Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Are Personal Loans a Good Idea for High Earners? What the Data Says

Personal loans aren’t just a fallback option—they’re increasingly used by high-income borrowers as a practical way to manage cash flow and fund major expenses.

Data suggests that higher earners face many of the same financial strains as everyone else, from rising living costs to competing priorities for their cash. As a result, many are turning to personal loans not because they’re struggling, but because they’re optimizing—using fixed-rate financing to stay flexible, preserve liquidity, and move forward with confidence on bigger financial goals.

High earners aren’t immune to cash flow strains

Despite higher salaries, many six-figure households live with surprisingly thin financial cushions. BHG Financial’s 2026 Consumer Debt & Finances Survey reveals that only 27% of families earning $100,000 or more feel confident they could cover three months to six months of expenses with savings in an emergency, and 26% of six-figure-plus households have less than $10,000 across their bank accounts. That means the majority are vulnerable if income slows or costs spike.

The Consumer Financial Protection Bureau’s Economic Well-Being report echoes this reality: 12.1% of households with incomes above $125,000 struggled to pay bills in the last year. Rising costs for housing, childcare, and healthcare often offset higher wages, leaving even well-compensated families feeling squeezed.

This helps explain why personal loans are gaining traction in the higher-income segment. According to a recent study, high earners account for more than one-third of personal loan demand.

As of Q2 2025, the number of loans funded climbed to 5.4 million, up 18% year-over-year, marking the strongest growth on record, according to a TransUnion Consumer Lending report. Prime borrowers—those with credit scores above 721—are the main drivers of growth, representing 20.2% of all originations.

Personal loan use and impact among prime borrowers

Here’s how prime borrowers—with a healthy credit history, strong incomes, and sound financial habits—are using personal loans, according to the latest data:

Borrowing power and loan size

High earners with excellent credit are more likely to qualify for larger loans than the average borrower. TransUnion data revealed that borrowers with scores above 721 have an average loan balance of $16,300 to $17,500 per consumer. This is over one-third higher than the average loan balance for all credit tiers: $11,700.

While the average loan duration lasts about 30 months, prime borrowers often extend their terms to 49 to 58 months, which helps them keep monthly payments low, even with a larger loan.

Debt levels and rates

TransUnion data also shows that borrowers with good and excellent credit are fueling most of the growth in personal loan originations and balances—signaling a shift in how higher-income households are managing debt. Instead of relying more heavily on revolving credit, many are turning to fixed-rate installment loans to gain predictability and control interest costs.

But what stands out is the potential cost advantage: prime borrowers typically secure APRs of 13% or lower, a significantly more favorable rate than the median APR of 21%, which applies to all borrowers. For high earners financing large balances, that difference can translate into thousands in savings over the life of a loan.

Credit strength (and a knowledge gap)

BHG Financial’s survey suggests many Americans already have strong credit: 78% reported good credit (FICO 670+), and 25% reported excellent credit (800+). Among households earning $100,000+, those shares rise to 86% good credit and 30% excellent credit.

At the same time, the survey shows some common misunderstandings that can affect borrowing decisions. Half of respondents incorrectly believed income is a factor in credit scores, and 24% incorrectly thought a shared cardholder’s credit affects their own score.

That’s one reason high earners benefit from choosing structured products they understand—and pairing any loan with a clear repayment plan.

Usage trends

With the housing market sluggish and consumer debt at an all-time high, many are using personal loans to improve their financial situation without compromising their liquidity. People commonly use personal loans for debt consolidation, home improvements, and everyday expenses.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Benefits of personal loans for high earners

Predictable payments and fixed terms

Most personal loans have a fixed interest rate and a set repayment period. This installment structure differs from a credit card, where the interest rate can fluctuate, and the monthly payment may vary.

A fixed-term loan allows you to budget effectively because you know exactly how much you will pay each month until the loan is paid off. This is a huge advantage, especially when credit card rates are higher than the typical personal loan rate.

Consolidation to reduce interest pressure

One of the most powerful uses for a personal loan is debt consolidation, especially when card rates are elevated. Credit card APRs now average 21.52% as of early 2026, with many new offers ranging from 20% to nearly 28%.

BHG’s survey data shows why many borrowers get “stuck” in revolving repayment: the most reported plan for paying off credit card debt was making minimum payments until the balance is paid in full—including 38% of respondents with household income above $100,000.

Swapping high-interest revolving debt for a lower-rate installment loan not only frees up monthly cash flow but also reduces the total amount of interest you pay over time—a smart way to stay ahead financially, especially as living costs continue to rise.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

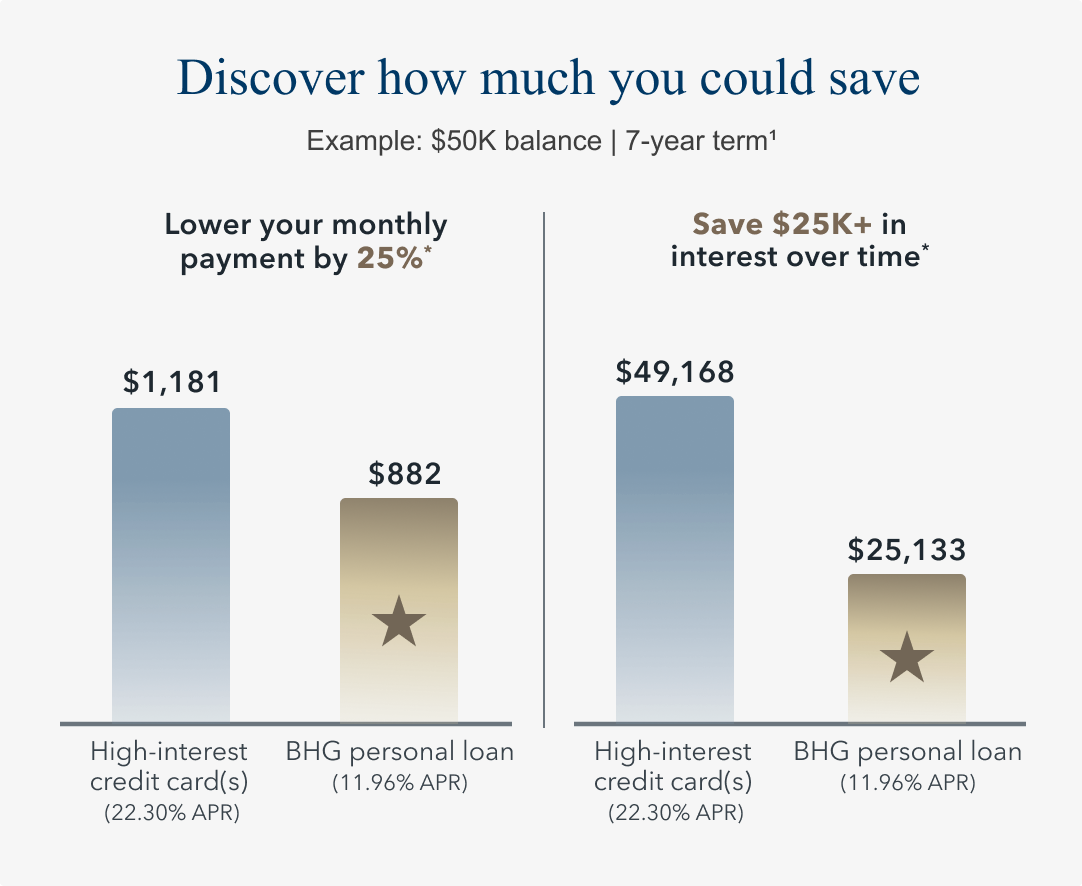

* Potential savings based off comparing repayment of a $50,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,181 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $882 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

What’s more, 12% of respondents told BHG that they plan to get (or already have) a debt consolidation loan. Those borrowers with a consolidation plan were also less likely to say they’d miss a payment.

FYI: BHG Financial offers large personal loans up to $250,0001 with no collateral required and fixed, affordable payments with terms up to 10 years.1,2 Approved applicants can unlock some of the lowest personal loan rates available in BHG’s 25-year history.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Strategic financing, not just emergency response

Finally, the usage data mentioned above suggests that high earners view financing as a strategic tool rather than a means of survival. They’re increasingly used for planned growth—funding major projects, investing in property, or covering education costs—making them part of long-term financial planning rather than a short-term fix.

Potential pitfalls to watch

Of course, no loan is risk-free. A personal loan only works in your favor if you have a clear plan to repay it and avoid slipping back into old habits. Unfortunately, TransUnion has noted that many consumers accumulate new credit card debt within 18 months, even after using a loan to pay down old accounts.

And while higher incomes provide more breathing room, they don’t eliminate risk: the Fed says delinquency rates among the highest-earning households are increasing faster than any other segment.

Rates are another factor. While prime borrowers often secure personal loans APRs of 13% or lower, that’s still a cost to weigh carefully. The key is to compare the loan’s rate with your existing debt to make sure you’re truly lowering expenses. Fixed-rate loans offer an added layer of protection, since your payments stay the same regardless of market swings.

Data‑driven checklist for high earners considering a loan

If you’re weighing the pros and cons of a personal loan, ask yourself the following questions before committing:

- Do you have a clear goal for the loan? A purposeful reason—like consolidation or planned spending—should guide the decision.

- How strong is my credit? Ensure your credit score is strong enough to secure a loan with a competitive interest rate.

- How does the APR compare? Most personal loan APRs are lower than credit card APRs—but only if you have good credit.

- Can I stay disciplined? Formulate a plan to make on-time payments and avoid accumulating new debt. Opt in for autopay when possible.

Why BHG personal loans make sense for high earners

BHG Financial offers personal loans that are designed to meet the needs of high-income borrowers.

- Unsecured: Our loans do not require any collateral.

- Fixed terms1 & payments: We provide affordable fixed-rate loans with predictable payments, which makes managing your budget simpler.

- Fast funding: If approved, you can receive funds quickly, in as few as 5 days.3

- Loan amounts up to $250,0001: We offer substantial loan amounts, much higher than many competitors, giving you the flexibility to make smart financial moves.

For six-figure earners, personal loans can be part of a long-term financial strategy to strengthen liquidity and financial resilience. The data shows they’re widely used, deliver positive results, and offer real advantages over credit cards and other forms of debt.

Ready to see what’s possible? Use our quick and easy payment estimator to get your personalized loan offers in just seconds.3

Check my rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Not all solutions, loan amounts, rates or terms are available in all states.

No application fees, commitment, or impact on personal credit to estimate your payment.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 This is not a guaranteed offer of credit and is subject to credit approval.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829