Personal Loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

Business loans

Tailored commercial financing that supports all your business needs to help you grow quickly.

Customized financing to consolidate high-interest debt or fund major purchases or expenses.

About BHG

Programs

Sign in

BHG Financial survey: Debt, credit, earning, & saving are all part of the Money Map journey

Table of Contents

- Income isn’t the end goal, it’s the fuel to get there

- Debt doesn’t have to derail people’s plans — it can help them move ahead

- Credit isn’t only a reflection of a person’s financial past — it paves the way for their financial future

- Wherever Americans are headed, saving is part of the route

- Making the American Dream personal

Achieving financial success rarely looks like a climb to the top, a race to the finish line, or a predetermined path to the American Dream. In 2026, a more realistic visualization of financial life in America is the BHG Financial Money Map, where there are many possible routes, resources, actions, and outcomes. Taking on debt, earning income, making purchases, building credit, and saving for the future are all money moves that can steer the course of a person’s financial path.

Most people feel hopeful about where they’re headed, no matter where they are on the BHG Financial Money Map right now. In fact, the 2026 BHG Financial Consumer Debt & Finances Survey shows that nearly three-quarters (74%) of respondents feel optimistic about their financial future. That number climbs slightly for higher-income Americans – 80% of high earners, which this report defines as those with annual household incomes of $100,000 or more, feel optimistic about their financial future.

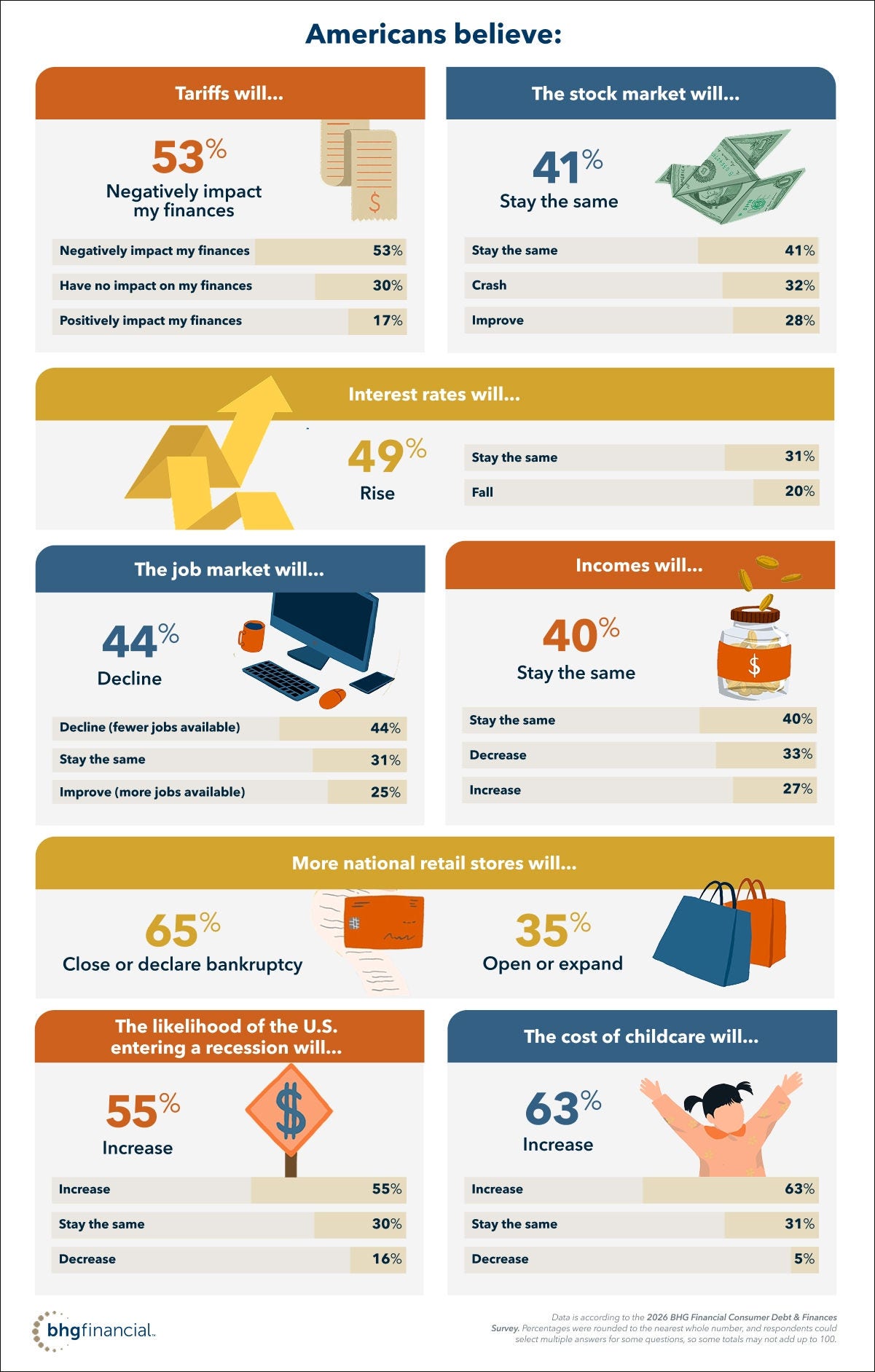

Americans are optimistic about their situations despite economic concerns. More than half (55%) of respondents said they think the likelihood of the U.S. entering a recession will increase, yet 64% of those still said they feel optimistic about their financial future. And more than half of respondents (57%) who said they have less than $5,000 across their bank accounts reported feeling optimistic about their financial future, even if they may not be well-prepared for unexpected expenses at the moment.

“The traditional narrative suggests financial success is a straight climb upward, but that’s not how people experience it,” Tyler Crawford, President of BHG Financial, said. “What we’re seeing in this data is a more realistic picture of Americans navigating a complex Money Map, making thoughtful decisions about saving, spending, and borrowing. That optimism reflects confidence that the actions they take today can meaningfully shape their financial future.”

"That optimism reflects confidence that the actions they take today can meaningfully shape their financial future."

Tyler Crawford

President of BHG Financial

Key Considerations

- Practically all (99%) respondents said saving money is somewhat or very important to them, and 49% have at least $20,000 across their checking and savings accounts.

- About half (48%) said they’re planning to make a big purchase related to travel (flights, hotels, activities, etc.) in the next year.

- 86% said they feel the American Dream is either somewhat or very attainable, and 44% said they believe the biggest challenge to achieving the American Dream is wages not keeping up with inflation and cost of living.

- 65% said the uncertainty of the U.S. economy is making it harder for them to make sound financial decisions.

- Almost half (45%) said they’re saving money for retirement, with only 31% of Gen Zers (ages 18-28 at time of survey) and 35% of millennials (ages 29-44 at time of survey) saying they’re doing so, compared to 53% of Gen Xers (ages 45-60 at time of survey) and 58% of Baby Boomers (ages 61-79 at time of survey). Just 7% of all respondents said they believe they’ll never be able to afford to retire.

- Nearly two in five people (38%) said they’re somewhat or very likely to miss a minimum debt payment in the next six months.

Income isn't the end goal, it's the fuel to get there

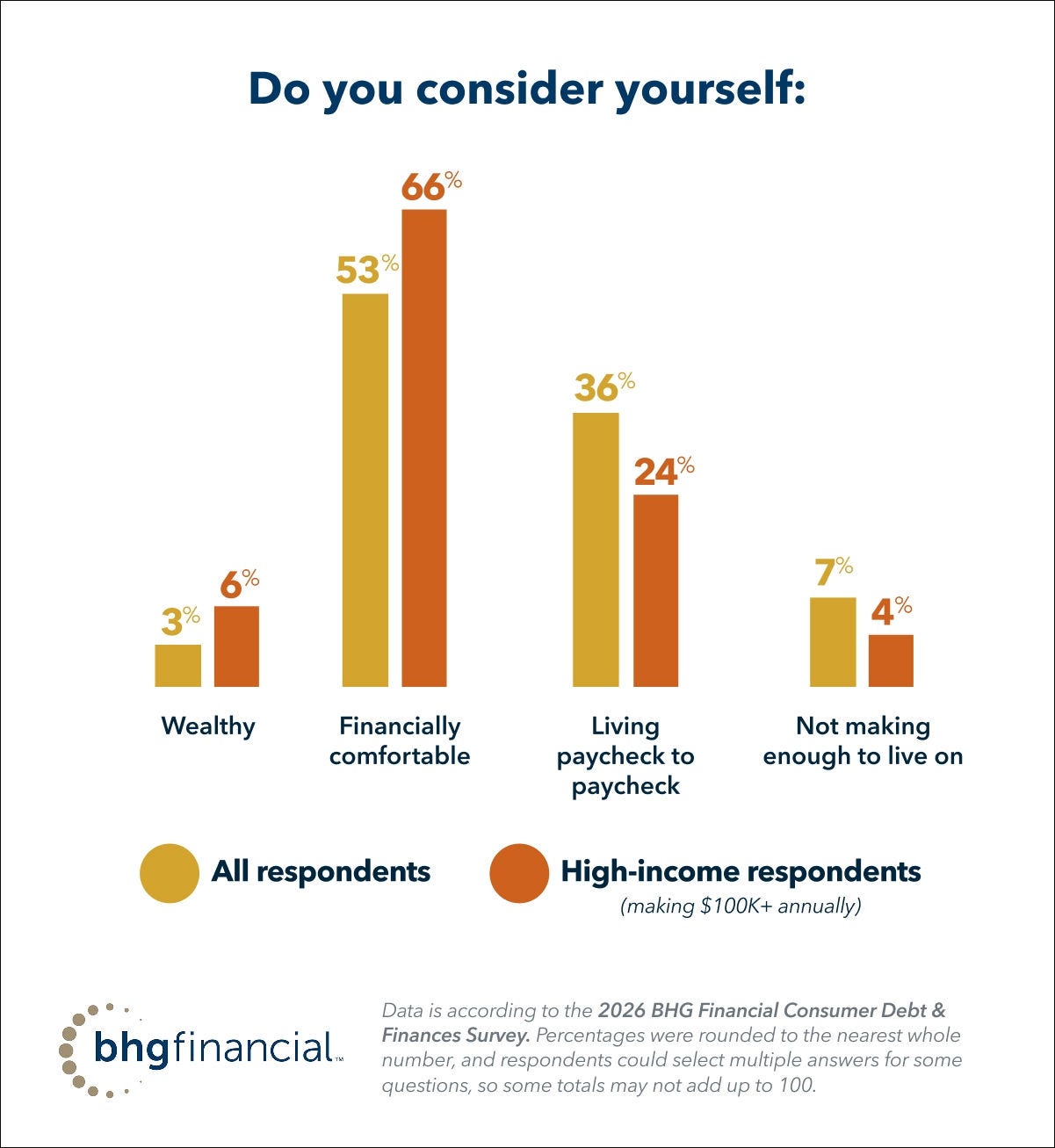

A high income is correlated with a greater degree of financial comfort. More than half (56%) of all respondents said they consider themselves financially comfortable or wealthy, with 72% who are making $100,000 or more annually saying the same.

Even so, financial security doesn’t suddenly appear when a person reaches a certain income threshold — it’s less about how much individuals earn and more about how they manage their money.

There are “...multi-millionaires who are more anxious about money than those who are kind of paycheck to paycheck,” says Dr. Dan Pallesen, CFP, CFT-I, PsyD, a financial advisor with a background in clinical psychology. “I think the biggest thing when it comes to financial security is ... someone who feels like they are participating in the outcomes of their life.”

In other words, being financially secure means making money moves. It’s all about being in the driver’s seat while traversing the BHG Financial Money Map and believing that “no matter what’s going to happen, I can create a plan, I can adapt,” he adds.

That mindset is something Americans can carry with them into unknown territory, such as a recession or unexpected job loss. More than half (55%) of respondents said the likelihood of the U.S. entering a recession will increase, while 30% said it will stay the same. Two in five think incomes will stay the same, while about one third (33%) expect incomes to decrease, and 44% think that the job market will decline (fewer jobs available).

Crawford says being proactive is key. “Take ownership of your financial situation and take action. Pay down your debt when you can, look for opportunities to consolidate, and be mindful of your choices so you build and maintain a good credit score. These seemingly small moves actually have a big impact on your overall financial situation and can give you ownership of that journey.”

Spending with purpose

Think of income as a resource that helps people make moves on the BHG Financial Money Map. Americans can use income to pay their bills, invest their earnings to grow their wealth, or spend a paycheck to advance their goals. The more intentional people are with their spending, the more advantageous their money moves will be.

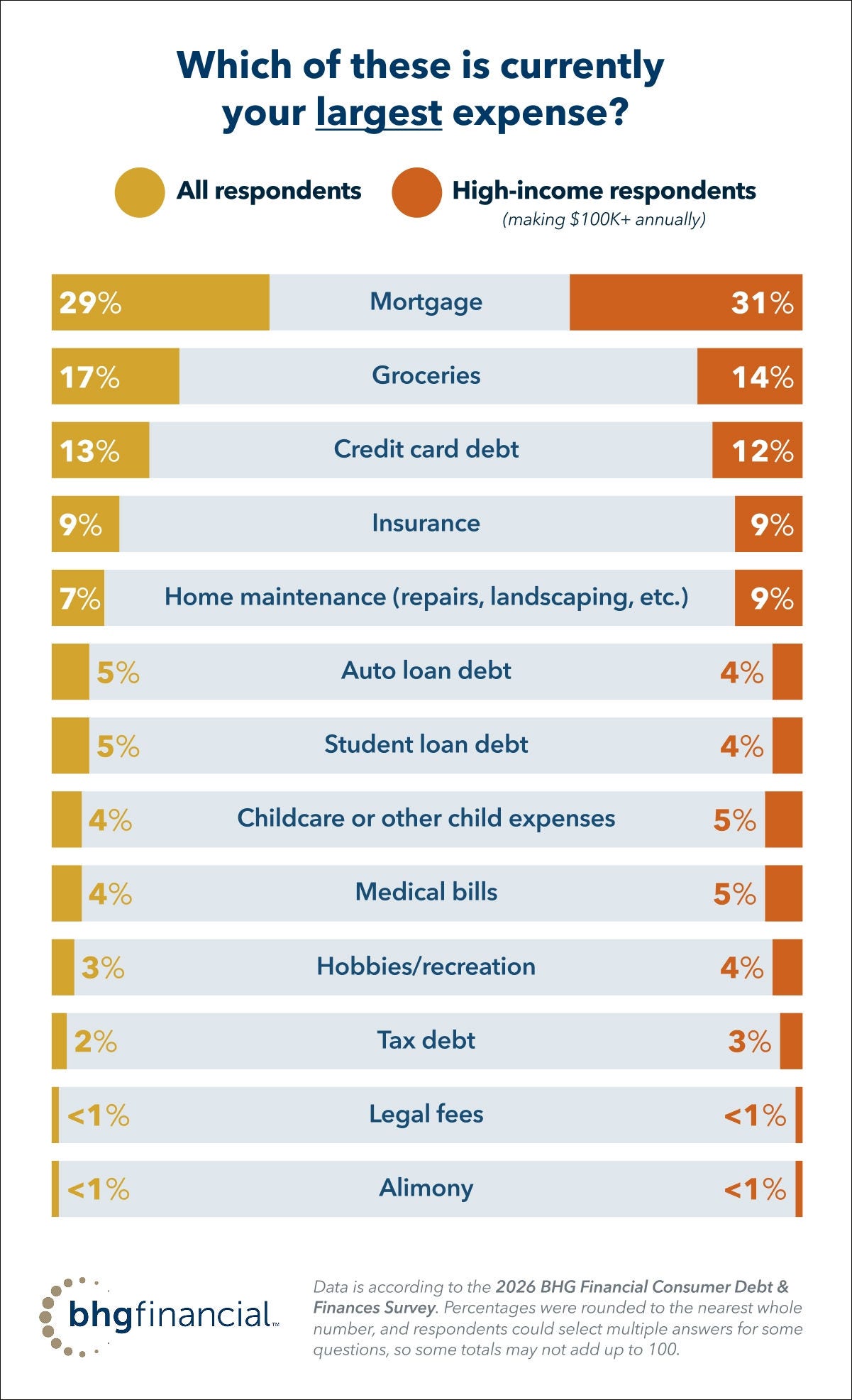

For example, buying a home creates an opportunity to build equity, allowing a person’s income to propel them further over time, even if their mortgage payment takes a chunk of their paycheck. Nearly one-third (29%) of respondents said their mortgage is currently their largest expense and 17% said groceries are currently their largest expense. These were the top responses for high-income households as well — 31% and 14%, respectively.

13% of all respondents (and 12% of high earners) said credit card debt is currently their largest expense.

“We’re in such a culture of consumption. And so, it drives a lot of the need to buy the newest and latest thing and finance it through credit card purchases, and it’s just so easy to get into debt without thinking about it,” says Dr. Pallesen.

Online shopping makes it especially easy to spend, with ecommerce sales rising. Meanwhile, 65% of survey respondents said they think more national retail stores will close or declare bankruptcy, which would ultimately change how and where consumers spend their money.

Credit cards have become essential to our daily lives, adding a component of convenience and ease of making money moves, but a culture of credit cards may also contribute to more impulsive discretionary spending. In fact, one in five respondents (20%) cited impulse purchases or overspending on non-essential items as a situation that contributed to their current debt.

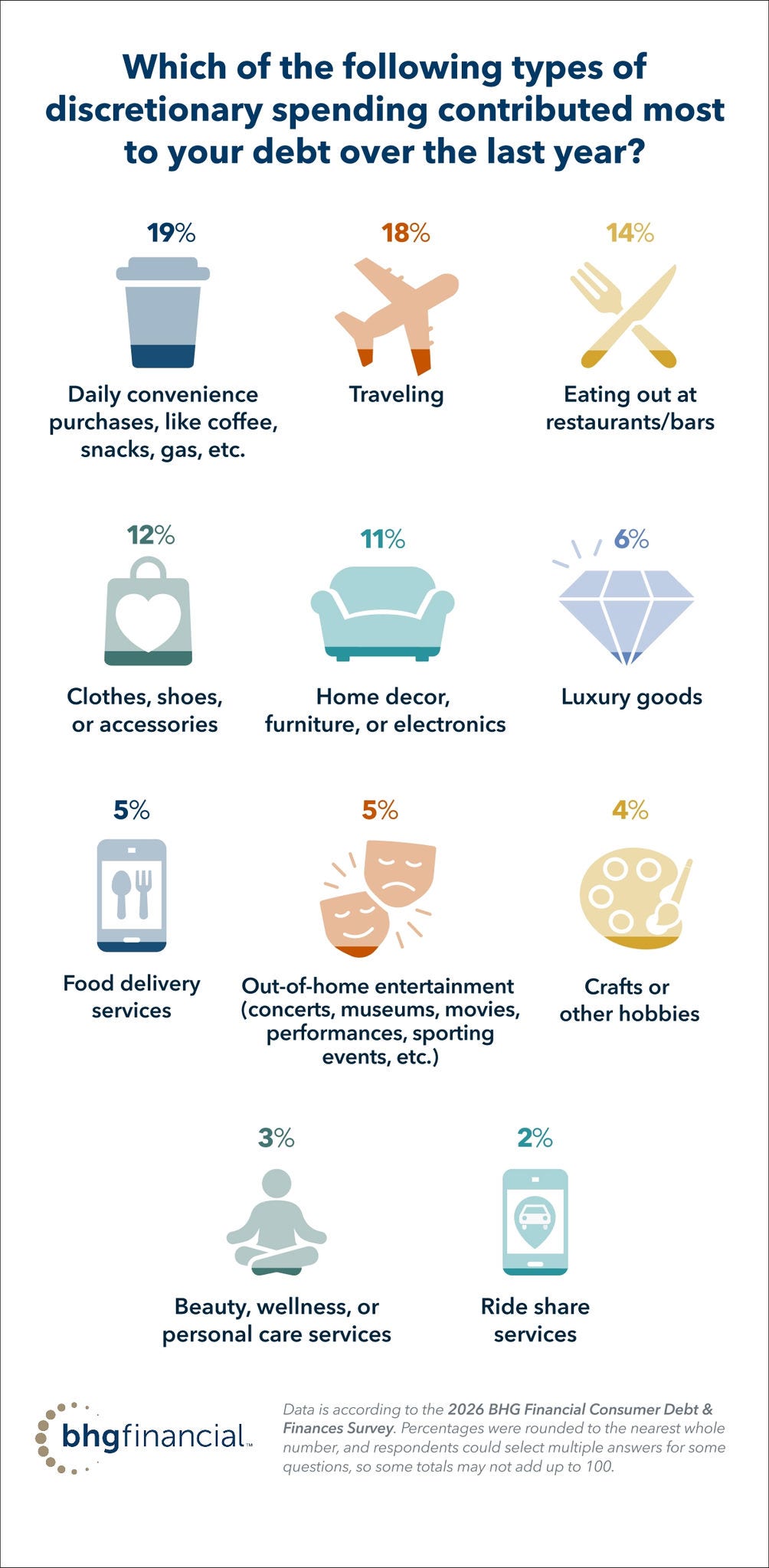

Nearly one fifth (19%) of respondents said the type of discretionary spending that contributed most to their debt over the last year is daily convenience purchases (like coffee, snacks, gas, etc.), the most common response. Other common responses included traveling (18%) and eating out at restaurants/bars (14%).

People with six-figure-plus household incomes were more likely to cite traveling (24%) as the type of discretionary spending that contributed most to their debt, followed by daily convenience purchases (16%), and eating out at restaurants/bars (11%). 10% said home décor, furniture, or electronics was the type of discretionary spending that contributed most.

Earning a bigger paycheck can often lead to an increase in discretionary spending, thanks to a phenomenon known as lifestyle inflation or lifestyle creep. “Psychologically, we get used to the things we’re exposed to,” explains Pallesen. “And so, at a certain income level, if that’s affording you purchases or experiences that were [out of reach before], you adapt to it. It becomes your new baseline, and so then you’re kind of seeking the next high.”

The social pressure of belonging to a wealthy peer group may also impact how some high-income earners spend their money. 13% of Americans earning $100K+ in annual household income said that relying on credit cards to maintain a certain lifestyle beyond their means contributed to their current debt.

That said, many Americans are planning ahead for major purchases. Nearly half (48%) of respondents plan to make a big travel purchase, such as booking a hotel, flights, or activities, in the next year, and nearly two in five (39%) are planning to pay for a home repair or improvement materials. More than a quarter (26%) said they plan to buy a new car in the next year.

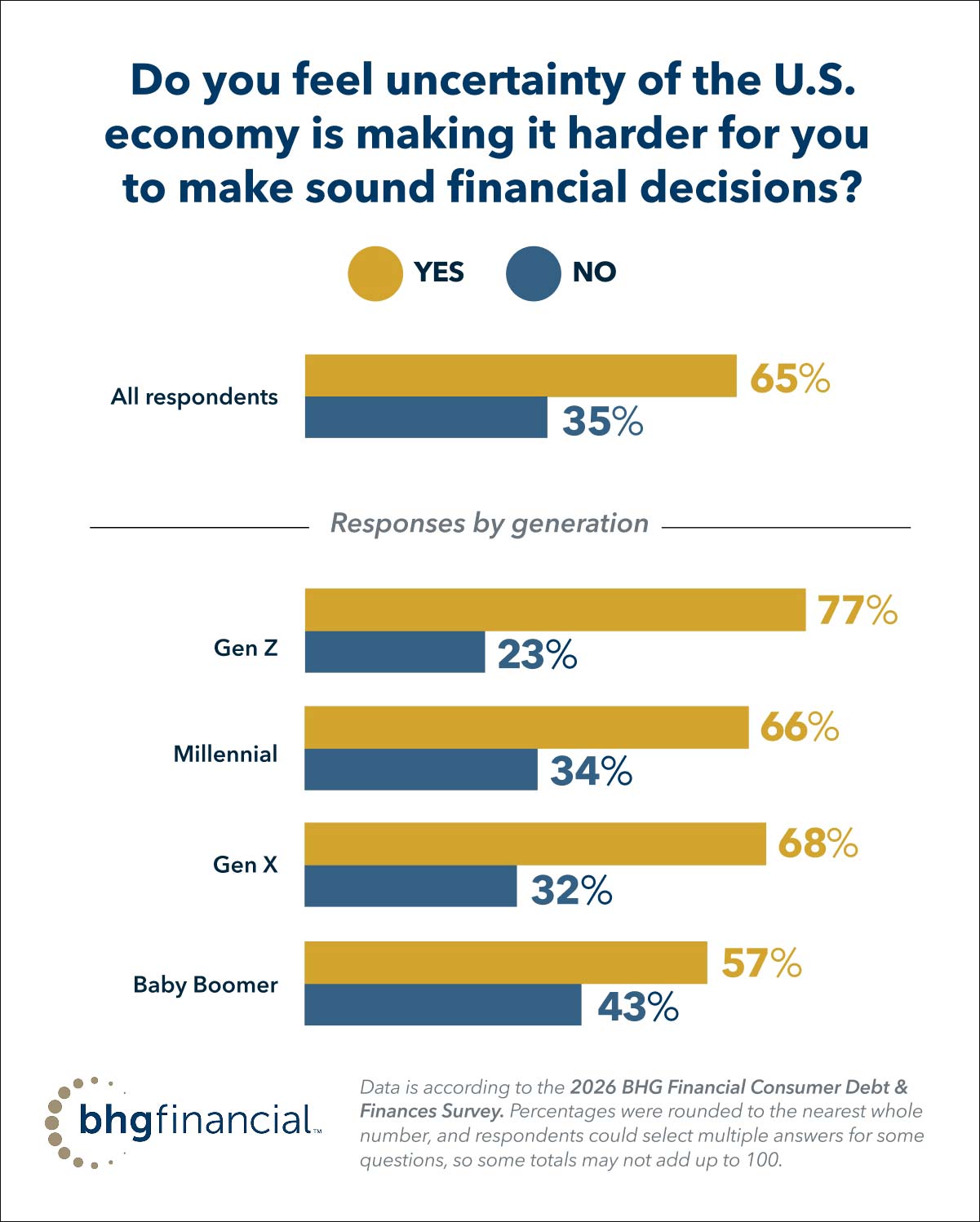

Finding financial security in an uncertain economy

65% of respondents said the uncertainty of the U.S. economy is making it harder for them to make sound financial decisions. The survey also shows that the effect of economic uncertainty on individual financial choices depends heavily on income and age.

- 62% of high-earners said the uncertainty of the U.S. economy is making it harder for them to make sound financial decisions.

- 77% of Gen Z, 66% of millennials, 68% of Gen X, and 57% of Baby Boomers said the uncertainty of the U.S. economy is making it harder for them to make sound financial decisions.

A second source of income may help with money moves, especially in uncertain times. Of those respondents with a second source of income from dividends, capital gains, or real estate income, 60% said economic uncertainty is making sound financial decisions harder, compared to 71% of people with only salary income.

A well-stocked emergency fund may also boost that feeling of financial security. Of respondents with at least $50,000 across their checking and savings accounts, 82% said they consider themselves financially comfortable or wealthy, and only 57% said the uncertainty of the U.S. economy is making it harder to make sound financial decisions.

Think of income and savings as resources that propel the journey around the Money Map, helping Americans safely navigate obstacles.

Debt doesn’t have to derail people’s plans — it can help them move ahead

Relying on debt can feel overwhelming, but debt can be a powerful tool to help achieve major life goals, like paying for higher education, buying or renovating a home, starting or expanding a business, or growing a family.

Debt can be as powerful as income at moving people forward, as long as they understand how they’re using it to get ahead, how they’ll repay it, and where they’ll land when this segment of their financial journey is complete.

According to Crawford, debt can be positive if it achieves more than it costs. That healthy debt can be things like “taking out a loan to make renovations to your home to improve your resale value or even getting additional education that may cost more now but will benefit you with higher salaries in the long run.”

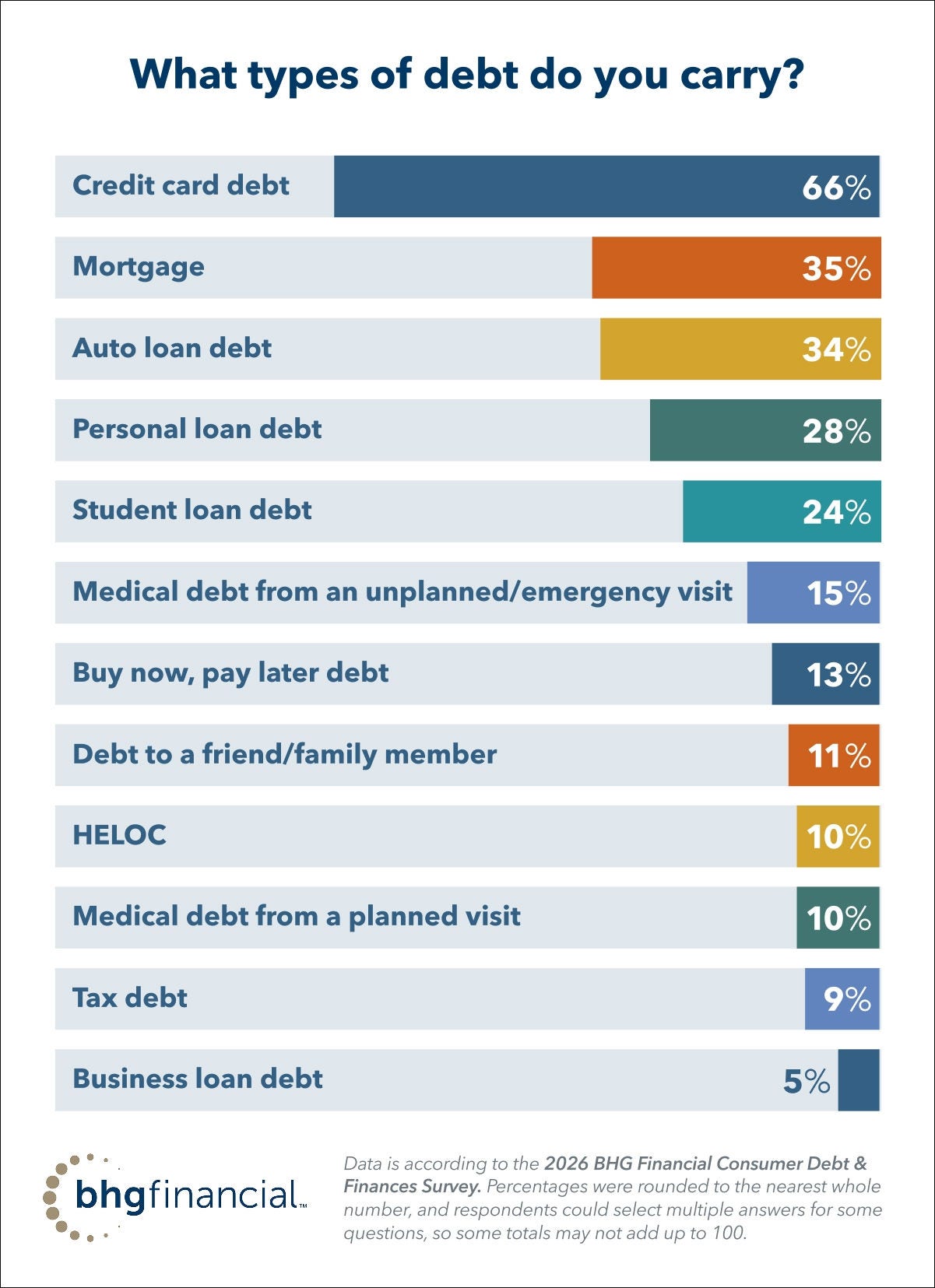

Many Americans have debt related to these goals. For example, 35% of respondents with debt have mortgage debt, 24% have student loan debt (including 41% of Gen Zers), and 5% have business loan debt. Some are also taking on credit card debt to achieve goals, including 12% of high-earners who said they used credit cards to finance a business venture or investment.

Crawford says he’s seen borrowers use debt strategically in recent years to upgrade their home instead of searching for a new one. “Home prices have increased across most of the U.S. in recent years, so many find it more affordable to upgrade their current home instead of buying a newer home. In those instances, you can finance your renovations for a fraction of what you’d pay if you moved, ultimately putting you in a better financial situation long-term.”

Yet cultural attitudes toward debt are often negative, which isn’t always a fair perception. “The stigma of debt, I think, is mostly negative,” says Dr. Pallesen. “It creates a lot of fear, anxiety, and hopelessness.”

Nearly half (46%) of respondents with debt said their current financial situation negatively impacts their mental health. And when asked which financial milestone is the most important, 38% said being debt free, which is an attainable goal.

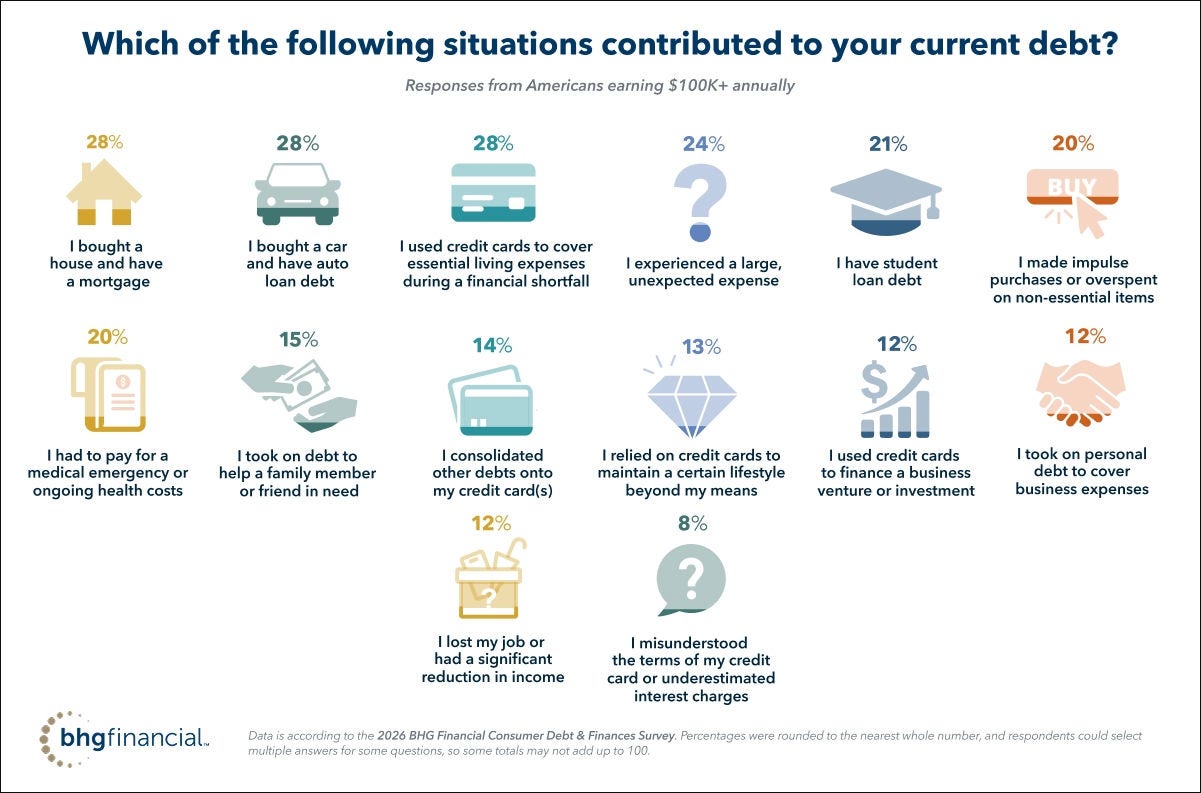

Often, debt happens due to a combination of circumstances. For example, one in five respondents said that making impulse purchases or overspending on non-essential items was one situation that contributed to their current debt. Of those, 24% also said that a large, unexpected expense contributed to their debt, 21% said a medical emergency or ongoing health costs contributed to their debt, and 16% said a job loss or income reduction contributed to their debt.

"When this happens, small wins can go a long way. Create a plan and take it day by day, month by month. This can help you feel like you're taking back control."

Tyler Crawford

President of BHG Financial

The most cited situation that contributed to respondents' debt was using credit cards to cover essential living expenses during a financial shortfall (31%). This strategy can help bridge the gap between income and expenses, which keeps Americans in the game. But once financial recovery is possible, the next money move can be a smart debt payoff plan.

Choosing a savvy debt repayment plan

When it comes to fine-tuning your financial strategy, the amount of debt a person carries is less important than how they manage repayment. Crawford says that if a person “can get to a point where they’re not increasing their debt over time and they’re managing their cash flow via the income they earn, I think that’s the most prudent position they could be in.”

Having a plan for debt repayment can help anyone make major strides around the Money Map, allowing them to maintain financial stability and avoid backsliding.

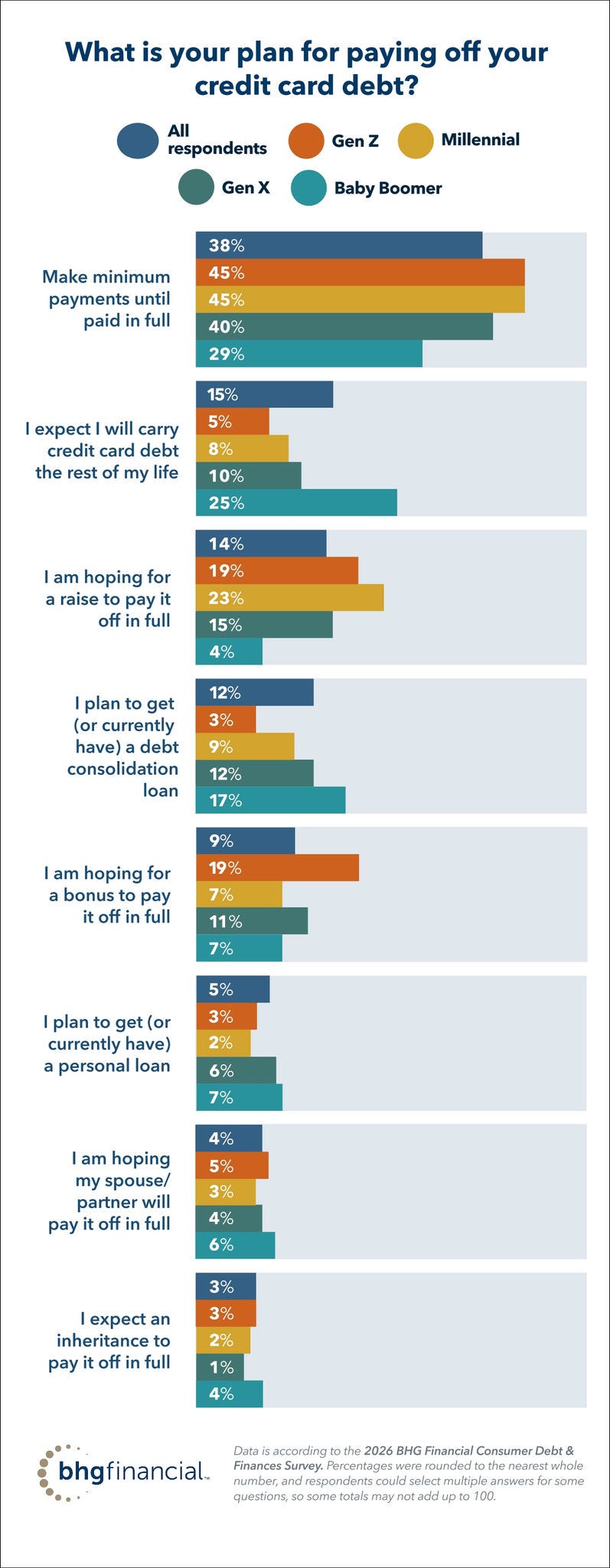

The most commonly reported plan for paying off credit card debt was to make minimum payments until the debt is paid in full (38% of all respondents with debt). This was also the case across generations and income levels, including:

- 38% of respondents with more than $100,000 in household income

- 45% of Gen Zers

- 45% of millennials

- 29% of Boomers

When asked how they planned to pay off their credit card debt, 15% of respondents said they expect they will carry credit card debt for the rest of their lives. That number is even higher (25%) for Baby Boomers.

But that’s certainly not the case for everyone, as many respondents cited plans to pay off their credit card debt – 14% are hoping for a raise to pay it off in full, and 12% said they plan to get (or currently have) a debt consolidation loan. People who planned to, or currently do, use debt consolidation loans or personal loans were more likely to feel confident they could keep up with their minimum payment. Not quite a third (30%) of those said they felt they were somewhat or very likely to miss a debt payment in the next six months, as opposed to 38% of all respondents.

Debt consolidation may help people access routes on the BHG Financial Money Map that would be tough to navigate without a personal loan as a payoff tool. “A debt consolidation loan could put you in a much better spot financially. It simplifies your debt, ultimately creating new paths for you now and in the future,” says Crawford.

Credit isn’t only a reflection of a person’s financial past — it paves the way for their financial future

Credit scores are often seen as a measure of financial responsibility. People with good or excellent credit have achieved an important money milestone — in fact, more single people are disclosing their credit scores on dating apps as a signifier of financial success. And while they are important, credit scores are a snapshot of a person’s finances, not the endpoint of their financial journey. And every money move has the potential to open new opportunities via credit score improvements.

The vast majority of respondents (78%) said they have good credit (a FICO score of 670 or above), and a quarter (25%) said they have excellent credit (800+ FICO score). For people with annual household incomes above $100,000, those shares jump to 86% and 30%, respectively.

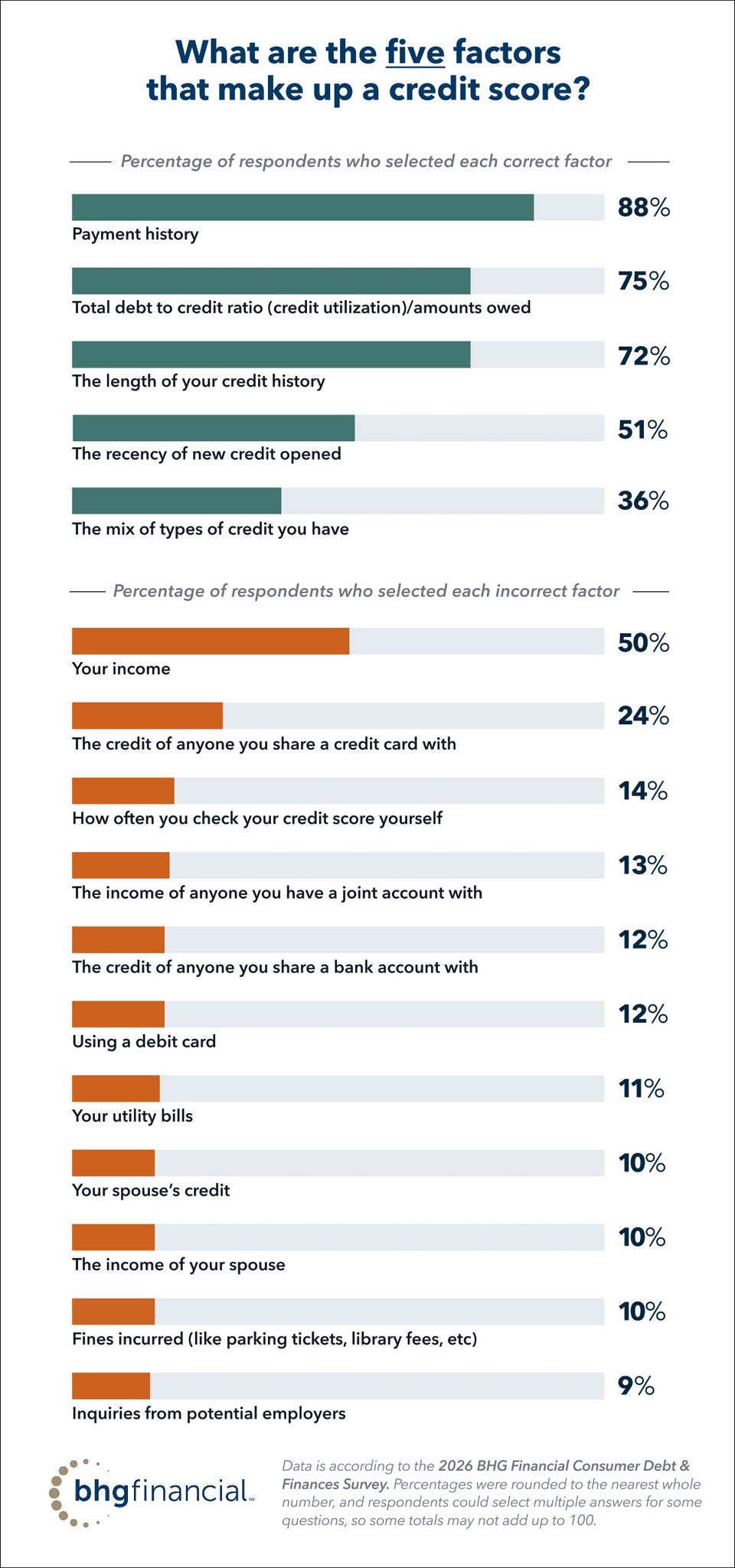

But to make those positive credit moves, it’s important to understand how a credit score is calculated. Half of respondents incorrectly identified income as one of the five factors that make up a credit score, and nearly a quarter (24%) incorrectly believed that the credit score of anyone they share a credit card with is a factor in their own score.

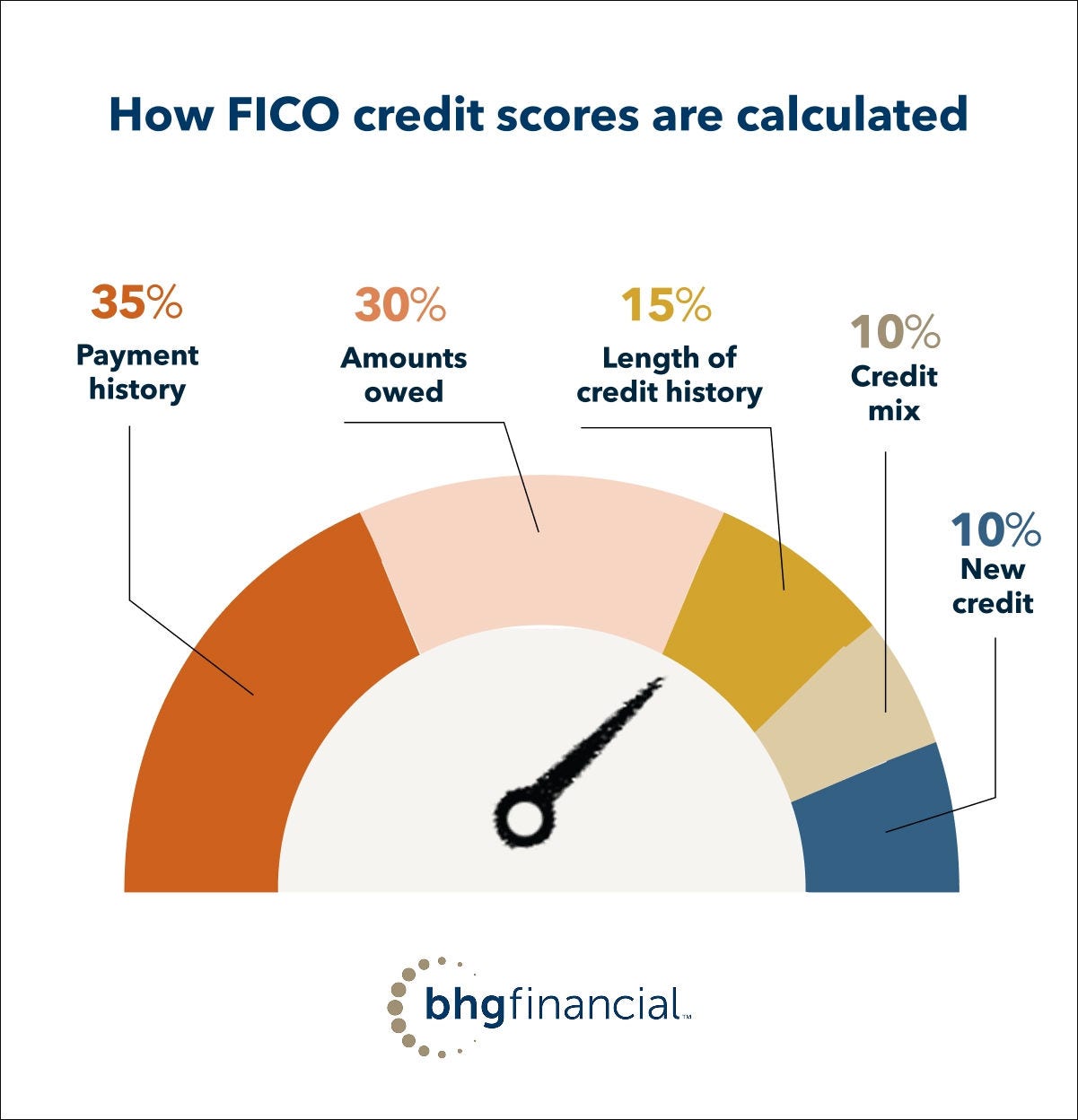

The elements of a credit score

There are five factors that make up a FICO score and each category impacts the score at different percentages.

88% of respondents correctly identified payment history as being one of the factors that make up a credit score. And three quarters of (75%) correctly identified total debt to total credit ratio (credit utilization)/amounts owed as one of the five factors that make up a credit score.

Just as paying down debt can improve credit utilization, opening a new credit card can ultimately raise a person’s credit limit and improve their credit score, assuming they use the card wisely. Of the 30% of respondents who said they plan to open a new credit card in the next year, 32% said their main reason for doing so was to build or improve their credit score, the most common response.

Improving or maintaining a good credit score can help a person with positive money moves on the BHG Financial Money Map — they might use rewards points to save money on travel or take advantage of their strong credit to secure better rates on loans.

Most respondents (72%) correctly identified the length of their credit history as one of the five factors that make up a credit score. Credit scores tend to improve as the average age of a borrower’s credit accounts increases, so it’s no surprise that 47% of Boomers said they have excellent credit, compared to 9% of Gen Zers.

Of the 70% of respondents who said they don’t anticipate opening a new credit card in the next year, nearly half (49%) said it’s because they have enough credit cards, and 22% said they’re focused on paying down their existing balances and other debts. That’s a strong money move that can improve a person’s credit as well, even if it happens gradually.

Wherever Americans are headed, saving is part of the route

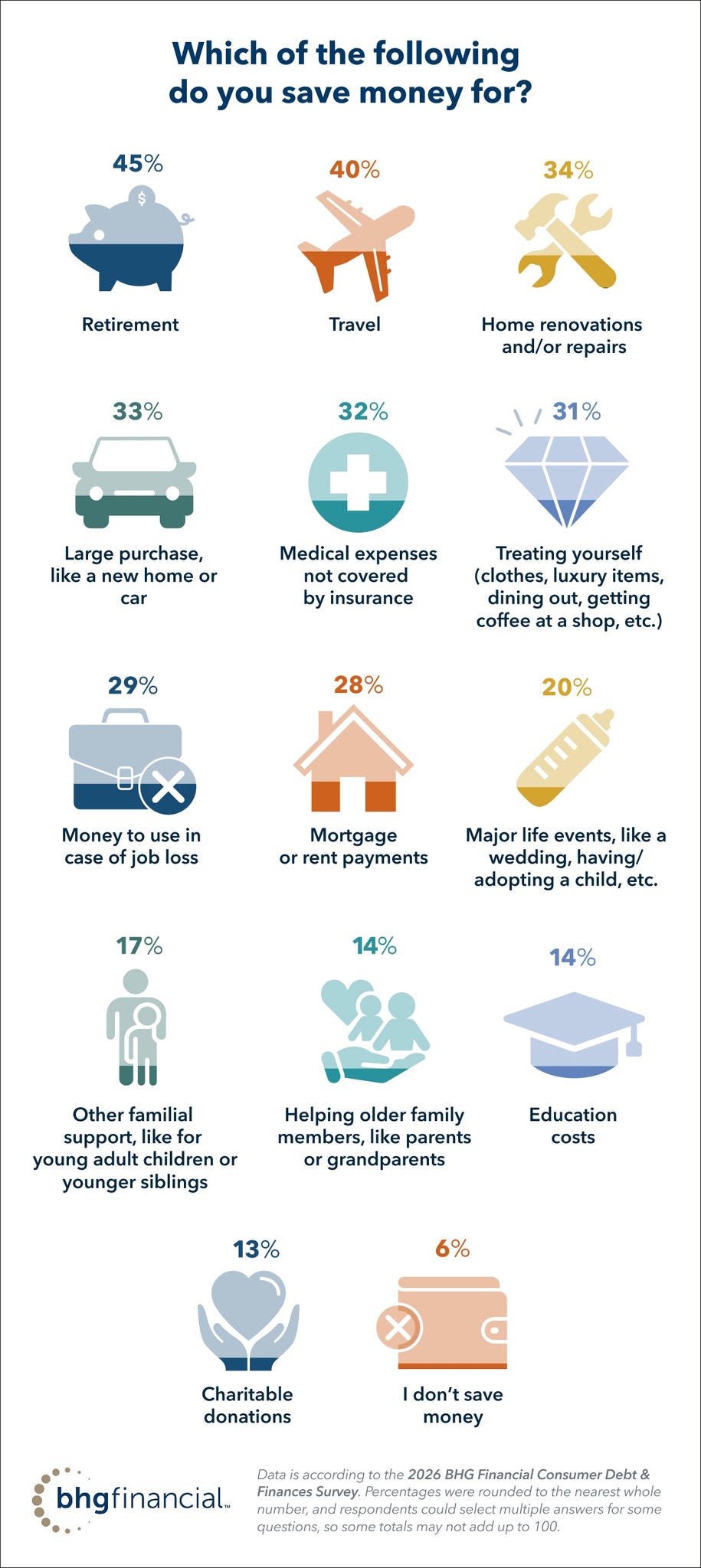

99% of respondents said saving money is at least somewhat important to them, with 75% saying that saving money is very important to them. That number increases to 79% for high-earners. The thing most respondents said they’re saving for is retirement (45%), followed by travel (40%), and home renovations and/or repairs (34%).

Most feel they have enough savings

Sometimes, a mini money move can have a major impact. For example, setting up a regular automatic deposit into a high-yield savings account, even if it’s a small amount, can help set someone up for financial security in the future.

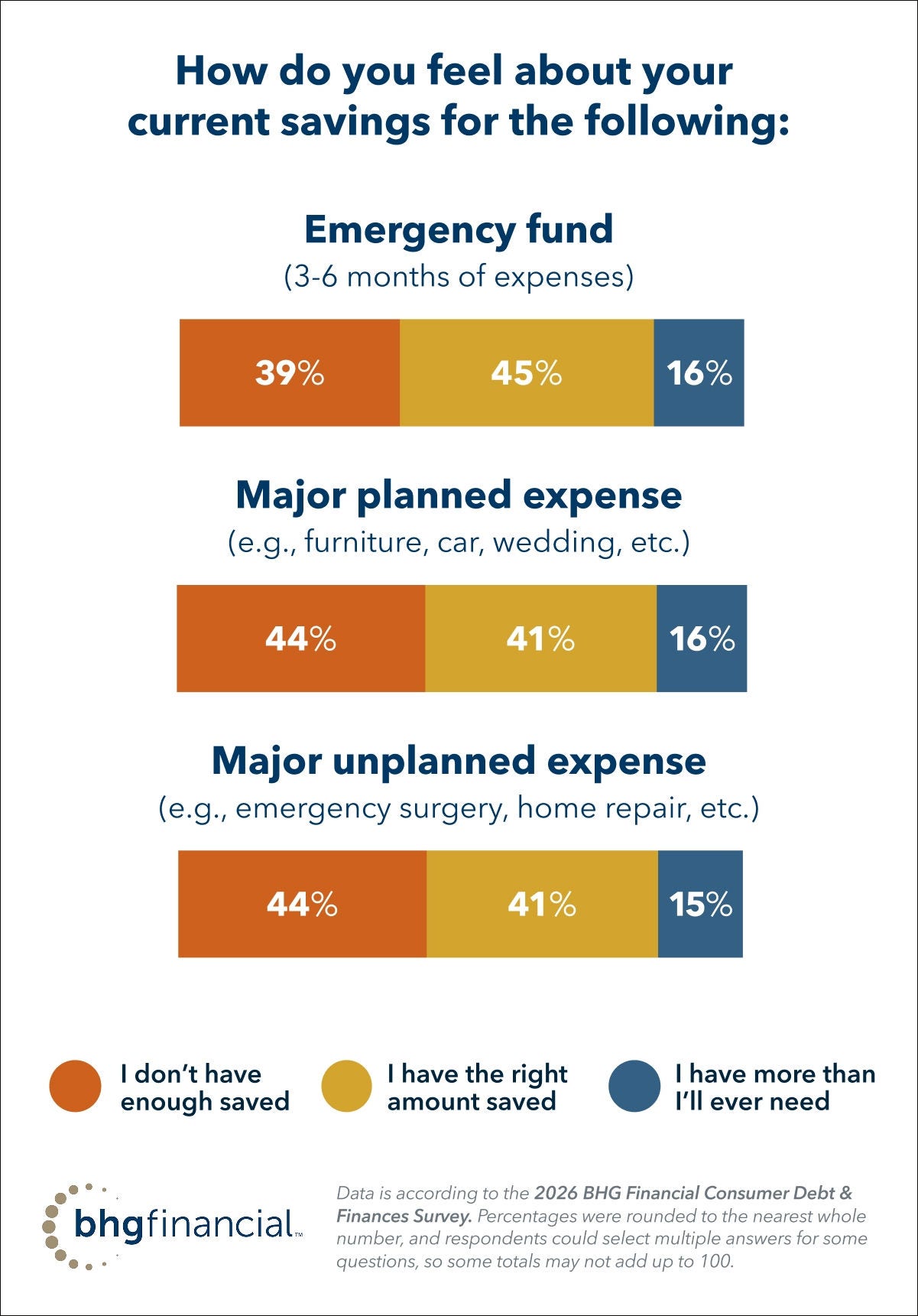

Many respondents believe they’re on track with their savings, with 61% saying they feel they have the right amount or more than they’ll ever need saved for an emergency fund (three to six months of expenses). That share rose to 73% for six-figure-plus households.

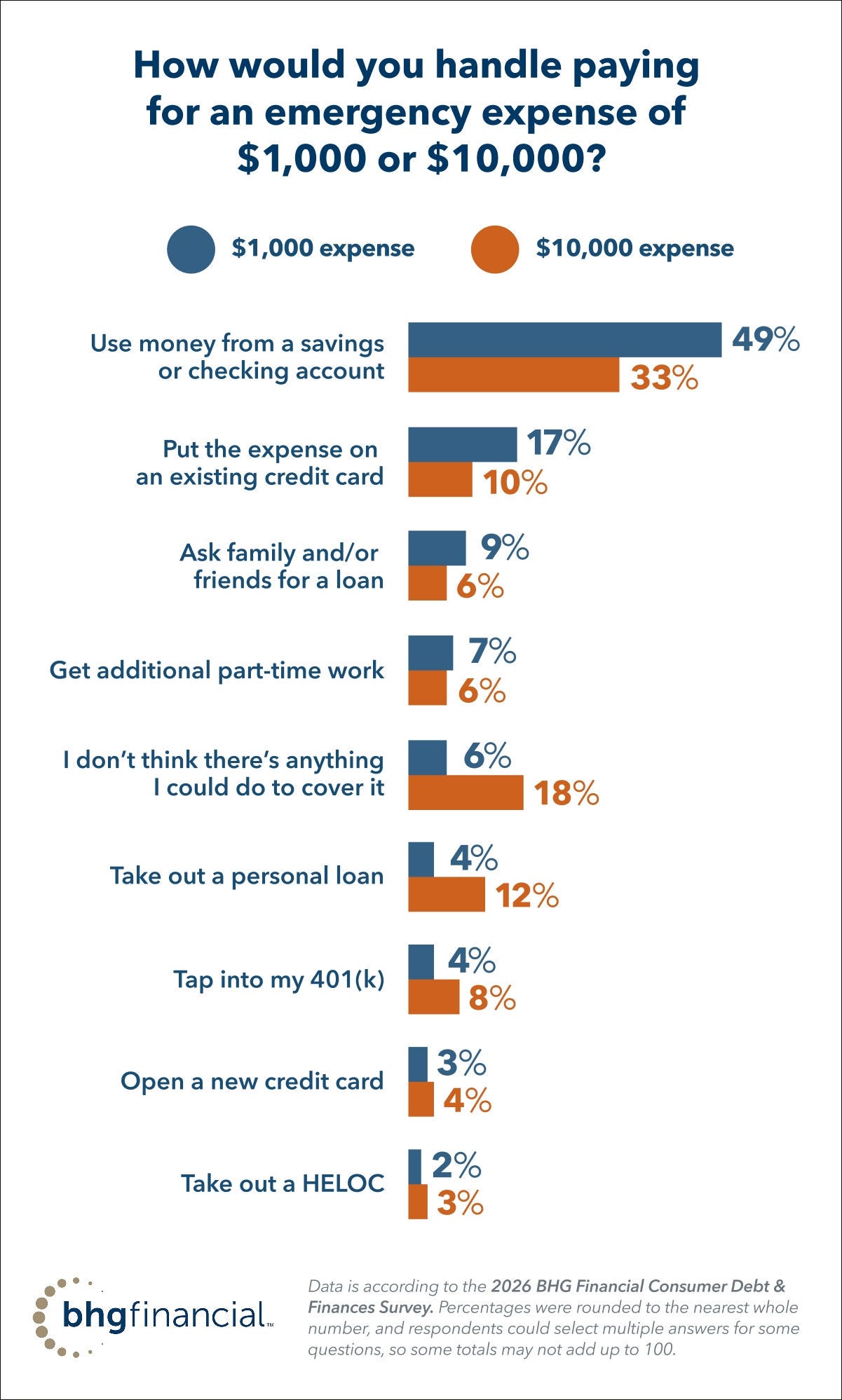

Nearly half of respondents (49%) said they could cover a $1,000 emergency expense from their checking or savings account, and 33% said the same about a $10,000 emergency expense. Just shy of half (49%) have at least $20,000 across their checking and savings accounts.

The biggest barrier to saving is the human brain

When it comes to spending behaviors that impact our ability to save, our brains can work against us. “The brain is designed for the immediate gratification and not the delay of reward,” explains Dr. Pallesen. This can impact our financial decisions for future experiences, like retirement and emergency funds.

Two in five respondents (40%) said they have less than $10,000 across their checking and savings accounts. Of those with less than $10K in the bank, more than a quarter (27%) said they feel they have the right amount saved or more than they’ll ever need in an emergency fund (three to six months of expenses), and a quarter (25%) said they feel they have the right amount saved or more than they’ll ever need for a major unplanned expense.

Of those with six-figure-plus household incomes, 26% said they have less than $10,000 across their bank accounts. The share was only slightly less (23%) for respondents earning at least $200,000 in annual household income.

Getting a large paycheck can also create a sense of financial security, with or without a stocked emergency fund. Of high earners who said they have less than $10,000 across their bank account balances, a third (33%) said they consider themselves financially comfortable. A smaller share (14%) even said they could cover a $10,000 emergency expense with their checking or savings account balances, despite indicating insufficient funds when asked about their bank account balances.

Crawford says liquid cash is just one metric people consider when they think about their financial security. “Financial security goes beyond your paycheck, although that is important, especially in your day-to-day,” he says. “It also comes down to what makes you feel secure individually. For some, it’s about setting themselves up for retirement by maximizing their 401(k) or investment accounts. For others, it’s about looking more toward real property. It’s all about what makes someone feel secure, which tends to vary widely and speaks to why our survey shows some people feeling financially secure without a lot of money in the bank.”

"It's all about what makes someone feel secure, which tends to vary widely and speaks to why our survey shows some people feeling financially secure without a lot of money in the bank."

Tyler Crawford

President of BHG Financial

Building for the future

Nearly 1 in 5 (19%) of respondents said they think building a retirement fund is the most important financial milestone to achieve. That same amount (19%) said their biggest financial regret is waiting too long to save for retirement, the most common response.

As mentioned earlier, 45% of all respondents said they’re saving for retirement. That tapers by generations: Baby Boomers (58%), followed by Gen Xers (53%), millennials (35%), and then Gen Zers (31%).

Overall, just more than a quarter (26%) of respondents said they plan for Social Security benefits to be their primary source of income in retirement, the highest response. However, generations are thinking about their primary income sources for retirement differently, especially when it comes to personal savings.

- Gen Zers: 35% said they plan for personal savings to be their primary source of income in retirement, followed by 401(k) distributions (27%)

- Millennials: 32% plan for their 401(k) distributions to be their primary source of income and 29% said it would be personal savings

- Gen Xers: 28% said 401(k) distributions would be their primary income source, while 23% said it would be Social Security benefits, and 15% said it would be personal savings

- Baby Boomers: More than half (51%) said they planned to primarily rely on Social Security benefits for income in retirement, 19% said they planned to use pension benefits, 12% plan on 401(k) distributions, followed by only 8% planning on personal savings being the primary source of income in retirement

Only 7% of all respondents said they believe they’ll never be able to afford to retire.

Making the American Dream personal

The American Dream has evolved over the years, but most are confident it’s within reach. The vast majority (86%) of respondents said they feel the American Dream is either somewhat or very attainable, with 91% of $100K+ earners saying the same.

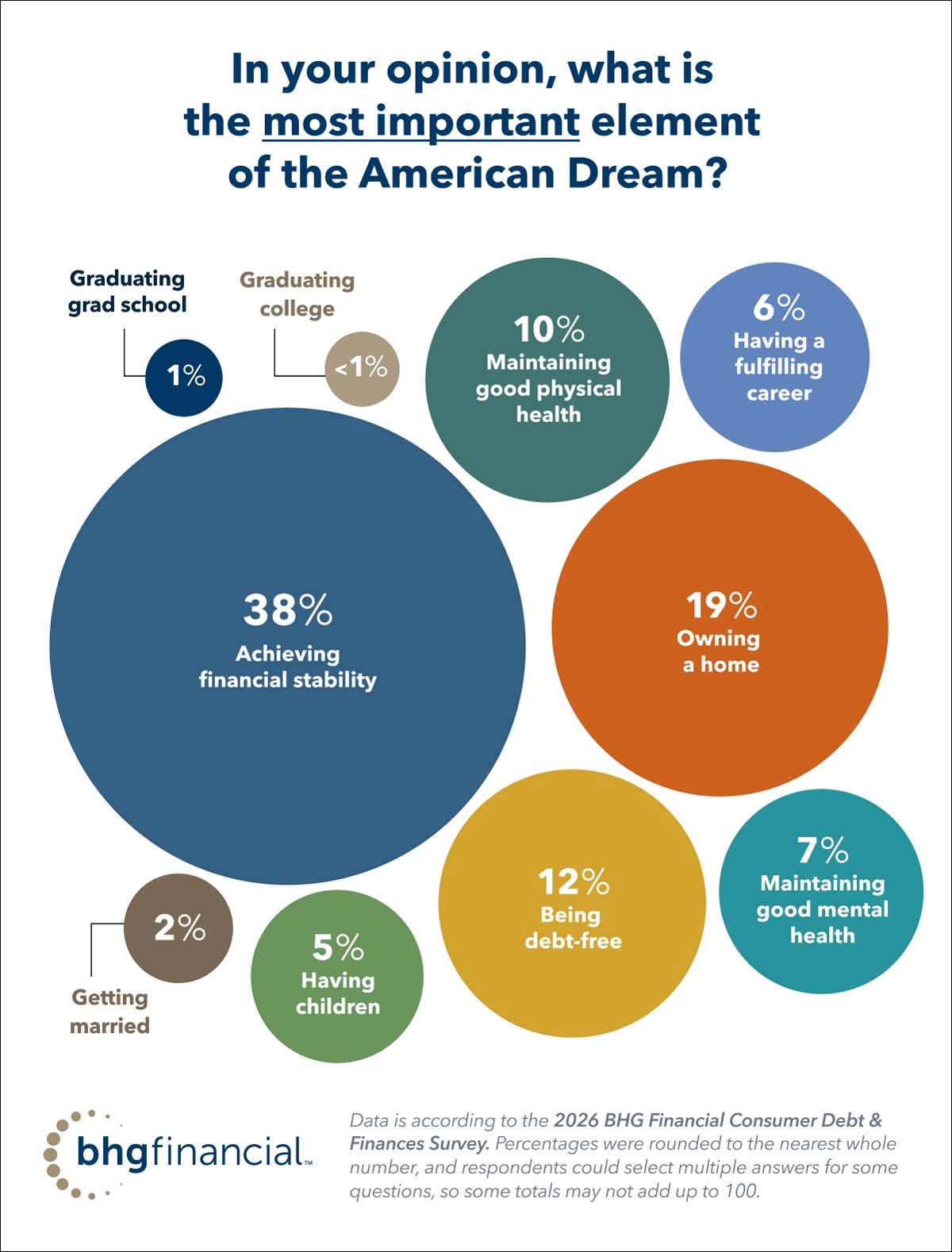

When asked about the most important element of the American Dream, the highest response for all respondents was achieving financial stability (38%). Only 19% said owning a home is the most important element of the American Dream.

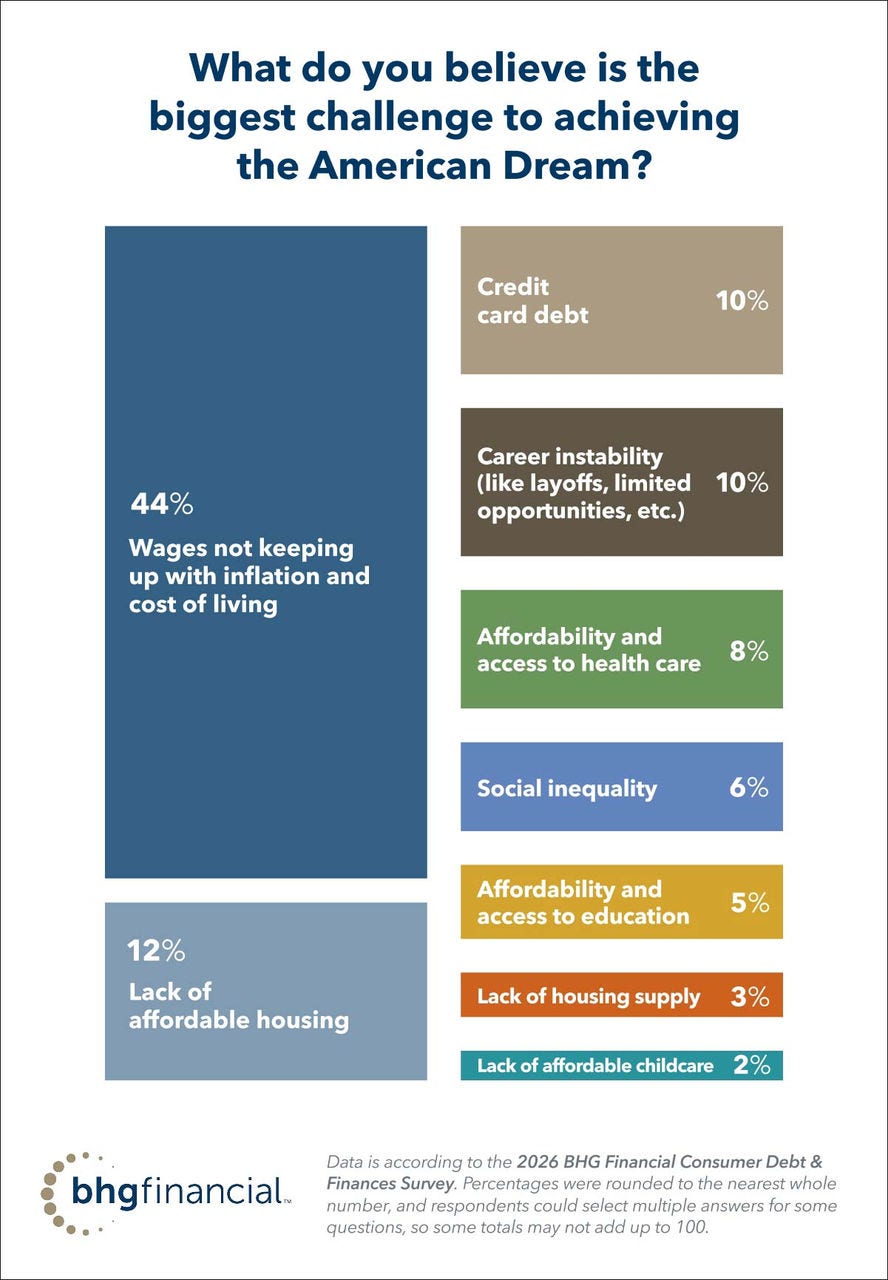

More than two in five (44%) respondents said the biggest challenge to achieving the American Dream is wages not keeping up with inflation and cost of living, while 12% said it's a lack of affordable housing. Among high-income earners, 38% said the biggest challenge to achieving the American Dream is wages not keeping up with inflation and cost of living, while 13% cited credit card debt.

As the 2026 BHG Financial Consumer Debt & Finances Survey reveals, income isn’t the only ingredient in financial well-being.

Ultimately, financial success in today’s America isn’t going to look the same as it did in the past. So, what does achieving financial stability mean today? It’s no longer an ideal held in the national consciousness, like the image of a house with a white picket fence. That’s because there isn’t just one way to be financially successful in America. On the Money Map, there are dozens of routes that lead to your version of the American Dream. When an obstacle arises, Americans can make money moves to get to their destinations.

“We’ve seen a lot of different situations and heard several financial journeys, which is what got us thinking about the Money Map. Everyone’s journeys are different and there’s no straight path to financial success. But what’s interesting is we can all see ourselves on the Money Map, no matter what’s happening in your life, whether you are looking to consolidate debt, you took on new debt to buy a home, you got a bonus at work, or you’re undergoing a home renovation. The path is individual, but we’re all on the Money Map together.”

"The path is individual, but we're all on the Money Map together."

Tyler Crawford

President of BHG Financial

Methodology

BHG Financial commissioned Qualtrics to survey a nationally representative sample of 2,012 working adults aged 18 and older making an annual salary of $50,000 or more. The survey was carried out online between May 27 to June 17, 2025. Figures have been weighted and are representative of all U.S. adults aged 18+. The average margin of error for responses is +/-2%. Percentages were rounded to the nearest whole number, and respondents could select multiple answers for some questions, so some totals may not add up to 100.

For California Residents: BHG Financial loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829