Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Debt as a Growth Strategy: When Borrowing Makes Financial Sense

Table of Contents

- Debt isn’t automatically bad—it depends on the outcome

- What strategic debt looks like for high-income earners

- The real question: Does this debt improve your financial position?

- When borrowing makes sense: Common strategic scenarios

- When borrowing doesn’t make sense

- Why debt consolidation can be a growth strategy (not just a rescue plan)

- Choosing the right consolidation loan: What to look for

- A smarter way to simplify debt without derailing your financial goals

- Final takeaway: The goal isn’t “no debt”—it’s better debt

- Check my rate

Every borrowing decision shapes your financial future. At some point, you’ll pause and ask, “Would taking on new debt actually improve my position?”

Whether you’re reviewing your overall debt structure or considering ways to simplify higher-rate balances, the math isn’t always obvious. You may have strong earnings and growing assets, but still feel pressure in your monthly cash flow—multiple payments, variable rates, and due dates scattered across the calendar. You’re not struggling—but you’re not fully flexible either.

In situations like this, restructuring, or even strategically adding debt can strengthen your financial position if it improves cash flow, protects liquidity, or supports long-term wealth building.

Debt isn’t automatically bad—it depends on the outcome

Conventional wisdom often pushes a single goal: eliminate all debt as fast as possible.

That approach works in some situations. In others, aggressively paying down debt can reduce liquidity, limit flexibility, or disrupt long-term wealth-building. Financial decisions are rarely that simple. Rather than asking, “Is debt good or bad?” the better question is, “Does this structure help me move forward?”

Why “debt-free at all costs” isn’t always the best goal

Imagine using a large portion of your savings to wipe out a low-rate mortgage. Removing the expense from your balance sheet feels like a win. But doing so may leave you with thinner emergency reserves, fewer liquid assets available for opportunities, or tax consequences if investments must be sold to generate cash.

Liquidity is protection. It allows you to respond to opportunity and uncertainty without scrambling.

Many high earners hold a significant share of their wealth in retirement accounts, business equity, or real estate—assets that aren’t easily converted to cash without penalties, taxes, or interrupting long-term growth.

In these situations, maintaining structured, affordable debt while preserving liquidity can provide greater resilience than aggressively eliminating every balance.

The difference between reactive debt and strategic debt

Debt is often categorized as “good” or “bad” based on affordability metrics such as interest rates and repayment terms. But that framework overlooks other factors, like opportunity cost and how the debt fits into your broader financial strategy.

To determine whether your debt is helping or hindering your progress, measure it as reactive or strategic.

Reactive debt tends to be:

- Accumulated without a defined payoff strategy

- Carried on revolving accounts with high variable APRs

- Structured around fluctuating minimum payments with no clear end date

Reactive debt—such as high-rate revolving credit—creates drag on your monthly budget. It absorbs cash flow and introduces unpredictability.

Strategic debt, by contrast, is more intentional:

- Used for a defined purpose, such as consolidation or home improvements

- Designed to produce measurable improvements, like lower interest exposure or more affordable payments

- Structured intentionally, often with fixed rates and clear repayment timelines

What strategic debt looks like for high-income earners

Rather than labeling debt as inherently good or bad, consider evaluating it through these strategic lenses: cash flow, stability, and long-term positioning.

Debt that improves your monthly cash flow

Cash flow is the foundation of financial momentum. Debt that increases monthly flexibility can be strategic. A good example of this is turning high-rate variable debt into fixed, predictable payments using debt consolidation.

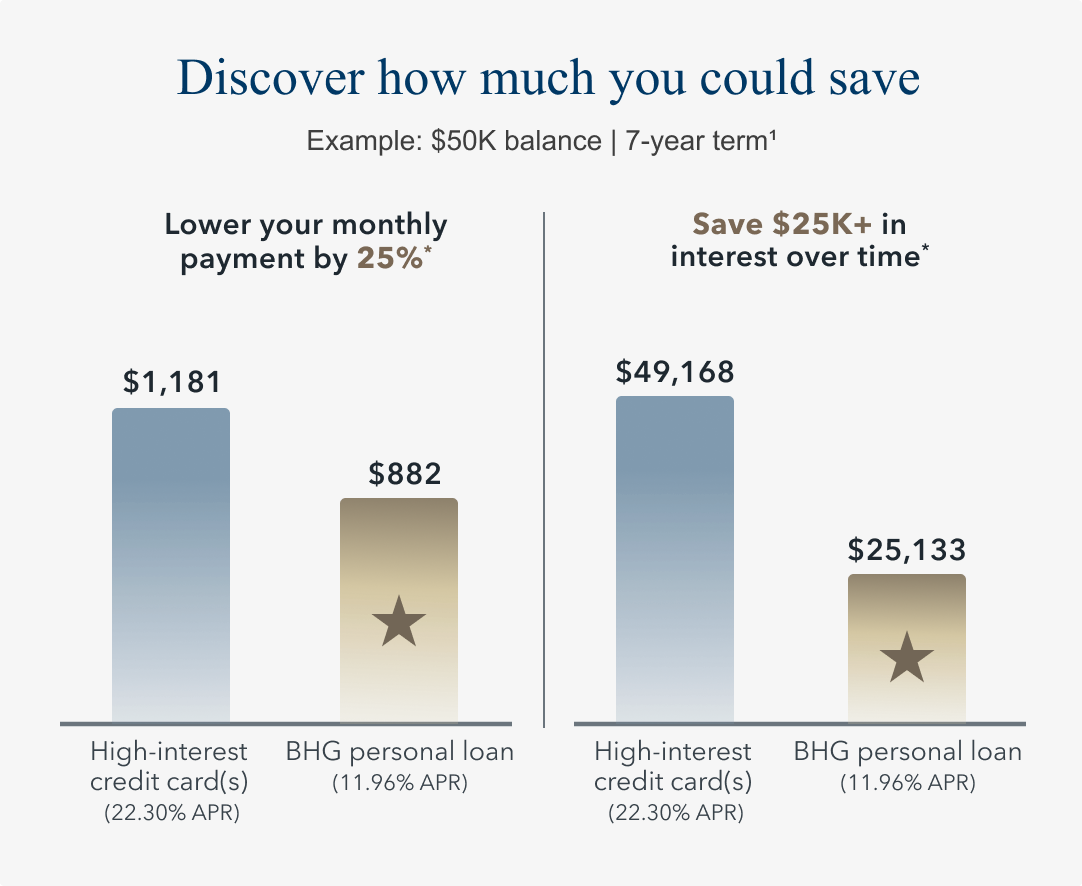

For example, if you’re carrying $50,000 across credit cards at 22% APR, monthly payments can exceed $1,181. Refinancing that balance into a fixed-rate personal debt consolidation loan at 12% interest would reduce the monthly payment to approximately $894.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $50,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,181 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $882 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

The debt still exists. But the structure improves cash flow immediately. Lower monthly payments can also create flexible capital to:

- Rebuild savings

- Increase retirement contributions

- Reduce reliance on revolving credit

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Debt that protects your long-term financial health

Another example of strategic debt is its use to preserve liquidity and maintain stability during major transitions, such as:

- Relocations

- Major home improvements

- Family milestones

- Passive income investments

Instead of liquidating investments at an unfavorable time, a structured loan can preserve assets, maintain investment momentum, and provide predictable repayment. Strategic borrowing, in this context, supports long-term stability rather than disrupting it.

The real question: Does this debt improve your financial position?

When evaluating new borrowing, move beyond emotion and run a simple cost-benefit analysis. Debt functions like an investment decision: you’re weighing cost today against measurable impact tomorrow—both financially and operationally.

The cost calculator

Before committing, evaluate your potential cost benefits, including:

- Monthly payment before and after

- Total interest paid over time

- Time required to offset any origination fees

If the new structure lowers both monthly obligations and overall cost, that’s a measurable improvement. If it stretches repayment far beyond your comfort zone with no cost advantage, reconsider whether additional borrowing aligns with your goals.

The efficiency factor

Even for strong earners, managing multiple accounts increases the risk of oversight. Divided attention can lead to missed payments, late fees, or unnecessary interest costs. Efficiency strengthens consistency—and consistency protects credit health and long-term borrowing power.

In the case of consolidation, multiple balances are replaced with a single fixed payment, one due date, and a clear payoff timeline. Fewer moving parts reduce friction and improve visibility into your financial progress.

The momentum metric

Scattered debt also slows financial momentum. When cash flow is fragmented across multiple balances, you have:

- Less room to build liquid savings

- Less room to invest consistently

- Less room to handle unexpected expenses without adding new credit

Consolidating or restructuring debt can restore forward motion. Clear timelines and predictable payments make it easier to measure progress toward future goals—and progress reinforces momentum.

When borrowing makes sense: Common strategic scenarios

Borrowing tends to make sense when it meaningfully improves cost, cash flow, or clarity. These examples illustrate how structured debt can strengthen—not strain—your financial position.

Consolidating high-interest debt to reduce financial drag

Replacing expensive revolving balances with lower, fixed-rate financing can reduce interest exposure and free up meaningful monthly cash flow.

Consider a small business owner carrying $75,000 in credit card balances. Despite making large monthly payments, most of the amount goes toward interest, with little reduction in principal. Frustrated by slow progress and unpredictable balances, they consolidate into a seven-year fixed-rate personal loan.

The new structure lowers interest costs and significantly reduces monthly obligations—freeing capital for retirement contributions while strengthening liquidity.

Simplifying payments to improve consistency and reduce missed-payment risk

Fewer moving parts reduce risk. A mid-career professional managing two credit cards and an existing personal loan finds the payments affordable—but the logistics overwhelming. Multiple due dates and fluctuating balances create unnecessary stress, and even one missed payment could impact a prime credit score.

By consolidating into a single structured payment with one due date and a defined term, they streamline oversight and reduce the risk of costly mistakes.

Using structured repayment to create a clearer timeline to becoming debt-free

Revolving debt can feel never-ending—even when you’re paying on time.

A borrower who has consistently met minimum payments for years sees little visible progress toward zero. By replacing revolving balances with a fixed-term loan, they gain a clear month-by-month path to payoff. Progress becomes visible. Visible progress changes behavior—and disciplined behavior compounds results.

When borrowing doesn’t make sense

Benefits aside, borrowing can be counterproductive when:

- There’s no defined plan. Taking on new debt without a clear purpose or repayment strategy increases risk.

- It’s used to maintain an unsustainable lifestyle. Debt should optimize structure—not subsidize spending beyond your means.

- Underlying habits remain unchanged. Consolidating without adjusting the behaviors that created the balances can restart the cycle.

Why debt consolidation can be a growth strategy (not just a rescue plan)

If high interest costs are absorbing a meaningful portion of your monthly income, that capital isn’t working toward growth. Redirecting those dollars toward investing, saving, or strategic opportunities can strengthen long-term positioning.

Consolidation can reduce financial drag and improve capital efficiency. If the new rate lowers your weighted average APR, you may decrease total interest exposure while improving monthly cash flow.

That shift isn’t just structural—it’s directional. It moves more of your income toward wealth-building instead of servicing high-cost debt.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Choosing the right consolidation loan: What to look for

Transparent terms and predictable monthly payments

Fixed rates, defined terms, and repayment options aligned with your budget create clarity. Longer terms can lower monthly payments and preserve liquidity—especially when flexibility matters more than rapid payoff.

Many lenders, including BHG Financial, offer prequalification through a soft credit inquiry3, allowing you to explore options and confirm that borrowing offers meaningful, measurable advantages before committing.

A process that respects your time

When you work with a lender that treats you like a partner, the process should reflect that. Streamlined applications, limited documentation requirements, and fast decision timelines reduce friction. Digital tools, clear communication, and responsive support help you move quickly when timing matters.

A lender that understands high-income borrower needs

Borrowing decisions often involve layered finances—variable income streams, business ownership, investment holdings, or multiple asset types. Effective underwriting should account for that complexity.

The right lender evaluates the broader financial context rather than relying solely on simplified metrics, helping ensure the solution aligns with your overall strategy.

A smarter way to simplify debt without derailing your financial goals

What a debt consolidation loan can help you do

A debt consolidation loan combines multiple debts into one fixed-rate personal loan with a structured repayment schedule. It can streamline your monthly obligations, potentially lower your total interest costs, and create a cleaner, more predictable budget.

Where BHG Financial fits in

BHG Financial offers debt consolidation loans designed for high-income borrowers who want structure, predictability, and flexibility.

With unsecured loan amounts up to $250,0001 and terms up to 10 years,1,2 qualified borrowers can access fixed-rate financing tailored to their needs.

Prequalification has no impact on your credit score,3 and approval decisions can be fast—often within 24 hours.4 This helps you access structured, predictable repayment that supports financial flexibility.

Final takeaway: The goal isn’t “no debt”—it’s better debt

Debt doesn’t determine your financial strength. Structure does.

When borrowing improves cash flow, reduces interest exposure, and clarifies your path forward, it can support growth rather than restrict it. Consolidation can transform scattered balances into a defined plan.

If your current debt structure is limiting your flexibility, a personal loan for debt consolidation may help you regain control and move forward with greater confidence. Explore how BHG can help you turn complexity into a clear strategy for what comes next.

Check my rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

4 This is not a guaranteed offer of credit and is subject to credit approval.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829