Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Will the Next Recession Hit High Earners the Hardest?

Table of Contents

- What do we mean by “high earner” and “recession”?

- Why recession risk is still on the table now

- Why the next recession could hit high earners especially hard

- Why high earners still have an edge

- How to recession-proof your finances as a high earner

- How BHG Financial supports high earners in uncertain times

- Check my rate

Economic cycles tend to follow familiar patterns, but early indicators show the next downturn may challenge long-standing assumptions about who is most at risk. According to S&P Global, one in four American workers laid off in 2024 came from professional and business services—the sectors typically associated with higher-earning, white-collar roles. Analysts link this trend to high interest rates, automation, and AI reshaping office jobs.

At the same time, more than half (55%) of respondents said they think the likelihood of the U.S. entering a recession will increase, according to BHG Financial’s 2026 Consumer Debt & Finances Survey. Two in five think incomes will stay the same, and 44% think that the job market will decline (fewer jobs available).

Many high earners are entering this period with less financial cushion than they expect. Prices are still high, wage growth has largely stalled in real terms, and everyday costs are consuming more of each paycheck—even at six-figure income levels.

This raises an important question: Are high earners actually more exposed in the next downturn than they realize?

In this guide, we’ll explore how slowing economic growth, shifting labor dynamics, and rising household debt could affect high-income professionals—and outline practical steps to strengthen financial stability, from stress-testing cash flow to consolidating high-interest debt before conditions tighten further.

What do we mean by “high earner” and “recession”?

Defining “high earners” in today’s economy

High earners make six-figure incomes—typically $100,000 to $250,000 or more. Using the DQYDJ’s most recent household income percentile calculator, households in the top 25% earn roughly $175,000 or more.

High income, however, does not always translate into high net worth, strong liquidity, or financial peace. And while 72% of six-figure earners consider themselves “financially comfortable,” according to BHG survey data, earning more doesn’t make finances any less complicated. Many high earners live in high-cost cities while also juggling mortgages, childcare, elder care, and high-rate credit card debt—leaving less margin than expected when uncertainty arises.

In this type of economy, high earners may be forced to choose between lifestyle changes and racking up debt, hoping that things will get better.

What a recession looks like in real life

A recession is a broad decline in economic activity, typically marked by rising unemployment, slowing consumer spending, and weaker business investment.

Recent trends from the S&P suggest the next recession may skew more “white-collar” than usual. Professional layoffs have increased, while lower-wage sectors remain comparatively stable. At the same time, the quits rate fell to 1.9%—its lowest since June 2020—indicating that workers are more cautious and holding on to existing roles as opportunities narrow.

The current economic backdrop: Why recession risk is still on the table

Forecasts for early 2026 point to slower economic growth, stubborn inflation, and a sluggish labor market. As a result, consumer spending is expected to slow as household budgets tighten across all income brackets. Nearly two in five people (38%) of respondents are somewhat or very likely to miss a minimum debt payment in the next six months. Among high-income earners, 38% said the biggest challenge to achieving the American Dream is wages not keeping up with inflation and cost of living.

In BHG Financial’s 2026 survey, the majority of Americans think a recession is likely, and 65% said economic uncertainty is making it harder to make sound financial decisions.

Slower growth, elevated uncertainty

A Reuters poll puts the 12-month probability of a recession at 45%, fueled by tariff concerns, elevated inflation, and slowing corporate investment. Economists also expect inflation to remain above the Federal Reserve’s 2% target until at least 2027.

While inflation has cooled from its peak during COVID-19, prices are not falling—they’re just rising more slowly. In fact, since 2020, wages adjusted for consumer spending have been largely flat, according to analysis from the Hamilton Project.

Food costs alone are nearly 24% higher than in 2021, according to USDA data. For high earners, this doesn’t break the budget—but it quietly erodes flexibility month after month.

Tariffs have also added pressure to the everyday budget. The Yale Budget Lab reports that the average tariff rate has climbed to 17.4%, the highest since 1935—costing American households an estimated $2,000 more this year for essential goods and services.

Household debt at record highs

Simultaneously, debt levels continue to climb. The Federal Reserve Bank of New York reports that U.S. household debt hit $18.6 trillion in Q3 2025—up $197 billion in just one quarter.

Credit card balances alone rose $24 billion and now total $1.23 trillion. This is 5.75% higher than the level one year ago. BHG found that 31% of Americans have used a credit card to cover a financial shortfall, not to collect points.

With higher balances, any income disruption—especially for those relying on bonuses or stock-based compensation—debt often becomes the pressure valve.

Rising delinquencies and persistent price pressure

Many high earners use credit cards strategically, but higher APRs make carrying balances riskier. With average APRs above 21%, even responsible use becomes expensive when cash is stretched across mortgages, childcare, healthcare, and rising everyday costs.

The percentage of people who are delinquent on credit card debt has risen steadily since 2021. While this pace has recently slowed, the trends highlight ongoing financial distress, even for those in higher-income brackets. Americans also continue to cite inflation as their top financial concern, according to both the Federal Reserve’s SHED report and recent Gallup polling.

Confidence is fragile, even for higher-income households

The combination of modest wage gains, higher prices, and rising debt may help explain why a growing share of Americans are feeling confident and strained simultaneously. While most respondents feel optimistic about their financial future, only 49% said they could cover a $1,000 emergency expense from checking or savings, and just 33% said they could cover a $10,000 emergency that way. Among six‑figure households, more than a quarter reported having less than $10,000 across their bank accounts.

For high earners—whose expenses tend to be larger and tied to family obligations—this uncertainty often drives a desire to protect their position, maintain momentum, and make intentional financial decisions that support long-term goals, even when income doesn’t stretch as far as it once did.

Why the next recession could hit high earners especially hard

High income brings advantages, but it doesn’t eliminate risk in uncertain economic environments. Instead, it forces difficult choices: adjust lifestyle expectations, dip into savings, or rely on debt and hope conditions improve.

High fixed costs and complex financial commitments

High earners often carry sizable recurring expenses: large mortgages in expensive markets, private school tuition, vehicle leases, and elder-care support. BHG Financial data reinforces how fixed expenses can limit flexibility: mortgages and groceries were the most commonly cited largest expenses, and a meaningful share of respondents (13%) also pointed to credit card debt as their biggest monthly obligation.

When bonuses shrink, or a layoff hits, these fixed costs can quickly exceed available cash flow.

Concentration in volatile sectors

Many high earners work in sectors whose hiring cycles mirror economic shifts: tech, consulting, retail management, and corporate services. Professional and business services alone accounted for 25% of recent U.S. layoffs, according to S&P Global.

These industries are also more likely to be impacted by AI-driven automation, downsizing of middle-management roles, and shifts in office-based employment.

Equity-heavy compensation and market swings

For professionals whose income relies on stock compensation, bonuses, or equity payouts, planning becomes more challenging. When markets fall, both compensation and portfolio values can decline at the same time—reducing liquidity precisely when it’s needed most and impacting net worth.

When borrowing costs rise

Some high earners maintain variable-rate debt (e.g., credit card balances, personal credit lines, or even margin loans) under the expectation that income will remain stable. But when interest rates stay elevated, these balances grow more expensive. For example:

- Variable-rate debt. Variable interest rates change based on market benchmarks. Even a small shift in APRs (from 18% to 21%) can increase the monthly interest charges on large balances.

- Margin loans. These allow investors to borrow against their portfolios to boost their investment capacity, using the portfolios as collateral. But this can be risky when markets fall. Lenders may issue a margin call—requiring borrowers to deposit more funds or sell investments at a loss to maintain minimum account levels.

The bottom line: When household debt is at record highs and delinquencies are rising, complacency is dangerous. Luckily, high earners have solutions at their disposal that they can use to strengthen their position proactively.

Why high earners still have an edge

The outlook isn’t all doom-and-gloom. High earners have real advantages that can make them more resilient and accelerate recovery.

Higher earning power and faster recovery

Professionals tend to have more leverage in the job market. They can often negotiate stronger compensation packages, tap into extensive networks for new opportunities, or transition more easily into consulting or contract work by leveraging their professional background and experience. Their higher earning potential also allows them to rebuild savings more quickly once income stabilizes.

Better access to credit and advice

In addition, high earners typically maintain stronger credit profiles, giving them:

- Access to lower rate borrowing options

- Flexibility to refinance or consolidate debt

- Opportunities to consult financial advisors and tax professionals who can help manage liquidity during transitions

Used strategically, this creates real advantages. For example, consolidating higher-rate debt into a single personal loan with a fixed rate and a predictable repayment timeline can free up cash flow during slower periods.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

How to recession-proof your finances as a high earner

Stress-test your cash flow and build liquidity

Start by mapping out all fixed monthly obligations and all income streams, including bonuses and variable compensation. Then, run “what-if” scenarios:

- What if I experience a 25% to 50% drop in income?

- What if I go six months without earning a bonus?

- What if my job search takes longer than expected?

Aim for an emergency fund covering three to 12 months of essential expenses, especially if you’re in a high-cost metro or are a single-income household. Should a recession bring layoffs, it’s important to have ample savings to cover longer job search timelines: the share of Americans defined as long-term unemployed (27+ weeks) has risen to 26%, the highest in more than three years.

Given Pew’s finding that only 48% of Americans have a three-month buffer, high earners should aim to exceed this benchmark.

Manage and consolidate high-interest debt

While reducing discretionary spending or delaying a large purchase helps, it’s important to address high, variable costs that cut into your savings.

High-interest revolving debt (especially credit cards and personal credit lines) is particularly dangerous during a recession. As rates rise:

- Minimum payments increase

- Variable rates remain unpredictable

- Delinquency risk rises (as shown by St. Louis Fed data)

This is where debt consolidation can help reorganize and optimize your finances. By moving multiple high-rate balances into one fixed-rate personal loan, you streamline payments and potentially lower total interest. Improved cash flow can be redirected to emergency savings or long-term goals.

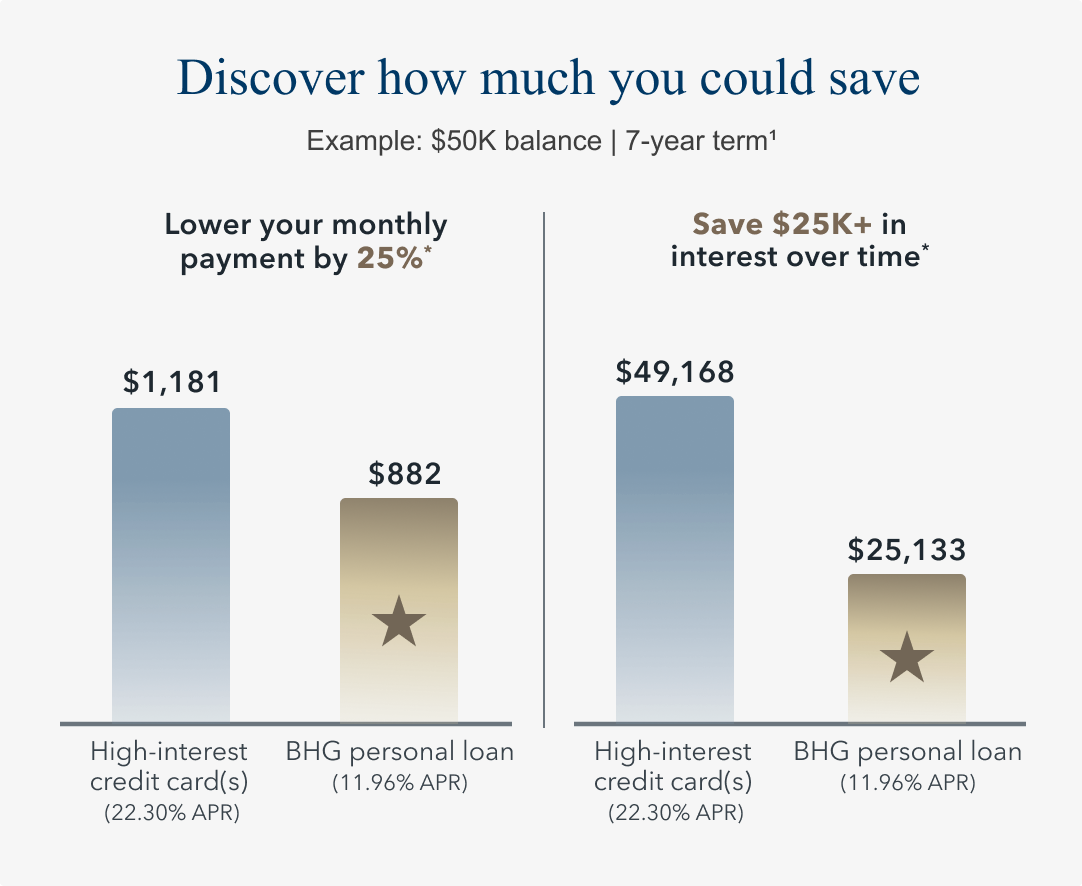

For example, here’s how using $50,000 loan to consolidate debt can lower your monthly payments and total interest:

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $50,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,181 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $882 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

Using a BHG Financial personal loan for debt consolidation

BHG Financial specializes in serving high-income professionals who want premium lending solutions. Qualified borrowers can unlock competitive fixed rates compared to many credit cards and predictable monthly payments. Plus, BHG’s large personal loans are designed to support higher incomes and complex cash-flow needs. Borrow up to $250,0001 with flexible loan terms up to 10 years.1,2

For many high-income professionals, a BHG Financial personal loan is often their go-to option for debt consolidation, thanks to competitive rates, industry-leading terms,1 and a streamlined experience tailored to busy professionals.

See how a BHG Financial personal loan could help you consolidate high-interest debt. Checking your rate won’t impact your credit score.3

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Diversify your income streams

Adding secondary income can strengthen financial resilience. High earners often have expertise that translates into:

- Consulting or advisory work

- Teaching, speaking, or writing

- Building investment income over time

Start considering how to build these passive income streams before a downturn, when you still have capacity and leverage.

Protect your career capital

Investing in career progression is one of the strongest recession strategies. Use these tips to strengthen your position, so you can reenter the job market faster, if needed:

- Upskilling in areas resistant to automation

- Expanding your network inside and outside your industry

- Keeping an updated resume on hand and maintaining a polished LinkedIn profile

- Nurturing strong professional relationships with mentors, sponsors, and recruiters

How BHG Financial supports high earners in uncertain times

Tailored solutions for high-income professionals

BHG Financial provides lending solutions designed specifically for high-credit, high-income professionals with complex financial profiles. Rather than a one-size-fits-all approach, BHG offers personalized guidance, holistic underwriting, and loan structures suited for the unique cash-flow patterns of prime borrowers.

When a BHG personal loan makes sense

A personal loan from BHG can support your financial goals when you want to:

- Consolidate multiple high-interest debts into one predictable monthly payment

- Lock in a fixed rate before credit conditions tighten

- Strengthen your liquidity strategy and simplify repayment

- Rebalance your financial plan to avoid accumulating new debt

Explore whether a BHG Financial personal loan is the right tool to help you recession-proof your finances. Get your instant loan options in seconds.4

Check my rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

4 This is not a guaranteed offer of credit and is subject to credit approval.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829