Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Financial Red Flags for the Sandwich Generation: Signs You’re Overextending Your Budget

Table of Contents

- Why budget overextension is so common for the sandwich generation

- Red flag #1: You’re relying on high-interest credit cards to cover monthly expenses

- Red flag #2: You’re missing savings targets (or not saving at all)

- Red flag #3: Your monthly payments keep rising due to variable interest rates

- Red flag #4: You’re frequently borrowing from retirement accounts

- Red flag #5: Medical or caregiving bills are consistently unexpected

- How BHG’s personal loan can help you regain control

- How to course-correct when you spot these red flags

- Final thoughts: You don’t have to manage these pressures alone

- Check my rate

If your budget feels tighter despite a solid income, the strain may not be your spending—it may be the weight of supporting multiple generations at once. Many members of the sandwich generation—adults caring for both dependent children and aging parents—find that budget overextension isn’t caused by poor money habits. It’s the result of carrying multiple responsibilities at once, often without a clear roadmap.

This article breaks down the most common financial red flags facing the sandwich generation, why they show up, and how to course-correct before short-term strains turn into long-term risk.

Why budget overextension is so common for the sandwich generation

The sandwich generation sits at the intersection of two major financial commitments: caring for children who rely on you and parents who increasingly need support. These obligations overlap, escalate, and often arrive with little warning.

Many professionals in this stage are in their peak earning years, yet cash flow feels tighter than ever. Income may be strong, but outflows are constant, emotional, and unpredictable—making it harder to plan, save, and adjust in real time.

The emotional expectations behind overspending

Overspending in the sandwich generation is largely driven by the pressure to show up fully for everyone—to help an aging parent maintain dignity, to give children stability and opportunity, and to avoid being the one who says “no” when needs arise. That emotional load can quietly influence financial decisions.

Over time, these decisions can stack up. Without a proactive plan, emotion can override structure—and budgets begin to stretch past their limits.

Hidden costs of multigenerational care

The financial impact of caregiving rarely shows up in one place. Instead, it spreads across everyday spending and adds pressure in ways that are easy to underestimate, such as:

- Transportation to medical appointments or school activities

- Groceries for larger or multigenerational households

- Out-of-pocket medical costs and insurance premiums

- Emergency travel or temporary caregiving arrangements

- School-related tuition, activities, supplies, and other expenses

Raising children alone is a significant financial commitment. A Brookings Institution analysis estimates that parents will spend an average of $310,605 to raise a child born in 2015, adjusted for inflation. Add eldercare to the equation, and the financial pressure compounds quickly.

According to AARP, family caregivers spend 26% of their income on caregiving-related activities. For high earners, that percentage can translate into tens of thousands of dollars annually—often absorbed quietly through credit cards or deferred savings.

A recent Harris Poll found that nearly 1 in 3 six-figure earners say they feel stretched, struggling, or drowning financially. Among the top expenses draining income: supporting extended family, childcare, groceries, and credit card or loan payments.

Caregiving also affects earning power. Time away from work, reduced hours, or stalled career progression can limit income growth right when financial demands peak.

Red flag #1: You’re relying on high-interest credit cards to cover monthly expenses

Using credit cards occasionally is common. Relying on them month after month to bridge budget gaps is a warning sign.

Why this happens to the sandwich generation

Caregiving costs fluctuate. One month may include routine expenses; the next may bring medical bills, travel, or unexpected support for an adult child. When cash flow can’t flex fast enough, credit cards become the default solution.

Three-quarters of six-figure earners used a credit card in the past three months, not for rewards, but because cash was tight, per the Harris Poll. Over time, this pattern can quietly erode credit health and make everyday finances more expensive.

Consequences of high utilization rates

High balances create more than interest expense. They affect:

- Credit utilization, which can lower your credit score

- Monthly cash flow, as minimum payments rise

- Financial flexibility, limiting future borrowing options

As balances grow, so does volatility. Variable APRs mean payments can increase even if spending doesn’t—making budgeting harder at an already demanding life stage.

When debt consolidation becomes a strategic fix

Consolidating high-interest credit card balances into a single, fixed-rate loan can be a practical step toward regaining control. Instead of juggling multiple payments and variable rates, consolidation offers structure: one payment, one timeline, and clearer visibility into debt payoff.

FYI: With loan amounts up to $250,000,1 industry-leading terms up to 10 years,1,2 and funding in as few as five days,3 a BHG personal loan for debt consolidation is ideal for helping you regain control and redirect resources toward long-term goals. Explore instant loan options today.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Red flag #2: You’re missing savings targets (or not saving at all)

When savings stall, vulnerability grows. Emergency funds and retirement accounts play a critical role in both future planning and everyday stability.

How caregiving duties crowd out savings

Prioritizing children or aging parents often creates what’s known as the caregiver pay gap. A joint analysis by AARP and S&P Global shows that the unpredictable nature of caregiving is one of the biggest stressors caregivers face, frequently disrupting income and limiting savings potential.

Sixty-seven percent of caregivers report difficulty balancing work and caregiving duties. As a result, 27% shift from full-time to part-time work and 16% turn down promotions. It can also pose limitations when it comes to travel or hourly availability, translating to halted career progression and earnings growth.

The impact on retirement and emergency preparedness

When income becomes unpredictable, IRA and 401k contributions are often the first thing sacrificed—even among high earners. Retirement savings need time to compound and grow, which means that pauses today can create larger gaps tomorrow. For professionals in their 40s and 50s, redirecting income away from retirement to cover every day needs can leave little margin for recovery.

In addition to retirement contributions, emergency funds are often depleted or never funded in the first place. Without adequate emergency reserves, unexpected caregiving costs are more likely to land on credit, reinforcing debt cycles, and limiting long-term progress.

Red flag #3: Your monthly payments keep rising due to variable interest rates

Rising payments without increased spending is one of the clearest signs of budget instability.

Why variable APR debt is especially risky for the sandwich generation

Variable-rate debt adds uncertainty at a time when predictability matters most. Credit card APRs—often in the double digits—can increase as market conditions change, raising monthly payments even if balances stay the same.

How fixed-rate consolidation loans offer stability

Fixed-rate personal loans replace uncertainty with consistency. Payments stay the same, timelines are clear, and interest costs are easier to anticipate.

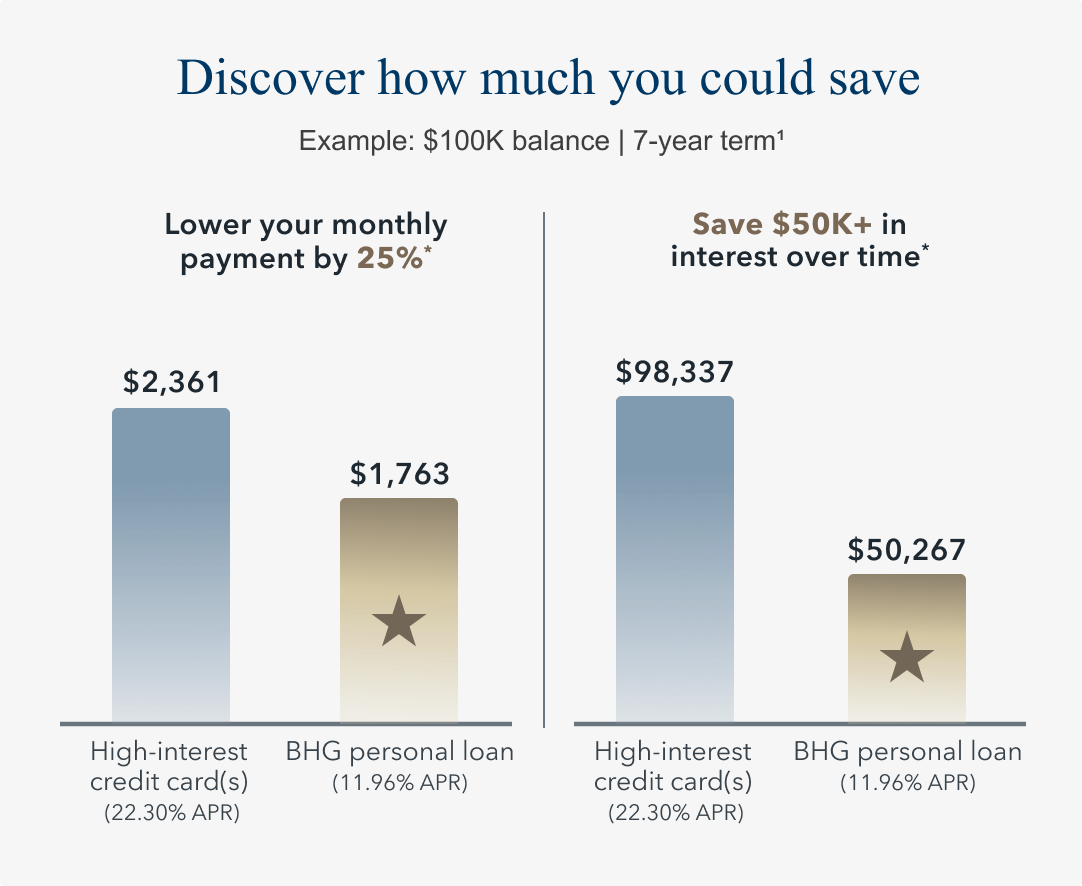

For example, shifting $100,000 in combined debt from an average 22% interest rate to a fixed 12% rate over seven years could save more than $48,000 in interest. Just as important, predictable payments create breathing room and restore planning confidence as retirement approaches or when priorities change alongside family dynamics.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $100,000 balance over 7 years on both a credit card with a minimum monthly payment of $2,361 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $1,763 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

Red flag #4: You’re frequently borrowing from retirement accounts

Retirement funds are designed for the future. Using them repeatedly to cover current needs signals deeper financial strain.

Short-term relief, long-term damage

Early withdrawals from retirement accounts can trigger tax consequences and penalties. The IRS typically imposes a 10% early withdrawal penalty on certain early distributions. These withdrawals are also subject to income taxes, reducing long-term growth and compounding losses over time. 401(k) loans (if they are even available) are limited in size and have their own negative consequences.

Read more: 401(k) Loan vs Personal Loan: Which is Right for You?

Why this signals a budget breakdown

Borrowing from retirement is rarely a first resort. Repeated withdrawals often indicate persistent cash-flow shortfalls rather than isolated emergencies—an indication that financial obligations need to be restructured.

Red flag #5: Medical or caregiving bills are consistently unexpected

Unexpected costs aren’t always avoidable. But when “surprises” happen repeatedly, they often point to planning gaps.

Why caregiving expenses spike without warning

Eldercare needs can change quickly. Medication adjustments, hospital stays, and mobility challenges can all trigger sudden costs. Eldercare alone can reach six figures when factoring in long-term care services, medical premiums, and emergency healthcare—one reason many families choose to provide care themselves, even when it strains their finances.

How to build a “caregiving contingency fund”

A caregiving contingency fund works like an emergency fund, but with a specific purpose. It can help cover:

- Travel or temporary housing

- Lost income during caregiving transitions

- Medical or caregiving services not fully insured

Planning ahead also means talking early and openly with family. Do your parents have long-term care insurance? Legal documents? A defined plan? These conversations reduce uncertainty later.

Working with a financial professional or elder care and estate attorney can clarify financial obligations to your aging parents and how to best use any savings or assets they have. For example, if an aging parent qualifies as a dependent, you may be able to increase contributions to an FSA or HSA to offset medical costs.

How BHG’s personal loan can help you regain control

For many in the sandwich generation, stability matters most. BHG’s personal loans are designed as planning tools—not quick fixes—for managing complex finances proactively.

Consolidating multiple debts into one predictable payment

Simplification reduces mental and financial friction. When you consolidate with a personal loan, your loan replaces multiple due dates, balances, and rates—making it easier to track your progress and stay on budget.

Lower monthly payments with longer terms

With terms up to 10 years,1,2 BHG loans can lower monthly payments and create immediate budget relief. That flexibility helps caregivers rebalance priorities, rebuild savings, and reduce reliance on high-interest credit.

Fixed rates for reliable planning

Unlike variable credit card APRs, fixed rates provide certainty. Predictable payments support long-term planning, helping you save or regain momentum while balancing multiple family obligations.

Example scenario: Using a personal loan to accommodate multiple priorities

Imagine you’re managing several high-interest credit cards while preparing your home to accommodate an aging parent. Rather than draining savings or stretching cash flow even thinner, you consolidate existing balances with a BHG personal loan. You also take out additional money for an emergency fund, so cash is available for unexpected expenses when you need it.

The result is one predictable monthly payment that creates breathing room—allowing you to move forward with necessary home updates and put aside some cash for future obligations while keeping your budget intact.

FYI: Most BHG borrowers (about 70%) are between the ages of 38 and 58. Our process is built for people juggling multiple priorities, with U.S.-based loan specialists who provide tailored support now and as needs evolve.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

How to course-correct when you spot these red flags

If you recognize any of these red flags, here’s how to recalibrate:

- Rebuild a realistic budget for a multigenerational household: Separate essential caregiving costs from discretionary spending, then allocate intentionally between children, parents, and personal needs. Audit expenses regularly to identify liquidity drains and opportunities to improve cash flow.

- Prioritize high-interest debt first: High-interest obligations do the most damage to cash flow and long-term progress. Addressing them first can free up resources faster and restore flexibility.

- Automate savings to rebuild stability: Even modest, automated contributions restore momentum. Consistency matters most when rebuilding financial resilience.

Final thoughts: You don’t have to manage these pressures alone

Supporting multiple generations is demanding—but it doesn’t have to derail your financial future. Spotting these red flags is an opportunity to take control, simplify, and plan proactively.

With the right strategy and planning tools, including a thoughtfully structured BHG personal loan for debt consolidation, you can create the breathing room needed to support your family while protecting your own goals.

Check my rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 This is not a guaranteed offer of credit and is subject to credit approval.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829