Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Can You Consolidate Debt Without a Loan? Pros and Cons of the DIY Approach

Table of Contents

For many high-earners, debt can feel like a contradiction. You have a strong annual salary, but multiple high-interest payments—from credit cards to personal loans to student debt—chip away at your hard-earned income. It’s natural to want a simpler, faster way to get ahead without borrowing more.

The idea of DIY debt consolidation, a "do-it-yourself" approach to paying down debt using tools you already have, can be tempting. But before you dive in, it’s worth understanding when these methods work best—and when a structured personal loan might deliver greater savings, stability, and peace of mind.

Key takeaway

Yes, you can consolidate debt without a loan using DIY strategies like budget restructuring and debt snowball or avalanche methods. These approaches can work for smaller balances, but they often take longer, require strict discipline, and may not lower your interest enough to make a big impact. Those with larger or higher-interest debts may prefer a structured personal loan that simplifies repayment, reduces total interest, and protects their financial flexibility.

Why consolidate debt in the first place?

The goal of debt consolidation is simple: to take control of your financial picture. Many professionals, even those with higher incomes, have multiple types of debt—often with interest rates north of 20%.

This creates messy, complicated finances that are easy to lose track of. The objective of consolidation is to streamline these obligations into one manageable payment. By simplifying your finances, you can:

- Reduce your interest rate: This is often the primary driver. Consolidating into a lower-rate product can save you thousands of dollars over time.

- Simplify your payments: Instead of juggling multiple bills with different due dates, you have one predictable monthly payment.

- Improve your cash flow: A lower, fixed monthly payment frees up more of your income for other priorities, like savings, investments, or everyday expenses.

A common option for consolidating high-rate debt is using a personal loan. However, some prefer to avoid new credit entirely, which is where the DIY approach comes in.

Common DIY debt consolidation methods

A DIY approach to debt consolidation means managing your debt without taking out a new loan. Here are several ways to do it:

1. Debt snowball or avalanche methods

The debt snowball and avalanche methods focus on aggressively paying down a specific debt without taking on any new credit. Here, you’d make the minimum payments on all your debts, while applying more cash to one specific debt.

The snowball method targets the smallest balance first, regardless of the interest rate. Once that's done, you "snowball" the money you were paying on that debt into the next smallest one. This creates a sense of momentum and accomplishment.

The avalanche method focuses on the debt with the highest interest rate first, which saves you the most money over time. Once that debt is gone, you "avalanche" that payment onto the next highest-interest debt. This is the most financially efficient approach.

Pros:

- No new credit needed

- Builds motivation and accountability

Cons:

- Requires high cash flow and discipline

- Doesn’t reduce rates or payments

Example:

Let's say you have three cards with balances of $3,000 at 25%, $8,000 at 22%, and $12,000 at 20%. You could use the avalanche method to save money by tackling the 25% card first, then the 22%, and finally the 20%. Or you could use the snowball method to pay off the $3,000 balance first for a quick win, followed by the $8,000, and then the $12,000.

Avalanche minimizes the total interest paid, while snowball provides faster psychological wins, even if it costs a bit more in interest.

2. Budget restructuring & self-funding

This is the most basic DIY approach: you aggressively cut expenses and divert all that extra income toward your debts. This is a powerful tactic that can be used in combination with other methods.

Pros:

- No new credit involved

- Can adjust repayment as needed

Cons:

- Progress can be slow unless you free up significant funds

- Lifestyle strain can cause burnout

- Diverts funds from savings, investments, or emergencies

Example:

A professional carrying $40,000 in credit card debt at 18% APR currently pays about $1,000 per month in minimum payments. At that rate, it would take roughly 62 months to fully pay off their debt. But, if after cutting expenses, they can redirect an extra $500 per month toward their debt ($1,500 total), it would reduce the repayment timeline to 35 months.

While this method effectively chips away at debt, progress is slow. And if additional cash flow can’t be freed up, it can strain savings or compromise liquidity.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

The risks of the DIY route for high-income borrowers

For professionals with strong income and significant high-rate debt, the DIY approach can be riskier and less effective than it seems. The same financial complexity that makes consolidation appealing is exactly what makes DIY so challenging.

Overcomplicating your financial picture

DIY often means juggling multiple accounts, each with different balances, APRs, and due dates. That complexity adds stress and increases the risk of late payments. For professionals already managing family finances, investments, and careers, that mental load can be costly.

Missed opportunity to save on interest

While some DIY methods like balance transfers offer a temporary reprieve, they don't permanently change your interest rates. High-income earners with strong credit are in a unique position to qualify for significantly lower rates on a personal loan.

A structured loan can save you thousands in interest, especially if you have significant debt.

Liquidity tradeoffs

Pulling from cash reserves or reducing contributions to savings may help you pay debt faster—but it also leaves you less prepared for a large tax bill, sudden expenses, or family obligations.

When DIY consolidation might work—and when it doesn’t

|

Situation |

DIY approach? |

Why or why not |

|---|---|---|

|

Less than $20K in debt, strong monthly cash flow |

Might work |

Small balances can be managed with strong budgets and sufficient income |

|

More than $20K in credit card or personal debt |

Not ideal |

Savings from lower APR consolidation loans are too significant to pass up |

|

More than $20K: Multiple cards with rates greater than 20% and combined balance of $20K or more |

Too costly |

A loan could dramatically lower interest and speed up repayment timeline |

|

Irregular income or cash flow pressure |

Risky |

Fixed-payment loan creates stability |

|

Want to avoid new credit |

Possible |

Effective, but progress is slower and less efficient; plus, may incur higher interest expense |

Other common debt consolidation methods

If you’re not ready to tackle DIY consolidation, there are other ways to consolidate debt by leveraging financing solutions. Two common options—using balance transfer credit cards or using your home equity—can work in certain situations.

1. Balance transfer credit cards

A balance transfer credit card allows you to move existing high-interest debt onto a new card with a 0% introductory APR. Most no-interest offers last between 12 and 21 months.

Pros:

- Pay zero interest during the promo window

- Potential to save hundreds or even thousands if you clear the debt quickly

Cons:

- Post-promo APRs often spike above 20%, which is higher than many personal loans

- Balance transfer fees (typically 3% to 5%) cut into your savings

- Credit limits may be too low for transferring balances higher than $15,000 to $20,000

Example:

If you have $20,000 in credit card balances and transfer them to a new card with a 3% transfer fee, you’ll pay $600 upfront. To pay the card off within your promotional period of 18 months and avoid a balance, you’d need to budget just over $1,144 per month. Otherwise, you’ll be subject to sky-high interest on whatever remains.

2. Cash-out refinance or HELOC

If you're a homeowner, you may have considered using your home's equity to pay off unsecured debt. A cash-out refinance replaces your existing mortgage with a new, larger one, allowing you to access the difference in cash. A Home Equity Line of Credit (HELOC) is a revolving line of credit you can draw from as needed.

Pros:

- Potential for lower interest rates than credit cards

- Can access a larger sum of money, depending on equity

Cons:

- Puts your home at risk—you could lose your home if you miss payments

- Closing costs and fees can be significant

- Extends your repayment horizon, sometimes by decades

Example:

If your home is valued at $600,000, and you have $400,000 remaining on your mortgage, you can use a HELOC or cash-out refinance to access a portion of your $200,000 equity (usually 80% to 85%) and pay off debt. You may qualify for a lower APR, but repayment is structured according to the mortgage schedule, which can spread payments over 15 to 30 years. This repayment approach requires careful planning to avoid putting your property at risk.

Why personal loans make sense for high earners

Predictability

A personal loan is a proven, reliable tool for debt consolidation. It comes with a fixed interest rate and a fixed monthly payment for the entire life of the loan. There are no surprises or sudden rate hikes, and your next payment falls on the same day every month.

Speed and simplicity

With an online lender like BHG, the application process is faster than what you might experience with traditional lenders, which can sometimes take weeks. BHG makes approval decisions quickly and can disperse the funds in your account in as little as a few business days.1 This speed and simplicity allow you to pay off your old debts and start fresh, fast.

Potential for major savings

A professional with strong credit can often replace high-interest credit card APRs of 24% or more with a loan rate as low as 10% to15%. This can translate into thousands of dollars in interest savings over the life of the loan. The money you save can then be redirected toward your investments, retirement, or other financial goals.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

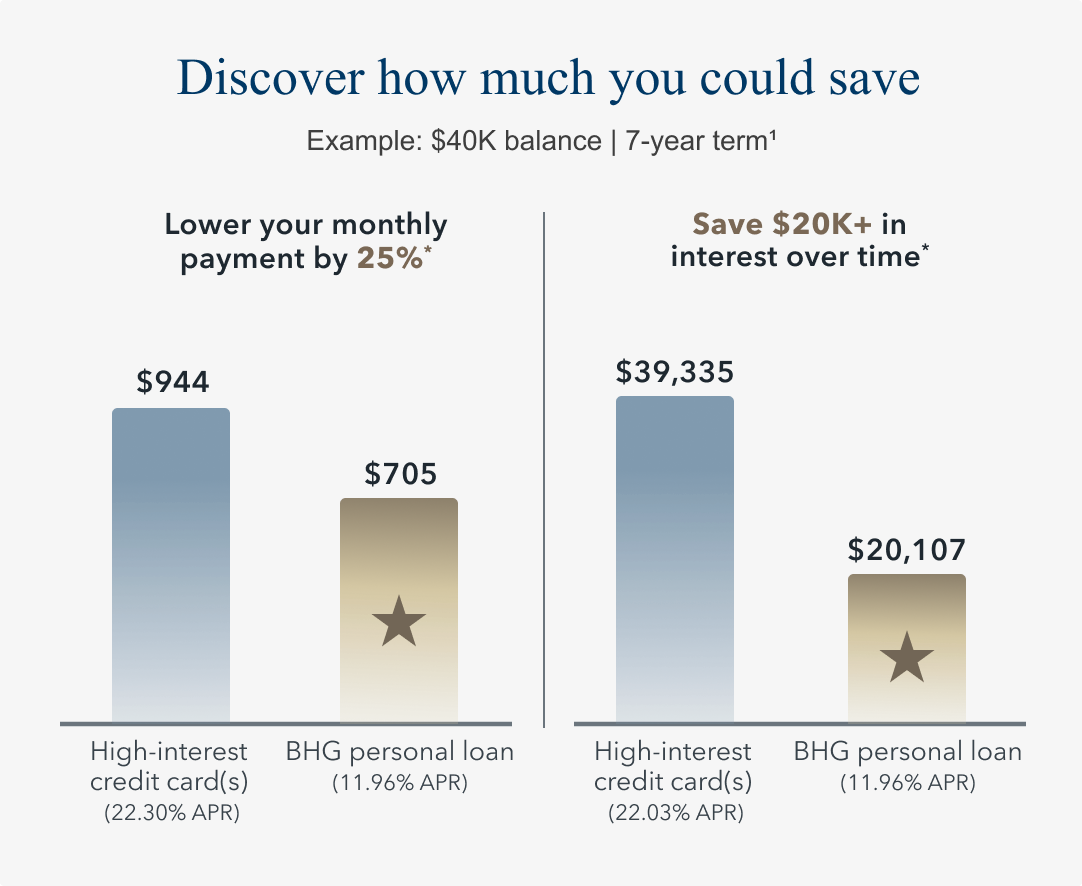

* Potential savings based off comparing repayment of a $40,000 balance over 7 years on both a credit card with a minimum monthly payment of $944 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $705 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

BHG personal loans are built for professionals

BHG Financial understands the unique needs of professionals. Our personal loans are specifically designed to address the challenges that come with significant debt and high income.

- Loan amounts up to $250,0002: Our loan amounts are larger than most competitors, enabling you to consolidate all of your debt at once.

- No collateral required: Our loans are unsecured, meaning you don't have to put your home or other assets on the line.

- Fixed terms up to 10 years2,3: Our industry-leading extended repayment terms make your monthly payments more affordable.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Final takeaway: DIY can work—but a loan may work better

DIY debt consolidation methods, balance transfer cards, and cash-out refinancing or HELOCs are all effective options for small balances and people with flexible repayment timelines. But they also require discipline and cash flow—and often don’t reduce interest rates enough to make a long-term impact.

Yes, you can consolidate debt without a loan. But for high earners with significant or high-interest balances, a personal loan offers simplicity, predictability, and meaningful savings. Remember, the goal isn't just to pay off debt; it's to do it in a way that preserves your liquidity and reduces your financial and mental burden.

Ready to see what’s possible? Use our quick and easy payment estimator to get your personalized loan offer in just seconds.1

Not all solutions, loan amounts, rates or terms are available in all states.

1 This is not a guaranteed offer of credit and is subject to credit approval.

2 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

3 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829