Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Fixed vs. Variable Interest: What’s Better When Consolidating Debt?

If you’re looking to pay off high-interest debt and exploring the idea of debt consolidation, you’ll need to choose between a fixed and variable interest rate. While the ideal option will depend on your unique situation and risk tolerance, opting for a fixed-rate option is more common because it creates a predictable payment schedule and ensures that your payments will stay the same.

Below, we’ll dive deeper into the differences between a fixed and variable interest rate as well as the benefits of debt consolidation for high earners.

Why interest type matters in debt consolidation

Consolidation is about control

There are two main benefits of debt consolidation: reducing the number of payments you need to track and the potential to get a lower interest rate. Consolidating multiple debts into a lower-rate personal loan gives you more control over your finances because it often means substituting variable-rate debt with fixed-rate financing. Not only does this ensure your interest rate doesn’t change, but it can also lower your monthly payments, reduce interest charges, and improve your cash flow over time.

The key to sustaining this type of control? Choosing the right interest structure for your loan.

High-income ≠ immune to debt traps

It’s not uncommon for six-figure earners to carry significant debt. High earners often juggle large mortgages, high tax burdens, and student loans.

They also tend to hold their assets in stocks, bonds, retirement accounts and real estate, which poses liquidity constraints. As a result, many professionals tend to lean on credit cards and other forms of financing to make ends meet. Carrying debt from month to month can quickly spiral out of control, especially if the balances are tied to high, variable-rate options like credit cards.

What is fixed interest?

When you take out a loan with a fixed interest rate, the rate you agree to at the beginning never changes. This means your monthly payments remain steady throughout the life of the loan, making it easier to plan ahead and stay on top of your finances.

How it works

Unlike variable interest rates, which can vary based on based on market fluctuations, a fixed rate is locked in when you sign your loan agreement. Your payment will stay the same even if the prime rate changes, helping you avoid surprises in your budget.

Benefits of fixed interest

Since a fixed interest structure locks in your rate and payments from the moment you finalize your loan, you can accurately predict your monthly expenses in advance and budget accordingly. Fixed interest is a huge plus if you’re concerned about rising market interest rates and prefer greater financial stability. It’s also ideal if your income varies based on business revenue, bonuses, and/or commissions.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

What is variable interest?

A variable interest rate changes over time, often based on market benchmarks like the prime rate or an index set by lenders. That means your payments can rise or fall depending on how rates shift during your repayment period.

How it works

Variable rates adjust periodically—sometimes monthly, quarterly, or annually—depending on your loan terms. When your rate goes up or down, your monthly payment adjusts with it, which can make budgeting less predictable.

Risks of variable interest

Variable interest loans can offer lower starting rates than fixed loans, which may reduce your initial payments. They also give you the chance to save if market rates drop, since your rate could decrease over time. However, the biggest risk is unpredictability. Variable rate loans don’t allow you to calculate your total loan cost in advance, making long-term financial planning a real challenge. Additionally, you might discover that increasing loan payments eventually outweigh the benefits of debt consolidation.

Fixed vs. variable: A side-by-side comparison

Here’s a closer look at how fixed and variable interest rates compare:

|

|

Fixed interest |

Variable interest |

|---|---|---|

|

Monthly payments |

Predictable |

Can fluctuate |

|

Budgeting |

Easier |

More challenging |

|

Total interest paid |

Potentially higher at first |

Potentially lower early on |

|

Risk of payment shock |

Low |

High if rates rise |

|

Stability in rising market |

Strong |

Weak |

What the data says

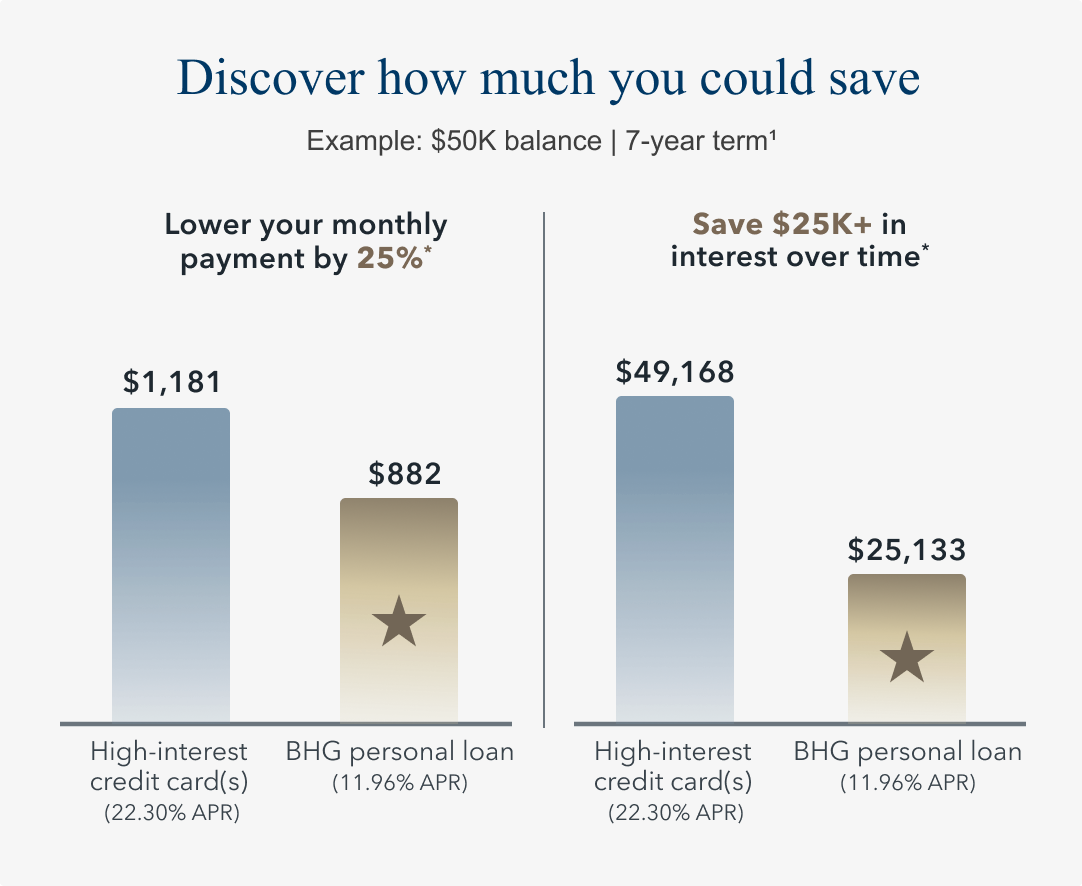

The average APR on all credit card accounts was 21.39% as of August 2025, according to the Federal Reserve. By comparison, average personal loan APRs range from 11% to 15% for borrowers with good credit. The difference in interest can result in significant savings. As such, fixed-interest rate loans tend to be more popular for borrowers who are looking for smart financing solutions. Roughly 72% of personal loans taken in 2023 had fixed rates, proving borrower preference for predictability.

FYI: BHG Financial’s personal loans for debt consolidation come with a fixed rate and industry-leading extended terms1 to help keep monthly payments low.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $50,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,181 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $882 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

For high earners, predictability is power

Cash flow management matters

The stakes are higher for professionals with higher monthly obligations and complex finances. Even small unforeseen rate hikes from variable rate loans can create ripple effects, pulling funds away from investments, business growth, or family needs. Choosing a predictable structure helps manage cash flow and preserve the wealth you’ve worked so hard to build.

Asset-rich ≠ cash-rich

Even if you own a lot of assets, such as a home, business, or investments, it doesn’t always translate to readily available cash. Preserving liquidity means opting for financing that avoids volatility, especially if you have irregular cash inflows or significant overhead costs.

Why BHG personal loans are fixed—and why that matters

BHG Financial understands the unique needs of high earners with complex financial situations. We offer fixed-rate loans that allow for predictable payments with no surprises. With us, you can enjoy:

- Higher loan amounts and no collateral: While other lenders limit how much you can borrow from as low as $1,000 to around $100,000, we offer loans up to $250,000.1 Plus, there is no collateral required.

- Flexible repayment terms: We’ll work with you to design a repayment schedule that aligns with your particular budget. BHG personal loans offer extended repayment terms of up to 10 years.1,2

- Easy application: With BHG, you can pre-qualify for a personal loan in minutes, without any effect on your credit score.3 Our knowledgeable U.S.-based concierge team is here for you throughout the application process.

- Fast funding: Upon approval, you may receive your funds in as few as 5 days.4 You won’t have to wait long to tackle your debt and/or pursue other financial goals.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Final takeaway: Choose fixed for stability and simplicity

If you’re searching for a strategic way to consolidate debt and regain financial control, a fixed interest rate is almost always the better option, especially in a high-rate economy. You’ll be able to shift away from multiple payments to one streamlined payment, simplifying your financial life, reducing monthly strain, and enjoying a great deal of peace of mind in the process.

Ready to see what’s possible? Use our quick and easy payment estimator to get your personalized loan offer in just seconds.4

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

4 This is not a guaranteed offer of credit and is subject to credit approval.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829