Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Consolidate, Save and Spend: The Loan Strategy High-Earners Are Using Right Now

Did you know that even among high-earning professionals, many borrowers find that a premium salary doesn’t always equal premium cash flow? Quite often, top earners face a paradox: despite their strong incomes, rigid repayment plans, and short loan terms can leave them financially constrained.

Plenty of high-earning professionals with prime credit have utilized personal loans to help them reach their financial goals—from covering a large purchase to consolidating debt or investing in promising opportunities. Personal loans often provide a more affordable, lower-interest alternative to high-interest credit cards. However, not all terms are created equal—shorter repayment terms may result in high monthly payments that strain cash flow.

Fortunately, there’s an easy way to create more flexibility in your budget that doesn’t involve taking on new debt: refinancing to a personal loan with longer terms. By extending your repayment period—and choosing a repayment plan that better suits your monthly budget—you can stretch out payments and ease monthly financial strain. This approach gives you more control over your finances and can help to balance your monthly cash flow.

In this guide, we will explore why even high-income professionals struggle with regular expenses, how refinancing works, and how to maximize the benefits of lower monthly payments with an optimized repayment plan.

Why High-Earners Struggle with Cash Flow

The Illusion of Financial Flexibility

A high salary doesn’t always guarantee financial flexibility. While many professionals assume that earning more money equates to greater financial freedom, the reality is often more complex. High earners frequently face significant financial obligations that limit their liquidity and ability to save.

Key factors contributing to cash flow challenges include:

- Large monthly debt payments: Many professionals carry substantial financial commitments, including personal loans, mortgages, student debt, and business investments.

- Limited savings or emergency funds: Despite strong earnings, high-income individuals often prioritize debt repayment and necessary expenses over building an emergency fund.

- Tax obligations: Higher salaries often come with a greater tax burden, which can take a substantial portion of annual earnings.

Beyond these financial commitments, high-income earners often face unique pressures related to their stage in life. Funding children's education, contributing to charitable causes, preparing for retirement, or covering business-related costs can all add up quickly. When combined, these factors can create a situation where even those with strong earning potential may find themselves short on liquidity. This is why refinancing can be a strategic move for borrowers looking to optimize cash flow and regain financial control.

The Refinancing Strategy: Same Debt, Lower Monthly Payments

How Refinancing Works

Instead of paying down a short-term personal loan—typically a term of between three to five years—you can refinance into a longer-term loan, such as BHG’s 10-year personal loan.1,2 By extending your repayment period, you not only lower your monthly financial commitment but also adopt a repayment plan that provides greater ease and predictability.

This strategy is particularly beneficial for individuals who need to free up cash for better financial planning, investment opportunities, or simply improving their overall financial well-being.

Why This Matters

- Lower monthly payments: Extending your loan term reduces your monthly payment, making it easier to manage cash flow.

- More financial breathing room: With a lower monthly payment, you can allocate funds toward high-yield investments, business growth, or personal savings.

- Improved credit utilization: Maintaining a lower debt-to-income ratio can improve your credit score over time.

- Avoid liquidating assets: Instead of selling off stocks or withdrawing from retirement accounts, you can manage your financial obligations more effectively.

- Enhanced financial planning flexibility: An optimized repayment plan allows you to adjust your financial strategy as opportunities or challenges arise.

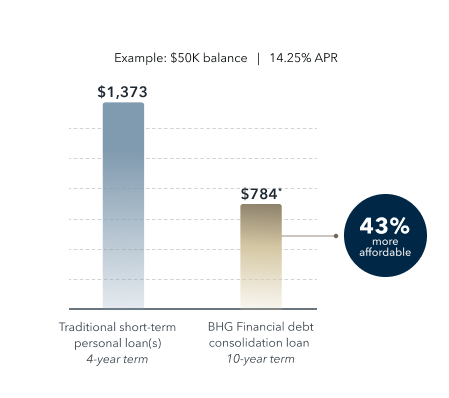

Example Calculation

Consider this scenario: You’re a high earner with excellent credit but dealing with large monthly payments on an existing personal loan. Let’s say you have a $50,000 traditional personal loan with a short term—your monthly payment could be over $1,300. But by refinancing it to a 10-year term, your payment could drop to as low as $795 per month.

Same debt but way more breathing room in your budget. That extra cash flow can be used to enjoy a little more flexibility each month, all while keeping your finances in check. Don’t let a high payment hold you back.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* BHG monthly payment based on BHG’s minimum available APR for a 10-year term, which is 14.25% as of 05/13/2026 and includes an origination fee. Your actual loan size, loan term, and monthly payment amount may vary based on your individual credit profile and other information provided in your loan application. Terms subject to credit approval.

By refinancing, you could free up thousands of dollars in cash flow each year. And even if you end up paying more in interest over the long run, the improved repayment plan and extra financial breathing room often outweigh the cost, especially when those extra funds are put to productive use.

What to Do with the Extra Cash Flow

Boost Savings and Investments

One of the most powerful benefits of refinancing is the ability to redirect your money toward building long-term wealth. Instead of having your income tied up in high loan payments, you can put your freed-up cash to work in ways that strengthen your financial future. Whether you're focused on growing your retirement savings, building an emergency fund, or seizing new investment opportunities, having extra liquidity allows you to make more strategic financial moves.

Here are some of the best ways to allocate your additional cash flow:

- Retirement accounts (401(k), IRA): Maximize contributions to secure your financial future and take advantage of tax-deferred growth.

- Brokerage investments: Deploy additional capital into stocks, ETFs, or other market opportunities to grow your wealth over time.

- Emergency funds: Strengthen your financial security with liquid savings, ensuring you're prepared for unexpected expenses.

- Real estate investments: Use the freed-up cash for down payments, property improvements, or expanding your real estate portfolio.

Reinvest in Your Business

For business owners, cash flow is everything. From scaling operations to hiring new talent or upgrading technology, additional liquidity can mean the difference between stagnation and growth. Refinancing to lower your monthly payments enables you to free up valuable capital that can be reinvested directly into your business. Instead of being tied up in high loan payments, your money can work for you—fueling expansion, boosting efficiency, and ultimately increasing profitability.

When you have more financial flexibility and a repayment plan that suits your cash flow, you can make strategic decisions that position your business for long-term success. Here are some of the ways you can reinvest your freed-up cash:

- Expand operations: Hire new staff, open new locations, or upgrade equipment.

- Marketing and advertising: Increase brand awareness and acquire more clients.

- Technology upgrades: Invest in software and automation to improve efficiency.

Looking for additional funding to grow your business even further? Learn more about BHG business loans.

Enjoy Financial Flexibility

More breathing room means more control over your budget—without feeling stretched thin. Financial flexibility gives you the power to make choices without stress. Consider reviewing your repayment plan to see how much more you could achieve with extra cash flow.

Who This Strategy Works Best For

Ideal Candidates for Refinancing

Refinancing isn’t the right choice for everyone, but it’s an excellent strategy for those looking to optimize their financial flexibility. The ideal candidates for refinancing include:

- High-income professionals with strong credit scores.

- Individuals with existing personal loans that have short repayment periods and who are seeking a better repayment plan.

- Anyone looking for increased financial flexibility while maintaining long-term financial health.

- Business owners who need more cash flow for reinvestment and growth.

If you fit into one of these categories, refinancing could be the key to unlocking a more manageable financial future.

How to Get Started with Refinancing

If you’re considering refinancing, follow these key steps to choose the right repayment plan and optimize your cash flow:

- Check your current loan terms: Review your interest rate, remaining balance, and repayment period. Understanding your existing loan structure is the first step in making an informed refinancing decision.

- Compare refinancing options: Look for extended-term loans with competitive rates, like BHG’s 10-year personal loan.1,2 Consider the total cost of refinancing, including any fees or prepayment penalties associated with your current loan, and evaluate how a new repayment plan can benefit you.

- Calculate your new monthly payment: Ensure it aligns with your financial goals. Use an online loan calculator to estimate potential savings and determine whether refinancing is the right move for your situation.

- Apply and finalize the refinance: Work with a lender that understands the needs of high-income professionals. BHG offers a streamlined application process, no credit impact for applying,3 and concierge-level service for busy borrowers.

- Put your extra cash to work: Be strategic with your newfound financial flexibility—whether that means investing or saving. Set clear financial goals for how you plan to use the extra funds and select a repayment plan that maximizes these benefits.

Refinancing a personal loan into an extended-term loan is an often-overlooked strategy that can provide high-earners with substantial financial relief. Lower monthly payments not only reduce financial strain but also open the door to greater opportunities—whether that means saving more or investing strategically. If you’re seeking a way to improve cash flow,borrowers who choose an extended repayment plan with BHG could find this to be the smart solution.

How BHG Can Help You Consolidate, Save and Spend

At BHG Financial, we believe financing should fit seamlessly into your life and goals. That’s why we offer personal loans tailored to your needs, with amounts up to $250,0001 and flexible terms of up to 10 years1,2. Consolidate your high-interest debt with a BHG loan designed to help you move forward confidently—while selecting a repayment plan that suits your financial circumstances. Plus, you’ll enjoy dedicated, U.S.-based concierge service that works around your schedule because your time is valuable. Ready to see what’s possible? See your personalized offers in just seconds.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

Annual percentage rates (APRs) for personal loans range from 6.49% to 28.89%, with terms from 2 to 10 years.

No application fees, commitment, or impact on personal credit to estimate your payment.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

IMPORTANT INFORMATION ABOUT ESTABLISHING A NEW CUSTOMER RELATIONSHIP

To help the government fight the funding of terrorism and money laundering activities, Federal law requires all financial institutions to obtain, verify and record information that identifies every customer. What this means for you: When you apply for a loan, we will ask for your name, address, date of birth, social security number and other information that will allow us to identify you. We may also ask to see your driver's license or other identifying documents. If all required documentation is not provided, we may be unable to establish a customer relationship with you.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829