positive domino effect, resulting in better terms across all of your existing debts.

3 ways debt consolidation can improve a strong credit score

1. Lowers your credit utilization ratio

One of the fastest ways consolidation can impact your score is by reducing credit utilization—the percentage of revolving credit you’re currently using.

FICO reports that utilization accounts for roughly 30% of your total score, and reporting agencies generally favor those who limit the amount of credit they’re using to less than 30% of their total available credit. However, many professionals exceed that threshold by charging large expenses to credit cards, even if they pay consistently.

When you move that revolving debt into a fixed-rate personal loan, your utilization on those cards drops immediately, improving your score and eliminating unpredictable interest charges.

Example:

If you have $40,000 across several cards with $50,000 in available credit, your utilization sits at 80%. Consolidating that into a personal loan drops your revolving utilization to nearly zero—often resulting in a measurable credit score boost within a few reporting cycles, as long as you don’t carry new balances on the cards after paying them off.

2. Creates a more predictable payment history

Your payment history makes up the largest portion of your FICO score—about 35%. That means even one missed or late payment can hurt your profile.

Consolidating your balances into one fixed monthly payment helps minimize that risk. With fewer due dates to track and one predictable payment schedule, you can better ensure consistent on-time payments while also reinforcing the strongest signal of creditworthiness.

3. Diversifies your credit mix

Credit scoring models also look at your credit mix, which refers to the variety of credit types you manage. Most high earners have heavy exposure to revolving credit through multiple personal cards and lines of credit.

Adding an installment loan, like a personal loan for debt consolidation, adds healthy diversification to your profile, which may slightly improve your score over time.

Most borrowers who consolidate debt through BHG improve their FICO score by 30 points or more within a few months of funding.

When debt consolidation makes sense for high earners with good credit

You’re managing debt, but paying a premium in interest

Professionals often carry large balances intentionally—but if those balances are on high-interest credit lines, they may be costing you more than is necessary.

According to the Federal Reserve, the average APR on all credit card accounts recently reached 21.16% and premium rewards cards often exceed that.

Take a look at your current APRs. If your balances are getting harder to manage, or your card rates are above average, it may be worth trying to lower it. Consolidating them into a fixed-rate personal loan can reduce interest costs and redirect more money toward your goals.

Read more:

How Do You Get the Credit Card Company to Lower Your Interest Rate?

You’re planning a large financial move

Debt consolidation can clean up your credit profile before applying for a mortgage or major investment (lower utilization and simplified finances). It can also free up cash flow, allowing you to allocate funds toward down payments, everyday expenses, or investment contributions without straining liquidity.

You value efficiency and simplicity in your finances

For those managing demanding careers and family obligations, one fixed monthly payment can reduce stress and minimize mistakes. A consolidated structure not only saves time but also brings clarity—making it easier to plan, automate, and stay in control of your broader financial strategy.

Why BHG’s personal loan is the strategic choice for high performers

Designed for high-income earners with strong credit

Unlike traditional lenders that rely solely on a credit score, BHG Financial takes a more holistic approach—evaluating your professional credentials, income history, and financial stability. This means your success and earning potential count toward your approval and loan terms.

Large loan amounts for meaningful consolidation

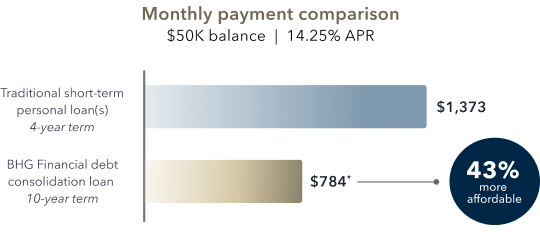

With personal loan amounts up to $250,0001 and terms up to 10 years,1,2 BHG allows you to consolidate multiple accounts—credit cards, personal loans, or lines of credit—into a single, predictable payment.

For example, consolidating $50,000 across several accounts can lower your total monthly payments by 42% and extend your repayment timeline. This helps you maintain liquidity while systematically paying down your balance.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* BHG monthly payment based on BHG’s minimum available APR for a 10-year term, which is 14.25% as of 05/13/26 and includes an origination fee. Your actual loan size, loan term, and monthly payment amount may vary based on your individual credit profile and other information provided in your loan application. Terms subject to credit approval.

Fast, confidential, credit-safe application process

BHG’s prequalification process takes minutes and has no impact on your credit score.3 You’ll receive a personalized offer tailored to your financial profile, supported by U.S.-based lending specialists who understand the demands of high-earning professionals.

From application to funding in as few as five days,4 the process is streamlined for speed, security, and discretion.

Most borrowers who consolidate debt through BHG improve their FICO score by 30 points or more within a few months of funding.

Beyond the score: Other benefits of strategic debt consolidation

More liquidity, more options

Reducing your high-interest payments can immediately improve cash flow. That freed-up capital can be reallocated toward strategic goals—such as investing, expanding your business, or optimizing tax planning.

Consolidation also helps preserve flexibility, ensuring your cash is available when opportunities arise.

Future-proofing your financial profile

A stronger score positions you for better rates, more leverage, and higher loan limits in the future.

Consider this example:

The difference between a “good” credit tier and an “excellent” one could mean qualifying for an 11% APR instead of 14%. On a $100,000 loan over seven years, you could save more than $13,500 in interest.

|

Loan amount |

APR |

Monthly payment |

Total interest |

|---|---|---|---|

|

$100,000 |

11% |

$1,712 |

$43,828 |

|

$100,000 |

14% |

$1,874 |

$57,416 |

Peace of mind during unpredictable markets

Lenders tend to tighten their requirements in times of economic uncertainty, which can make it harder for even qualified borrowers to secure favorable terms. Streamlining your credit profile through consolidation can strengthen your approval odds with lenders, giving you more options and stability regardless of market conditions.

Key questions for high earners considering consolidation

Before deciding whether to consolidate, it helps to take a step back and look at the bigger picture of your financial goals and obligations.

- Are you using credit strategically—but paying more than you should? Even when debt supports growth, it still pays to minimize cost. Lowering your interest rate can translate into thousands in long-term savings.

- Would a simplified credit profile support your next big move? Consider upcoming opportunities and whether you have your preferred cash flow and credit readiness. A consolidated profile can improve your approval odds and borrowing power.

- Do you have the credit strength to qualify for the best terms? If so, you’re in a strong position to act now before rates fluctuate or balances increase. Your excellent credit gives you access to premium loan structures designed for high-income earners like you.

Final thought: Use consolidation to strengthen what you’ve already built

Consolidating debt can help turn strong credit into even greater financial flexibility. Whether you’re planning a large purchase or simply want more control over your cash flow, streamlining balances can strengthen your overall credit health and expand what’s possible with your next major financial move.

Already have great credit? Use it strategically. See how a BHG personal loan can consolidate your debt and strengthen your profile—with no impact on your credit score.3

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

*Based on internal data, most BHG debt consolidation borrowers may improve their FICO® score by 30+ points within 2 months. Credit scores depend on many factors and individual results may vary based on personal spending habits.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

4 This is not a guaranteed offer of credit and is subject to credit approval.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829