Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Why High Earners Often Get Priced Generically by Lenders—And How Smarter Debt Consolidation Changes That

Table of Contents

- FICO is strong—so why do high earners still get mispriced?

- The mispricing dilemma for high earners

- Why traditional models fall short

- What a profession-aware evaluation looks like

- How BHG Financial helps bridge the underwriting gap

- Looking ahead: Smarter data, fairer outcomes

- Accurate pricing is better lending

- Check my rate

If you've built a successful career, you probably expect your financial profile to speak for itself. And by most measures, it should. Your income is strong, your career trajectory is clear, and you understand your debt. So when lenders don’t see it that way, it can be frustrating to receive loan terms that look no different from mass‑market financing.

The models lenders use to assess borrowers were built for broad populations and tend to misinterpret financial sophistication as financial risk. High utilization across multiple accounts looks the same whether debt is being carried strategically or reflects actual repayment stress.

As a result, many six-figure earners get priced generically without any regard to the financial context that actually determines risk.

FICO is strong—so why do high earners still get mispriced?

It’s worth zooming out: overall consumer credit quality has improved meaningfully over the last two decades. FICO reports the national average U.S. FICO Score at 714, up from 687 in 2005—an unusually long upward trend by historical standards.

Key TAKEAWAY

Is credit the best it’s ever been? It’s close. Recent averages sit near record levels, with FICO noting a peak of 718 in April 2023 and now 714 in 2026.

In other words, the average borrower is grading out as “good” credit—yet that headline strength can mask pockets of stress (like rising delinquencies and elevated utilization), and it doesn’t change the core issue for high earners: a generic model can still miss context.

Well-qualified, or “prime” borrowers are frequently offered generic terms that don’t reflect their true financial profile. When high earners consolidate debt through a lender that takes a more complete view, they unlock pricing that better reflects their true creditworthiness and gain more control over their financial trajectory.

For high-income professionals, strong aggregate credit can actually make mispricing worse. When lenders tighten around a one-size-fits-all “prime” definition, borrowers with complex cash flow—bonuses, distributions, multiple tradelines, strategic leverage—can be treated like average-risk consumers even when their capacity to repay is far stronger than their bureau snapshot suggests.

That’s why high earners often need underwriting that weighs income stability, liquidity, and trajectory alongside the score.

The mispricing dilemma for high earners

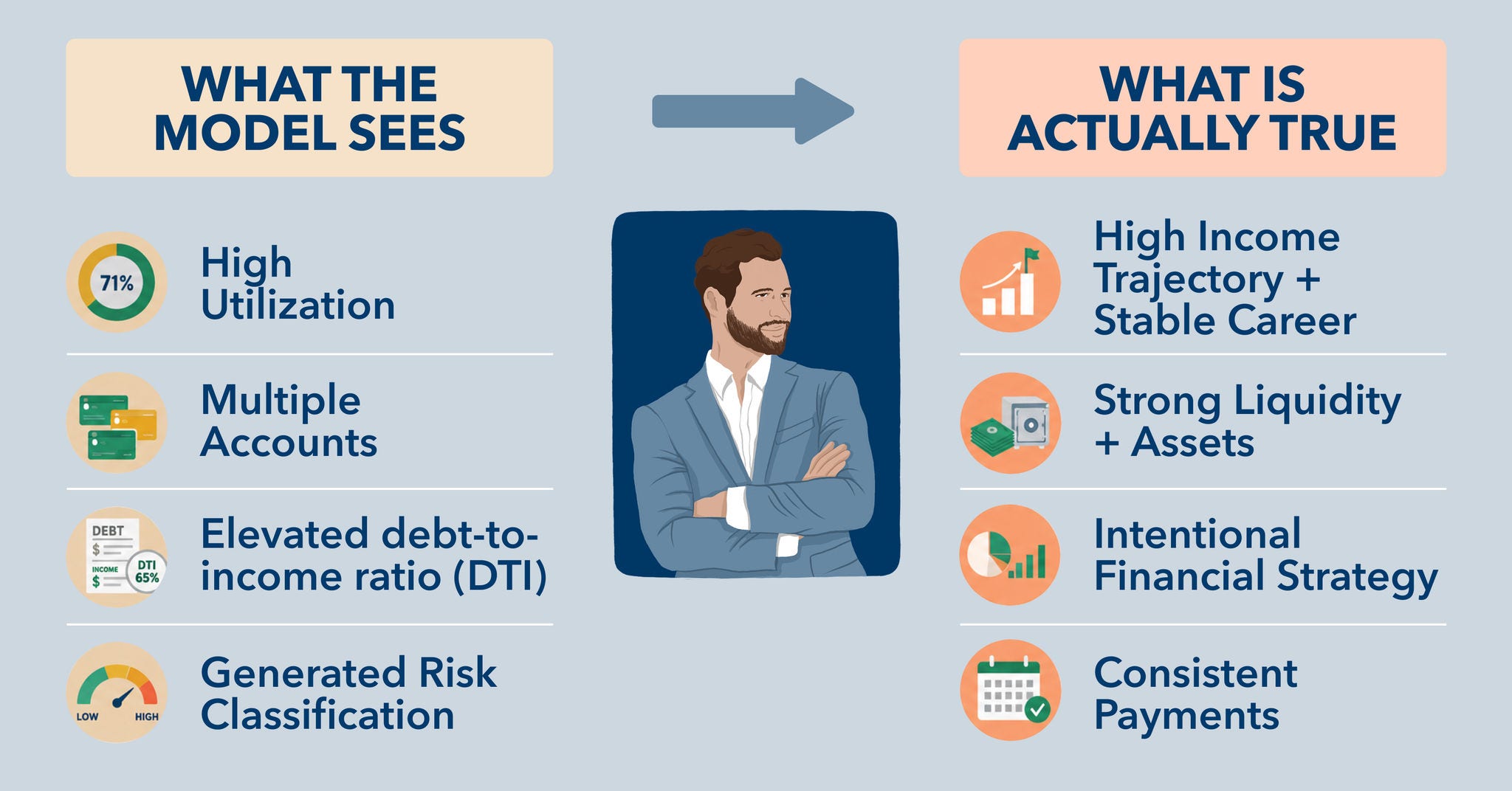

High earners are often misclassified by traditional credit models, and it shows up in their loan terms.

Take a physician carrying multiple open credit accounts alongside education debt from earlier in their career. Payments are current, and the debt is being managed deliberately—but an automated scoring system sees elevated utilization and flags it.

What the model can't discern is that those balances are easily serviceable relative to income, and that the borrower has good reasons for carrying them. Physicians often hold student debt well into practice while building reserves. Executives may prioritize investment diversification over aggressive paydown.

These are informed financial decisions—not warning signs—but the model assigns risk only based on what it can measure.

For borrowers who know they're low-risk, this is genuinely frustrating. They're offered terms and pricing designed for someone with a much weaker profile—and they know it.

Why traditional models fall short

Standard consumer credit scoring was built for scale and simplicity. It works reasonably well across a broad population, but it wasn't designed for those with high but variable incomes.

Several structural limitations contribute to mispricing:

- Revolving utilization is evaluated as a snapshot. Models penalize high utilization even when that debt is being managed strategically or is easily serviceable relative to income. Carrying a balance isn't the same as struggling with one.

- Incomplete view of income and liquidity. High earners may hold significant unreported assets, non-W2 income, or business interests not visible to consumer credit bureaus. The model has no way to account for it.

- Risk profiles don't update in real time. Many algorithms are slow to reflect changes that can impact credit, such as someone who's recently paid down substantial debt or seen a significant increase in income.

What a profession-aware evaluation looks like

When a lender looks beyond standard metrics, the picture changes considerably. Assessing income consistency, professional tenure, career stage, and overall financial trajectory gives underwriters the context a model alone can't provide.

A “professional-aware” evaluation recognizes that financial strength can also be captured by analyzing how income is earned, how it fluctuates, and how borrowers allocate capital over time.

An executive earning through quarterly distributions, for example, may look riskier on paper than their actual position warrants. When evaluated with that context, these borrowers are strong candidates for premium credit pricing and loan structures that fit how they actually manage money, like debt consolidation.

The case for debt consolidation tailored to high earners

High earners often consolidate debt for practical reasons, not financial distress. As life evolves, their finances become more complicated than they need to be and no longer tell the full story of how strong their position really is.

A debt consolidation loan is often (and accurately) framed as a simplification tool. Fewer payments and a single fixed rate make cash flow easier to manage. However, consolidation also creates an opportunity for lenders to evaluate risk more accurately.

When that loan is underwritten holistically, it unlocks terms that finally reflect the borrower's actual profile rather than a model's approximation of it.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

How BHG Financial helps bridge the underwriting gap

BHG Financial was built to serve professionals whose financial complexity exceeds what standard models can evaluate. Our underwriting process reflects 25 years of refinement, combining data analytics with human review, so context is never lost in translation.

For high earners consolidating debt, that means a few things:

- Holistic credit assessments. Income consistency, professional tenure, and overall financial trajectory factor into the assessment, allowing us to distinguish between temporary leverage and structural risk. Given the holistic nature of our underwriting, BHG may be willing to lend to borrowers with elevated DTIs if their profile supports it.

- Terms built around how professionals actually earn. Loan structures can reflect bonus schedules, partnership distributions, or career-specific cash flow patterns, rather than forcing borrowers into one‑size‑fits‑all repayment plans.

- Experienced underwriters, not just algorithms. Data provides insight, but human judgment ensures borrowers are evaluated as individuals. Our relationship-driven processes are part of the reason why BHG customers rate us 25% higher than our competitors.

The outcome is tailored consolidation: high-rate revolving debt rolled into a single fixed-rate loan solution, with improved cash flow and pricing that more accurately reflects your earning stability. While longer terms don’t always mean faster payoff, they often create a clearer, more sustainable path forward.

Over time, responsible consolidation can also improve a borrower’s credit profile. Most borrowers who consolidate debt through BHG improve their FICO score by 30 points or more within a few months of funding as revolving utilization declines and payment behavior stabilizes.*

Looking ahead: Smarter data, fairer outcomes

The future of lending is moving toward more adaptive frameworks using systems that integrate real-time income data and professional indicators rather than static snapshots.

At BHG Financial, we’ve long taken a comprehensive approach to underwriting, evaluating income strength, professional stability, and future potential alongside traditional credit metrics. As the adoption of VantageScore 4.0 expands across the lending ecosystem, it will become part of our evaluation framework as well—a natural extension of the holistic view we already apply to every borrower.

For professionals actively improving their debt profile, this evolution will help them become better positioned financially and recognized as stronger candidates by more lenders, with access to larger loan amounts and more favorable terms.

Our vision remains consistent at BHG: continue integrating predictive analytics with empathy‑driven underwriting, and lead the market in transparent, profession-aware lending experiences.

Accurate pricing is better lending

High earners deserve credit terms that reflect their genuine stability, not just outdated score metrics built for a different borrower.

BHG’s debt consolidation approach reduces mispricing by combining professional insight with sound lending science. For clients, that means getting pricing that matches the risk you actually represent, and using that foundation to build toward long-term financial goals with clarity.

If you've felt like your loan terms don't reflect the borrower you actually are, it may be worth exploring what a more complete evaluation looks like. Estimate your monthly payment with no impact on your credit score.1

Check my rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

*Based on internal data, most BHG debt consolidation borrowers may improve their FICO® score by 30+ points within 2 months. Credit scores depend on many factors and individual results may vary based on personal spending habits.

Not all solutions, loan amounts, rates or terms are available in all states.

1 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829