Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Buffett Says This Comes Before Investing—Why High Earners Should Rethink Credit Card Debt Now

In a world obsessed with market returns and portfolio strategy, Warren Buffett just gave investors advice that has nothing to do with picking stocks.

It has to do with paying off your credit cards.

During a recent interview highlighted by Inc., Buffett said that if he owed money at 18%, the first thing he’d do with any extra cash would be to pay it off. In his words, doing so would be “way better than any investment idea I’ve got.”

For high-earning professionals juggling multiple financial priorities and high-interest obligations, it’s a message worth sitting with.

Because there’s a certain kind of financial pressure that can exist even when income is strong. You earn well. You invest consistently. You think long-term. And yet, a few revolving balances lurk quietly in the background—charging 18%, 20%, sometimes more.

To put it plainly: high-interest credit card debt is a guaranteed drag on wealth.

This article breaks down why—and how restructuring that debt can strengthen your financial foundation before you chase another percentage point in the market.

The financial math behind Buffett’s advice

Buffett’s logic is simple. High-interest credit card debt can outpace predictable investment returns.

Credit card APRs for prime borrowers often fall between 11% and 22%, with averages for all cards hovering near 20%, according to recent Consumer Financial Protection Bureau data. That means every dollar carried month to month accrues interest at a double-digit rate.

An 18% interest rate on debt is a guaranteed 18% cost.

Very few investments offer return you can lock in at that level. In fact, the stock market has returned an average of 8% to 11% over the past 50 years give or take. Some years are strong while others are flat—or worse.

So, you’re faced with a choice.

If you had $1,000 to spare, would you invest it all expecting a potential 10% gain? Or use that same $1,000 to eliminate an 18% interest charge?

- Invest $1,000 at 10%: You might earn $100.

- Pay off $1,000 at 18%: You avoid (save) $180 in interest.

One outcome depends on market performance. The other improves your position immediately. Paying off high-interest credit card debt functions like earning a risk-free return equal to the interest rate you’re eliminating. That’s why Buffett calls it better than any investment idea he can offer.

And yet, many successful earners delay addressing revolving debt.

Why? Because the minimum payments feel manageable. Income is strong. Therefore, the pressure to pay more toward the balances doesn't seem quite as urgent.

But compounding interest doesn’t slow down just because you’re comfortable. It snowballs either way.

What this means for high earners

Using a credit card is okay, if you pay it off at the end of each month. But for high-earners—many of whom have variable incomes, assets tied up in investments, and/or significant monthly obligations—paying credit card balances in full each month isn’t always realistic.

High income provides flexibility. It does not provide immunity. You can have strong earnings and still experience limited liquidity in a given moment.

In many cases, this has less to do with spending habits and more to do with timing. Bonuses that haven’t hit yet. Capital committed to long-term investments. Opportunities that required upfront funding.

This gap is why it’s so easy for many to let expensive revolving debt linger in the name of competing priorities.

Buffett’s message is a reminder to start with fundamentals. Before expanding investment strategies, address the cost of capital working against you. Strategic debt management should be viewed as a foundational financial move, not as a last resort.

Debt consolidation as a smart financial tool

There’s a misconception that debt consolidation signals financial trouble. For established professionals, it’s often the opposite.

If multiple high-interest balances are charging 17%, 19%, or more, consolidating them into lower-rate options (such as fixed-rate personal loans) introduces structure. Debt consolidation can:

- Dramatically reduce interest costs

- Free up monthly cash flow

- Create one predictable monthly payment

- Establish a clear payoff timeline

This approach directly helps you pay down expensive debt faster—aligning with Buffett’s core advice on trimming high-interest obligations first.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

How BHG’s philosophy aligns with Warren Buffet’s core message

Like BHG Financial, Buffett isn’t anti-debt. He’s anti-expensive debt.

Debt used strategically can preserve liquidity and protect long-term investments, whereas debt left revolving at double-digit interest rates does the opposite. By consolidating high-interest credit card balances into a lower fixed rate, you reduce that drag and bring predictability back into your cash flow.

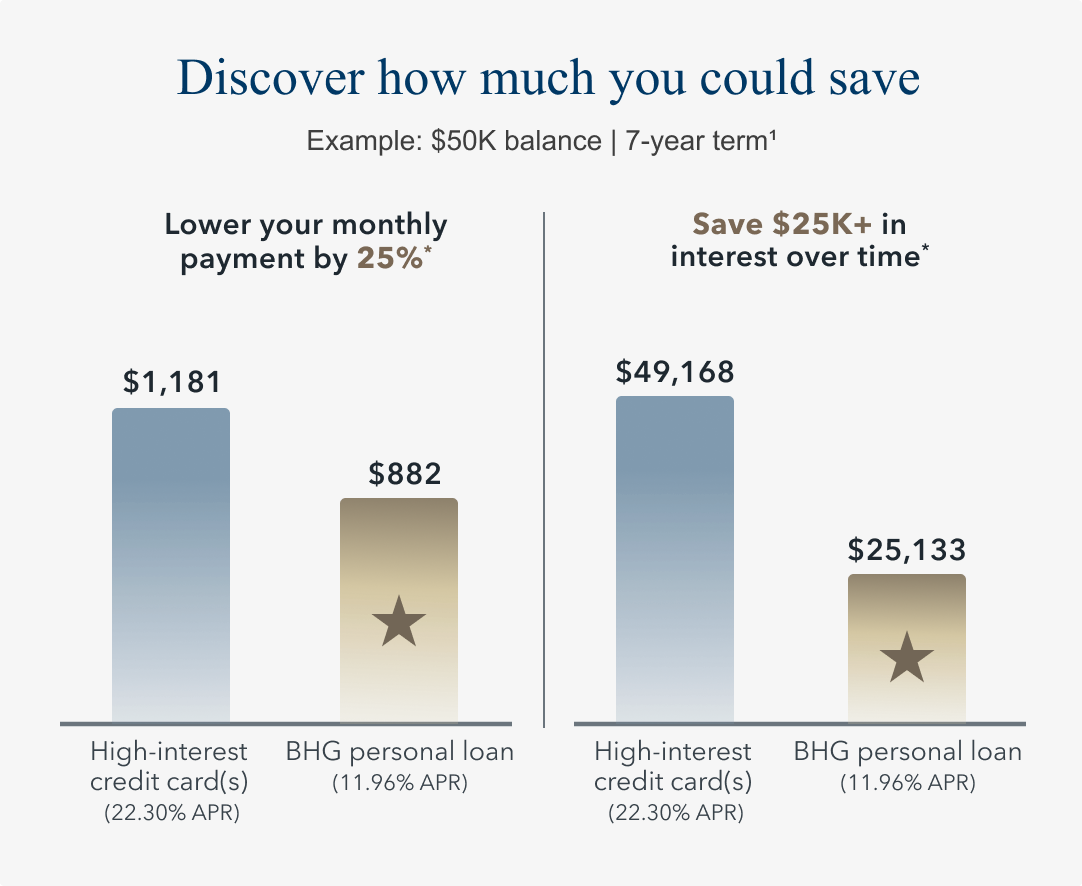

Consider a simple example, in which you consolidate high-rate debt with a $50,000 personal loan from BHG. Here, you:

- Reduce your monthly payment by $287 (24%)

- Save $24,000 in total interest over time

- Secure a defined end date instead of an open-ended payoff cycle

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $50,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,181 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $882 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

This is both a mathematical advantage and a mental shift. When debt is structured and predictable, it stops competing with your long-term plan, so you can allocate capital intentionally instead of reacting to rising balances.

Beyond repayment: Reclaiming financial momentum

At BHG Financial, we work with high-credit, high-income professionals every day. Many are surprised by how much flexibility they regain once high-interest debt is reorganized.

With large, unsecured personal loans1 and extended fixed terms1, qualifying borrowers can:

- Consolidate substantial balances

- Secure predictable monthly payments

- Preserve liquidity rather than tapping investments prematurely

From there, the conversation shifts toward the future. You can:

- Invest with greater confidence

- Strengthen emergency reserves

- Improve credit utilization

- Plan strategically rather than reactively

Take Warren Buffett’s advice a step further with BHG’s help

If you’re carrying high-rate credit card debt, paying it down often delivers a stronger financial outcome than chasing incremental gains in the market. The next step is simple.

Review your current APRs and calculate what those balances are costing you annually. Then, compare that with what a structured, fixed-rate personal loan for debt consolidation could look like.

Because sometimes the smartest investment isn’t doing something new, it’s strengthening the foundation you already have.

BHG Financial offers fixed-rate personal loans for debt consolidation tailored to your needs, with amounts up to $250,0001 and flexible terms of up to 10 years.1,2 Plus, you’ll enjoy dedicated, U.S.-based concierge service that respects your schedule and your goals.

Ready to see what’s possible? Get your personalized loan offer in just seconds,3 with no impact to your credit score.4

Check my rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 This is not a guaranteed offer of credit and is subject to credit approval.

4 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829