Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Signs You’re a Strong Candidate for a Debt Consolidation Loan

You’ve worked hard to build success—whether through your career or strategic investments—and you manage your finances with intention. Still, juggling multiple high-interest balances or accounts can make even a strong financial picture feel cluttered.

Many people are turning to debt consolidation loans for high earners as a way to simplify payments and strengthen their overall strategy.

If you’re wondering whether it’s the right time, here are the key signs you’re ready to consolidate debt—and who the ideal borrower is for these types of loans.

First, let’s set the record straight: Debt consolidation isn’t just for people in trouble

It’s a tool for optimization, not just recovery

Professionals with strong credit and multiple financial obligations often use personal loans to consolidate their debt and regain control over their finances. Many use consolidation to:

- Combine multiple high-interest balances into a single, manageable payment

- Lower monthly obligations to free up liquidity for investments, renovations, or everyday needs

- Streamline their financial lives, making it easier to track and plan for long-term goals

Strong credit? Strong income? You might be the ideal fit

Borrowers with solid credit and consistent income are in the best position to make debt consolidation work to their advantage. Building credit and financial strength isn’t just smart—it’s strategic. With strong credit and consistent income, lenders can present customizable terms that can help put you in control.

Consolidation makes the most sense when you can secure better terms that either save you money, simplify repayment, or ideally, do both. By combining multiple balances into one lower-rate personal loan, you can reduce interest costs, streamline your payment schedule, and free up cash flow—all while maintaining the strong credit profile you’ve worked hard to build.

Checklist: Do these signs sound like you?

Score yourself as you go. If most of these feel familiar, it may be time to consider using a personal loan for consolidation.

✔ You have excellent or good credit (680+)

If your score is 680 or higher, you’re already in a position to use credit strategically. A debt consolidation loan for high earners can help you turn that strong foundation into measurable savings by securing better loan terms, lowering interest costs, and reducing monthly stress.

Borrowers with good credit typically qualify for a personal loan with APRs between 11% and 14%. This is substantially lower than the average credit card APR, which currently hovers just above 21%, as reported by the Federal Reserve. Such significant differences in APR alone can make consolidation worth considering.

Read more: Does Debt Consolidation Hurt Your Credit?

✔ You earn a high income, but want better cash flow

Earning six figures can feel like financial freedom—until you’re juggling credit cards, student loans, and other obligations. Even high earners can face cash flow challenges when monthly debt obligations pile up.

If you’re earning a sizable income but facing liquidity restraints, debt consolidation lets you reorganize payments and reduce interest expenses to create more monthly breathing room. This frees up money for priority goals, whether that’s paying down debt, upgrading your home, or funding your child’s education.

✔ You carry multiple balances—strategically or otherwise

Maybe you’ve spread balances across cards or short-term financing plans to maximize rewards or minimize monthly payments. Over time, this can become inefficient.

Consolidation simplifies your payment structure, letting you track a single loan and know exactly when your debt will be paid off.

✔ You’re paying more than 15% APR on some balances

High-interest debt silently erodes your cash flow. Even one card with an APR above 15% can cost thousands over time if you carry a balance month to month. If you have credit card APRs that are higher than average, or other high-rate debt straining your budget, consolidating with a fixed-rate personal loan can lower these costs and improve predictability.

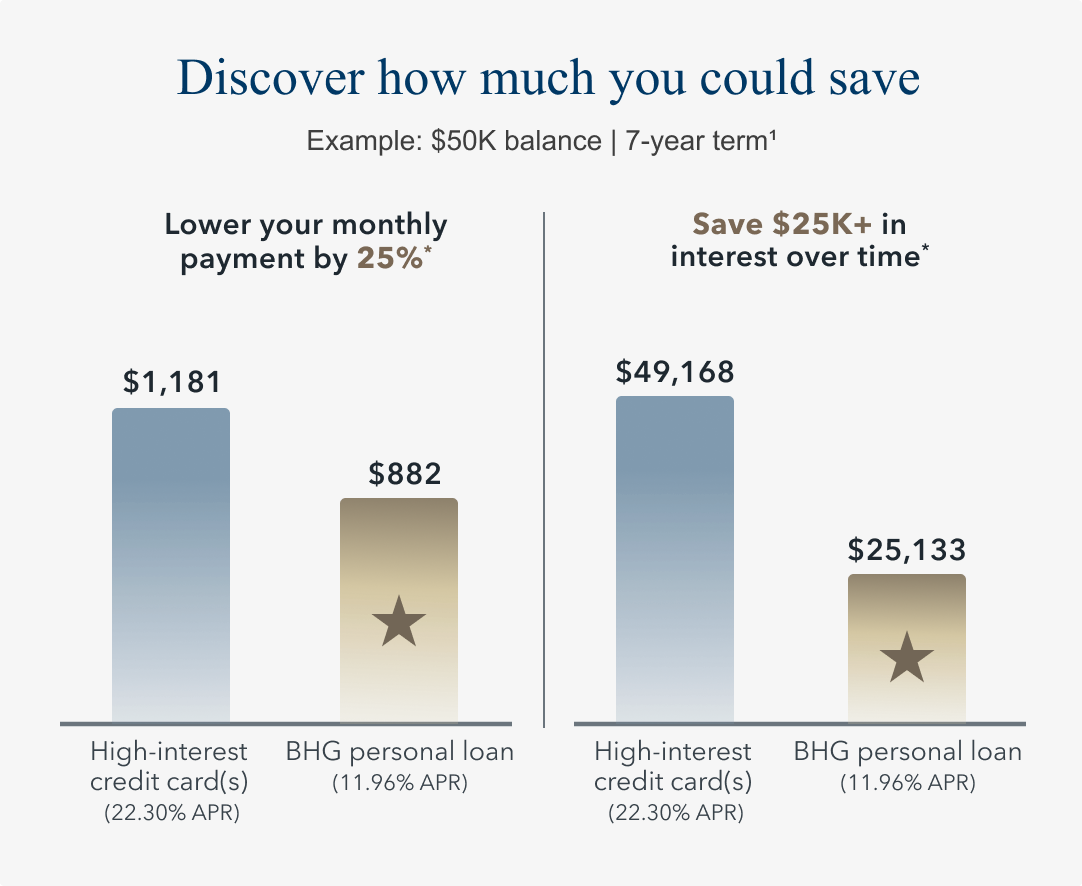

Here’s how the math works out if you were to take out a personal loan of $50,000 with a 7-year term to consolidate debt.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $50,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,181 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $882 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

✔ You value efficiency and control in your finances

One loan. One payment. One rate. Consolidation simplifies your financial life, giving you control and visibility. Instead of juggling multiple due dates and fluctuating interest rates, you can focus on higher-level goals—investments, growth opportunities, or family expenses—without distraction.

✔ You’re planning a big financial move in the next 6–12 months

Debt consolidation may be a good idea if you’re planning to make a big financial move in the near future, such as:

- Purchasing a second home or vacation property

- Renovating your primary residence

- Renovating your primary residence

- Funding a child’s college tuition

Cleaning up your financial picture in advance gives you a competitive edge. By consolidating balances, you can lower your credit utilization ratio, which can improve your credit score over time and give you better borrowing power to pursue large investments or major life goals.

✔ You want to maximize liquidity without sacrificing progress

Take stock of your progress toward your priority goals, including debt management. How are you faring? Consolidation helps create flexible cash flow by lowering monthly debt payments without compromising liquidity. This allows you to redirect funds toward:

- Investment portfolios or retirement accounts

- Entrepreneurial ventures or side projects

- Unexpected personal expenses

FYI: BHG Financial’s large personal loans for debt consolidation are unsecured, meaning you don’t have to put up collateral or assets to secure the funds.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Bonus signs you’re an ideal BHG personal loan candidate

If you’re considering consolidation, BHG may have what you need to do it wisely. Here’s how to tell if you’re ready to leverage BHG’s personal loans for professionals and higher earners:

✔ You prefer working with a lender that understands successful people

When evaluating loan applications, BHG considers your full financial picture—income, career background, and earning potential—not just credit score. This holistic approach ensures the loan fits your financial reality and long-term goals.

✔ You need a loan size that matches your financial life

BHG offers high unsecured loan amounts up to $250,0001 with industry-leading repayment terms up to 10 years,1,2 ideal for consolidating larger balances while keeping monthly payments manageable. This flexibility allows borrowers to handle multiple obligations in one streamlined solution.

✔ You want speed, privacy, and a professional experience

With BHG, you can prequalify in minutes with no impact on your credit score.3 Funding is fast4, confidential, and tailored to your timeline, helping you take action without disrupting your life or professional focus.

Learn more: The Best Personal Loans for Prime Credit Borrowers with Debt

How many boxes did you check?

- 0–2 boxes: You might not be ready just yet—but check back after reviewing your debt picture.

- 3–5 boxes: You’re likely a strong candidate. Prequalify with BHG and then compare your estimate4 with offers from other lenders to see if consolidation could create significant savings and control.

- 6+ boxes: You’re the ideal BHG borrower. It’s time to take the next step and get your instant personal loan offer.

You’ve worked hard to build a strong financial position. Debt consolidation is a tool to protect, optimize, and strengthen it.

A BHG personal loan offers high loan amounts, flexible terms, and a streamlined process that respects your time. Funding in as few as five days4 means you can act when the opportunity arises, keeping cash where it’s most useful.

Ready to consolidate like a pro? See what you qualify for with a BHG personal loan—no credit impact3, just clarity.

Check my rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

4 This is not a guaranteed offer of credit and is subject to credit approval.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829