Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

When to Pay Credit Card Bill to Increase Credit Score

Paying your credit card bill may seem simple: make at least the minimum payment by the due date to avoid late fees. However, if your goal is to raise your credit score fast, there’s more to consider than just avoiding penalties. Strategic timing—especially paying before your statement closing date or even paying twice a month—can significantly impact your credit utilization and, by extension, your credit score.

Most borrowers who consolidate debt through BHG improve their FICO score by 30 points or more within a few months of funding.

Let’s walk through why timing matters, how to identify the best date to pay your credit card bill, and how these strategies can help you build stronger credit faster.

Key Considerations

- As a general rule, you should pay your credit card bill by the due date to avoid late fees and negative impacts on your credit score.

- If you tend to carry balances from month to month, paying it early before the billing cycle may save interest.

- If you have a high balance, making multiple payments a month can help lower your utilization ratio, and in turn, raise your credit score.

- Understanding your statement closing date is an essential part of your credit-building strategy. Consider tools like autopay or financial apps to stay on track.

What is your statement closing date?

The statement closing date indicates the end of your billing cycle. On the last day of your billing cycle, your credit card issuer will finalize all charges, payments, and credits and calculate the total amount you owe for that cycle.

Your statement closing date and payment due date are not the same. The payment due date is the deadline by which you must make at least the minimum payment toward the balance to avoid late fees.

You also have a grace period, usually 21 to 25 days, between your statement closing date and your payment due date. If you pay your full balance during this time, you won’t incur interest.

Understanding the credit card billing cycle

Understanding the best time to pay credit cards starts with understanding how the billing cycle works. If your credit card closing statement date is the first of every month, then:

- On January 1, the card company generates a statement detailing your transactions from December 1 to December 31. This balance will then be reported to the credit bureaus shortly after.

- If your grace period is 21 days, your payment due might be January 21. You’ll need to make a payment toward the statement balance on or before this day to avoid late fees.

FYI: Making minimum payments on time keeps your account in good standing, but interest will still accrue on the remaining balance. Paying your credit card off in full during your grace period will help you avoid charges and protect your credit score.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

When is the best time to pay your credit card?

The general rule of thumb is to always pay your credit card bill by the due date. This prevents late fees, interest charges, and negative marks on your credit report, which can seriously damage your credit score.

Missing a payment, even by a day, can trigger notoriously excessive late fees that strain monthly budgets. Late fees now average $41 per late payment, according to the Consumer Financial Protection Bureau (CFPB). And even though the CPPB finalized a rule that would cap late fees on credit cards to just $8 in 2024, the motion was vacated in May 2025.

Why payment timing matters for your credit score

Strategically timing your credit card payments can help you avoid card charges and protect your credit score. Here’s how timing plays a role.

Credit card issuers typically report your balance to the three major bureaus (Experian, Equifax, and TransUnion) shortly after your statement closing date—not the due date.

If you consistently pay off your card after the statement closes, you may still show a high utilization rate to the credit bureaus. (Credit utilization makes up 30% of your FICO score.) Keeping your utilization below 30% can improve your credit score over time.

Also, paying your credit card in full and on time each month strengthens your credit score by building a strong payment history—the most important factor, making up 35% of your FICO score.

Making payments on time is non-negotiable for good credit. In some cases, paying early could also help your score. You should pay your card early if:

- You carry a balance on your credit card from month to month. Paying before the due date can help reduce interest charges.

- Your balance regularly exceeds 30% of your credit limit. Early payments improve credit utilization before it gets reported and protect your score.

Here’s how it works:

Let’s say you have a credit card with a $15,000 limit. If your balance before the statement closes is $9,000—that’s 60% utilization. However, if you pay $7,500 before the statement closes, your reported balance is only $1,500. That drops your utilization to 10%, which can lead to an improved credit score.

Should you pay multiple times a month?

If you can afford it, pay your credit card more than once per month. It will help you manage your credit utilization and overall credit health. This is because paying your credit card balance more than once a month makes it more likely that you’ll have a lower credit utilization ratio when the bureaus receive your information.

It may be a good idea to make multiple payments during your billing cycle if:

- You have a higher-than-normal balance relative to your available credit limit.

- You want to avoid interest charges or reduce debt more aggressively.

- You’re actively working on improving your credit score.

The 15/3 rule

For those who want to pay credit cards twice a month, the “15/3 rule” may be a good strategy. The 15/3 rule suggests making two payments during your billing cycle: one payment 15 days before the statement closing date and another payment three days before the closing date.

This tactic keeps your balance consistently low throughout the billing period, ensuring that your reported balance is minimal when your statement closes.

You don’t have to follow this exact schedule but making multiple smaller payments before the statement is issued helps improve credit utilization.

How BHG helps you manage your credit strategy

Managing multiple credit cards and due dates can be overwhelming—especially if you're juggling interest charges and high balances. In this instance, getting a personal loan for debt consolidation may be a smart solution for managing credit more strategically because it can help you save money and streamline your finances.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

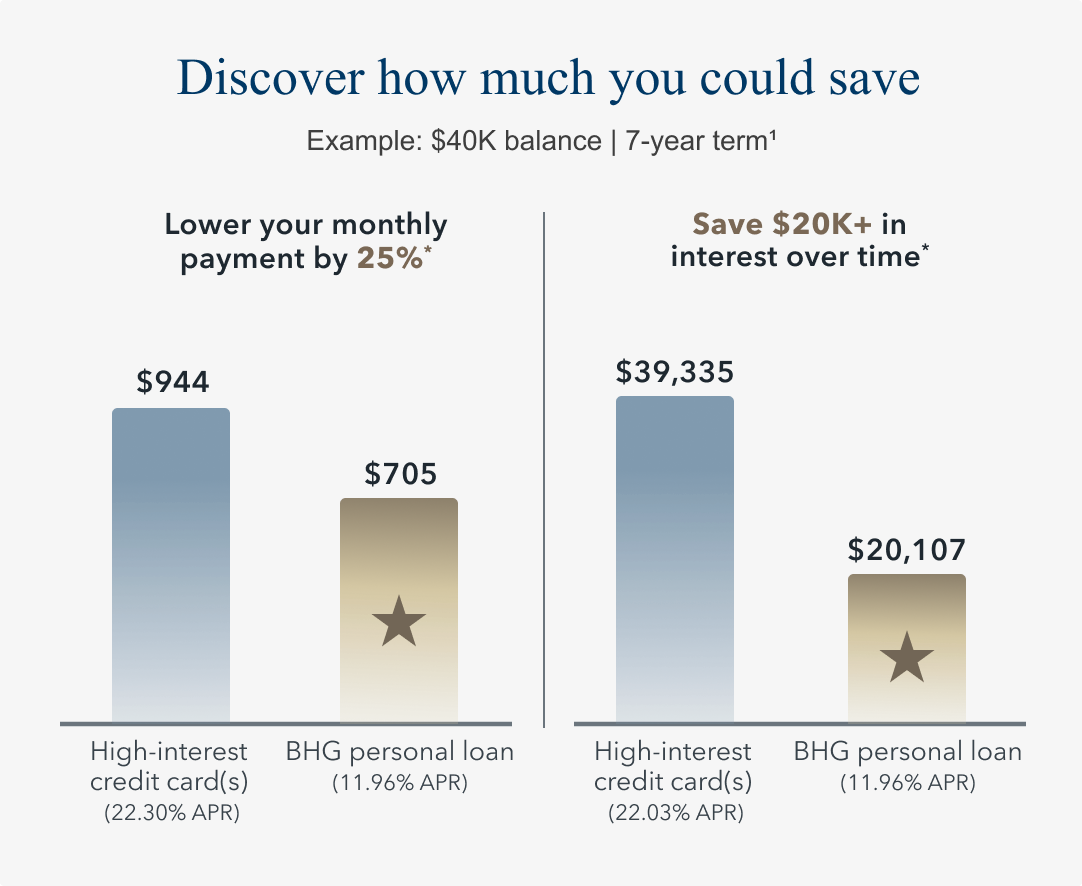

* Potential savings based off comparing repayment of a $40,000 balance over 7 years on both a credit card with a minimum monthly payment of $944 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $705 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

BHG Financial offers flexible loan options that can help:

- Potentially secure a lower rate compared to typical credit card APRs.

- Consolidate multiple payments into one manageable monthly payment.

- Finance significant debt, up to $250,0001.

- Choose flexible repayment terms that fit your budget,2 reducing the risk of missed payments.

- Maintain credit by making on-time payments consistently.

Ready to see what’s possible? Use our quick and easy payment estimator to get your personalized loan estimate in just seconds. There’s no impact on your credit score to check your rate.3

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

When to pay credit card bill to increase credit score FAQ

Does paying your credit card bill early raise your score?

Early payment and credit score improvement are often linked. Paying your credit card bill early, especially before your statement closing date, can positively impact your credit score by lowering your utilization ratio. This is because the balance reported to the credit bureaus will be lower.

How do I know my statement closing date?

You can find your statement closing date on your monthly credit card statement. It's usually listed along with your payment due date and billing period details.

Can I pay my credit card bill more than once a month?

Yes, you can absolutely pay your credit card bill more than once a month. In fact, paying credit cards twice a month can be a smart strategy to keep your credit utilization low and potentially improve your score, especially if you carry a higher balance.

Will this method work if I carry a balance?

Yes, this method can still be beneficial if you carry a balance. Even if you can't pay your full balance, making payments throughout the month or paying as much as you can before your statement closing date will reduce the amount of interest you're charged, as interest is usually calculated on your average daily balance.

What tools can help me track payments?

There are several tools that can help you track credit card payments, including setting up autopay with each issuer, adding reminders to your digital calendar in Google or Outlook, and enabling credit card app notifications. You can also use budgeting tracking apps like Mint or Monarch Money to track your spending and set payment reminders.

Recommended articles

Personal Loans

Personal Loan vs Credit Card: The Surprising Way to Cut Interest Costs

June 23, 2025 | 6 min read

Debt Consolidation

7 Key Factors That Determine Eligibility for High‑Limit Debt Consolidation Loans

January 12, 2026 | 7 min read

Debt Consolidation

Can Debt Consolidation Improve Your Credit Score?

December 10, 2025 | 7 min read

Personal Loans

Should You Dip Into Savings or Use a Loan? How to Decide

October 14, 2025 | 6 min read

Debt Consolidation

How to Improve Your Credit Score: Essential Tips for 2025

August 8, 2025 | 6 min read

Debt Consolidation

How Consolidating Debt Can Free Up Cash for Bigger Goals

November 6, 2025 | 6 min read

*Based on internal data, most BHG debt consolidation borrowers may improve their FICO® score by 30+ points within 2 months. Credit scores depend on many factors and individual results may vary based on personal spending habits.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 This is not a guaranteed offer of credit and is subject to credit approval.

3 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829