Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

What Is Prime Credit?

A strong credit score does more than unlock better interest rates. For many high-earning professionals, prime credit is the qualifying factor that allows them to access larger loan amounts, more flexible terms, and strategic financing solutions. “Prime credit” refers to a credit score that signals to lenders that you’re a low-risk borrower—someone with a history of paying obligations on time and managing debt responsibly.

Lenders classify borrowers into groups such as prime, super-prime, near-prime, and subprime (based on credit-scoring models defined by FICO® and VantageScore®) because these tiers help them predict how likely someone is to repay a loan based on past behavior.

A prime borrower is statistically less likely to default, which is why they’re offered more competitive terms and higher approval odds. A subprime borrower, on the other hand, presents higher risk—resulting in higher APRs and stricter requirements.

Let’s explore how prime credit is determined—and how it can shape your financial opportunities.

Understanding credit tiers and what "prime" means

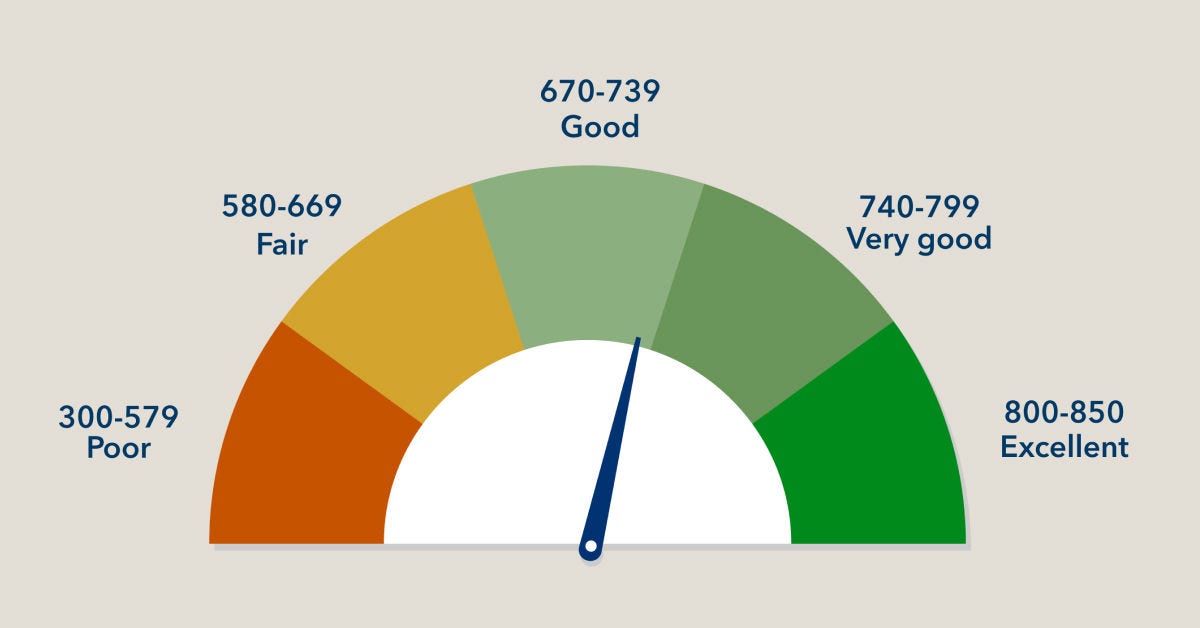

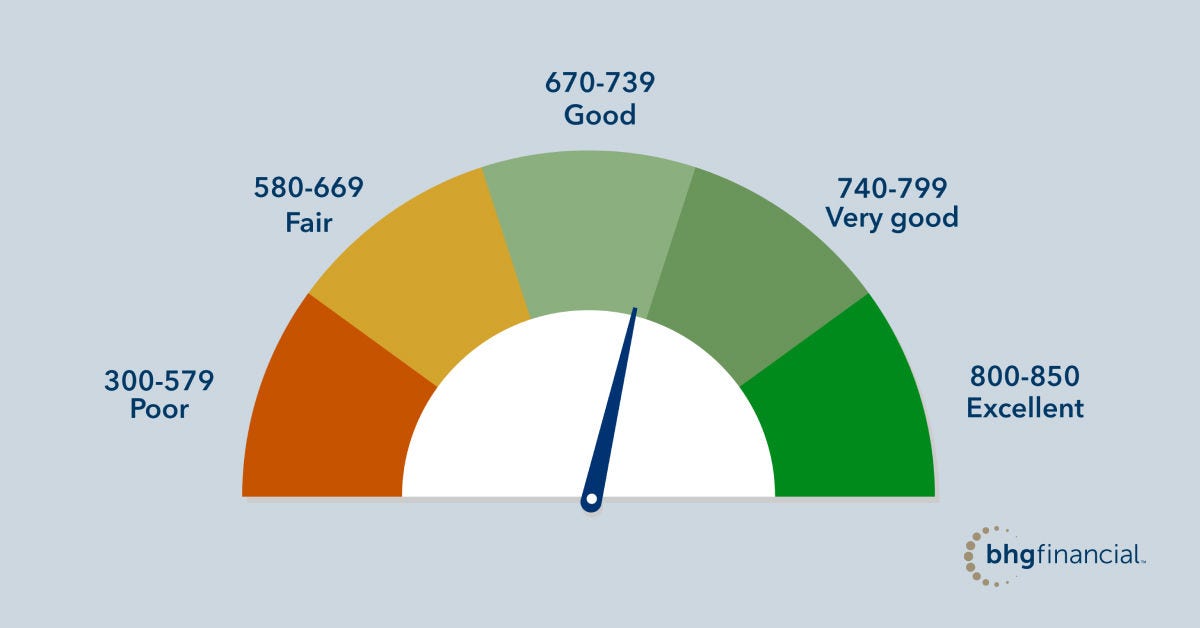

FICO®—the most widely used scoring model—categorizes credit scores into five ranges:

- Poor (300 to 579): Well below U.S. averages; approval less likely.

- Fair (580 to 669): Below U.S. averages, but approval is possible with higher terms.

- Good (670 to 739): Slightly above U.S. averages; approval likely.

- Very Good (740 to 799): Above U.S. averages; signals you are a dependable borrower.

- Excellent (800 to 850): Well above U.S. averages; lenders view you as an exceptional borrower.

Prime borrowers generally fall in the 670 to 739 FICO band, with very good and excellent borrowers often classified as super-prime. The Consumer Financial Protection Bureau (CFPB) and VantageScore® consider scores of 660 and 661 to be prime. Borrowers in the prime and super-prime tiers have significantly lower delinquency rates than those in fair or poor credit tiers.

Lenders view prime borrowers as:

- Low risk: They’ve demonstrated reliable financial behavior over time.

- Predictable: Their balances, income, and payment history show stability.

- Creditworthy: They qualify for larger loan amounts and longer repayment terms.

For example, someone with a 720 score may qualify for lower APRs and more flexible terms compared to someone with a 640 score—even if both earn strong incomes. That’s because credit scores provide lenders with a quick, standardized snapshot of risk.

How prime credit affects interest rates and approvals

Better credit leads to lower rates and higher approval odds, especially for personal loans and credit cards. In fact, FICO’s inaugural FICO® Score Credit Insights Report suggests that lenders’ tightening underwriting standards may be why personal loan delinquencies have begun to decline from recent peaks.

Borrowers with excellent credit often receive APRs significantly lower than those with fair credit—sometimes by 10 to 15 percentage points. For prime borrowers, this equates to significant savings.

For instance, let’s say you have a $100,000 personal loan with an APR of 12%—terms awarded to you based on your prime credit status. Your total borrowing costs will be much lower than if you were to qualify for the same loan with a higher APR of 19%.

- Monthly payment at 12% APR: $1,765

- Total interest over 7 years: $48,282

- Monthly payment at 19% APR: $2,160

- Total interest over 7 years: $81,507

Higher scores also improve approval odds for unsecured loans that don’t require collateral to secure the funds. This is where BHG stands out.

“At BHG, we take a holistic approach when evaluating credit, considering a wide range of factors to understand each applicant’s complete financial picture. While we look at many variables, we have a particular appreciation for prime credit,” says Tyler Powell, Vice President of Analytics at BHG.

“Applicants with strong credit histories demonstrate consistent financial responsibility and reliability, qualities that align with our commitment to sound lending practices and long-term partnerships. Prime credit often reflects stability, which helps us make confident lending decisions that benefit both our clients and our portfolio.”

BHG’s personal loans reward strong credit with large, unsecured loan amounts up to $250,0001 and fixed terms up to 10 years.1,2

Prime borrowers benefit from predictable monthly payments and the ability to consolidate multiple debts into a single, streamlined solution.

How prime credit is determined

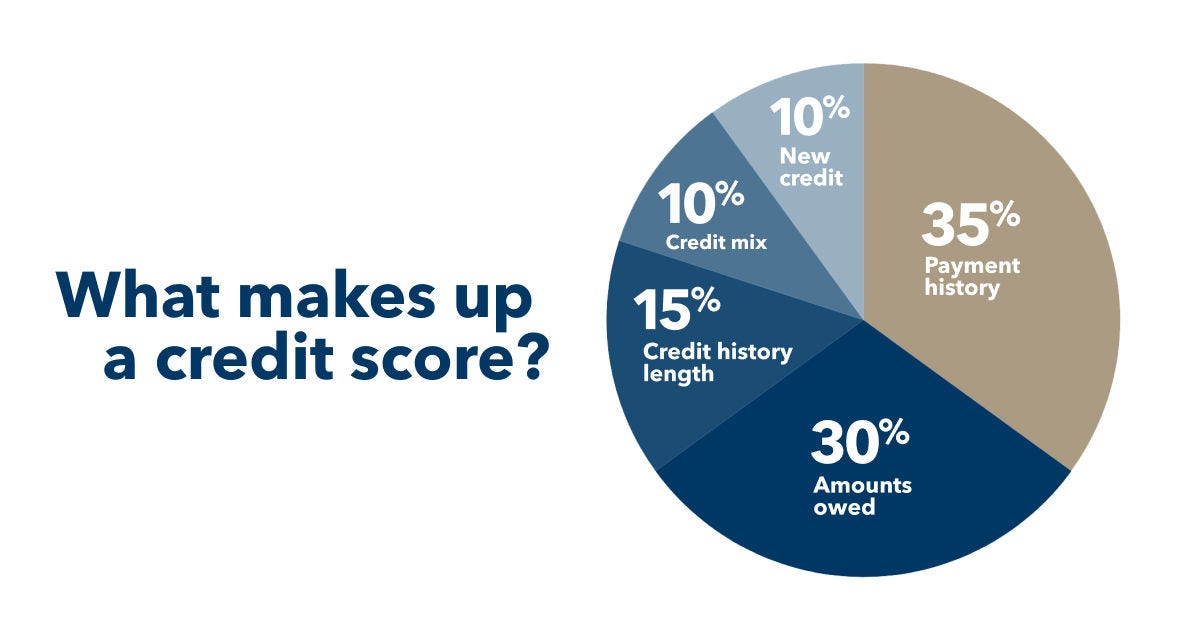

Your credit score is calculated using five main factors. Understanding these can help you maintain prime status or work your way toward it.

- Payment history (35%): Paying on time is the most influential factor. A single late payment can drop a strong score by dozens of points.

- Credit utilization (30%): This measures how much of your available revolving credit you use. For example, if you have a $30,000 credit limit and carry a balance of $9,000, your utilization is 30%. Lower utilization (below 30%) supports prime credit.

- Length of credit history (15%): Older accounts (i.e., how long you’ve demonstrated responsible borrowing habits) help build trust with lenders.

- Credit mix (10%): A blend of installment loans and revolving credit is ideal for maintaining a high score.

- New credit inquiries (10%): Multiple applications in a short period can temporarily reduce your score.

Behaviors that build prime credit include paying every bill on time each month, keeping balances low relative to credit limits, and using installment loans responsibly to manage and reorganize debt.

On the other hand, harmful behaviors include frequent late payments, maxing out credit cards, and rapidly accumulating new debt.

Tools and habits to maintain prime credit

Maintaining prime credit becomes much easier when your systems support consistent habits. A few intentional practices like the ones below can keep your score strong and help you avoid the stress that comes with juggling multiple accounts.

- Create a structured budget: Outline your monthly inflow and fixed obligations so you always know what’s coming and going. This helps prevent unintentional overspending, especially during months with irregular income.

- Automate payments: Setting bills on autopay ensures you never miss a due date, protecting the most important factor in your score—your payment history.

- Monitor your credit report: Use AnnualCreditReport.com to identify errors, outdated accounts, or fraudulent activity before they affect your score.

- Consolidate high-interest debt responsibly: Streamlining multiple payments into one predictable installment loan can lower your utilization, simplify your financial life, and help you avoid the high-interest debt trap.

If you’re managing multiple debts, a BHG personal loan for debt consolidation can help simplify your finances. Check your rate in seconds3, with no impact to your credit score.4

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Benefits of having prime credit

Having prime credit can make borrowing less expensive. But more importantly, it expands your financial freedom, giving you access to better loan options that support your liquidity needs and long-term goals.

Key benefits include:

- Lower interest rates: You’ll pay less to borrow, which is especially valuable when taking out larger personal loans or seeking extended repayment terms.

- Higher credit limits: Lenders are more comfortable offering higher limits to prime borrowers, giving you more flexibility to manage cash flow or fund larger projects.

- Easier loan approvals: Prime credit helps reduce documentation requirements and makes approvals for mortgages, auto loans, and personal loans more straightforward—without needing to pledge collateral.

- More negotiating power: Lenders often compete harder for prime borrowers, which may strengthen your borrowing power over time.

How BHG rewards prime credit borrowers

BHG is built for high-credit, high-income professionals who expect more from their lending experience. Instead of one-size-fits-all solutions, BHG offers one of the largest unsecured personal loans in the industry—up to $250,0001—with competitive fixed rates and repayment terms of up to 10 years.1,2

These extended terms create predictable monthly payments that support better long-term financial planning, especially for borrowers who want to simplify their debt or improve cash flow without sacrificing liquidity.

With BHG, prime credit borrowers can also check their eligibility with no impact on their credit score,4 making it easy to explore options confidently and without pressure.

What to do if you’re not yet in the prime range

If your score falls in the “near-prime” category—typically 620 to 669—you’re not alone. Nearly 34% of consumers fell within the middle ranges (600 to 749) in 2025, FICO® reports.

Many high earners end up here due to higher credit utilization across multiple revolving accounts. Near-prime borrowers often face higher APRs, lower approval odds, and stricter personal loan requirements.

The good news? Scores in this range can improve quickly with the right steps. Here’s how to strengthen your credit profile:

- Reduce revolving balances: Paying down credit cards lowers your utilization ratio—a major driver of credit score increases.

- Correct inaccurate information: The Consumer Financial Protection Bureau found that 27% of Americans have an error on their credit report serious enough to affect their creditworthiness. Addressing these can improve your score quickly.

- Maintain consistent payment history: Set reminders or use autopay to ensure you build a track record of one-time payments.

- Avoid closing old accounts: Longer credit history supports higher scores.

- Limit new credit inquiries: Avoid opening multiple new accounts within a short window. If you do need to secure financing, make sure you borrow with intention—for example, to consolidate high-interest debt or fund home improvements.

Using a personal loan to improve credit health

A personal loan can play a strategic role in improving your credit—especially when used to consolidate credit card balances. It also helps you preserve liquidity, so you keep more cash available for immediate needs, rather than tying it up in several high-interest revolving accounts.

A BHG personal loan can help you:

- Reduce your utilization ratio: Credit cards are revolving accounts. Paying them off with an installment loan lowers utilization, which is a major credit score factor.

- Replace multiple due dates with one predictable payment: This reduces the risk of missing a payment.

- Pay off debt with a clear timeline: Fixed terms help you build momentum toward financial stability.

The bottom line: Why prime credit matters

Prime credit gives you options: it helps you access lower rates, qualify for higher loan amounts, and move through the lending process with confidence. Most importantly, it positions you to make smart decisions that support long-term progress—whether you’re consolidating high-interest debt, preparing for a major purchase, or optimizing your cash flow.

Responsible borrowing is essential to maintaining prime credit. That means using tools that simplify repayment, reduce financial pressure, and provide predictable outcomes.

If you’re ready to simplify your debt and strengthen your credit, explore BHG’s personal loan options today.

Check your rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 This is not a guaranteed offer of credit and is subject to credit approval.

4 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829