Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Credit Card Refinancing: How to Lower Your Interest and Pay Off Debt Faster

Table of Contents

- What is credit card refinancing?

- How can personal loans help refinance credit card debt?

- What are the benefits of using a personal loan for credit card refinancing?

- What are the alternatives to personal loans for refinancing credit card debt?

- Credit card refinancing FAQ

- How BHG can help you refinance credit cards

If you have several credit cards with different balances and interest rates, keeping track of them and making payments can feel overwhelming. Credit card refinancing—a term that can refer to several credit card debt consolidation methods—is a popular solution for simplifying your finances and potentially saving money.

Below, we’ll explain several ways to refinance credit card debt, including using a personal loan to consolidate it, so you can lower your interest rates and pay off debt faster.

Key Considerations

- There are several ways to refinance credit cards, including personal loans and balance transfer cards.

- Credit card refinancing generally makes sense if it allows you to get a better interest rate or lower monthly payments.

- If you have high-interest, variable-rate balances on multiple credit cards, a personal loan for credit card debt could reduce the amount of interest you pay over time, potentially helping you pay off your debt faster.

What is credit card refinancing?

Credit card refinancing is the process of opening a new credit card with better terms and using it to pay off your existing credit card debt and/or consolidate multiple credit card balances into one.

Those who refinance can potentially get a lower interest rate or a different payment schedule, which can help save on interest and/or pay off debt faster. A common way to refinance credit card debt is by transferring a credit card balance to another card with a 0% promotional annual percentage rate (APR).

However, refinancing debt with a balance transfer comes with some drawbacks, such as transfer fees and temporary promotional periods. To avoid the risk of fees and higher rates following the promotional period, some opt to refinance credit card debt using a personal loan, which comes with fixed interest rates.

How can personal loans help refinance credit card debt?

If you have multiple high-interest cards, a personal loan for credit card debt could help you manage it. A personal loan could also reduce the amount you pay in interest over time.

A personal loan for debt consolidation, sometimes called a debt consolidation loan, is a lump sum of money that you borrow from a lender to pay off some or all your existing debt. Instead of paying several creditors by their due dates, you’ll only pay one creditor each month: the personal loan lender.

You can usually borrow more money with a personal loan to refinance credit card debt than you could using most transfer cards. Plus, these loans come with fixed interest rates that may be lower than your existing variable credit card rates, potentially reducing the total interest paid over the life of the loan.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

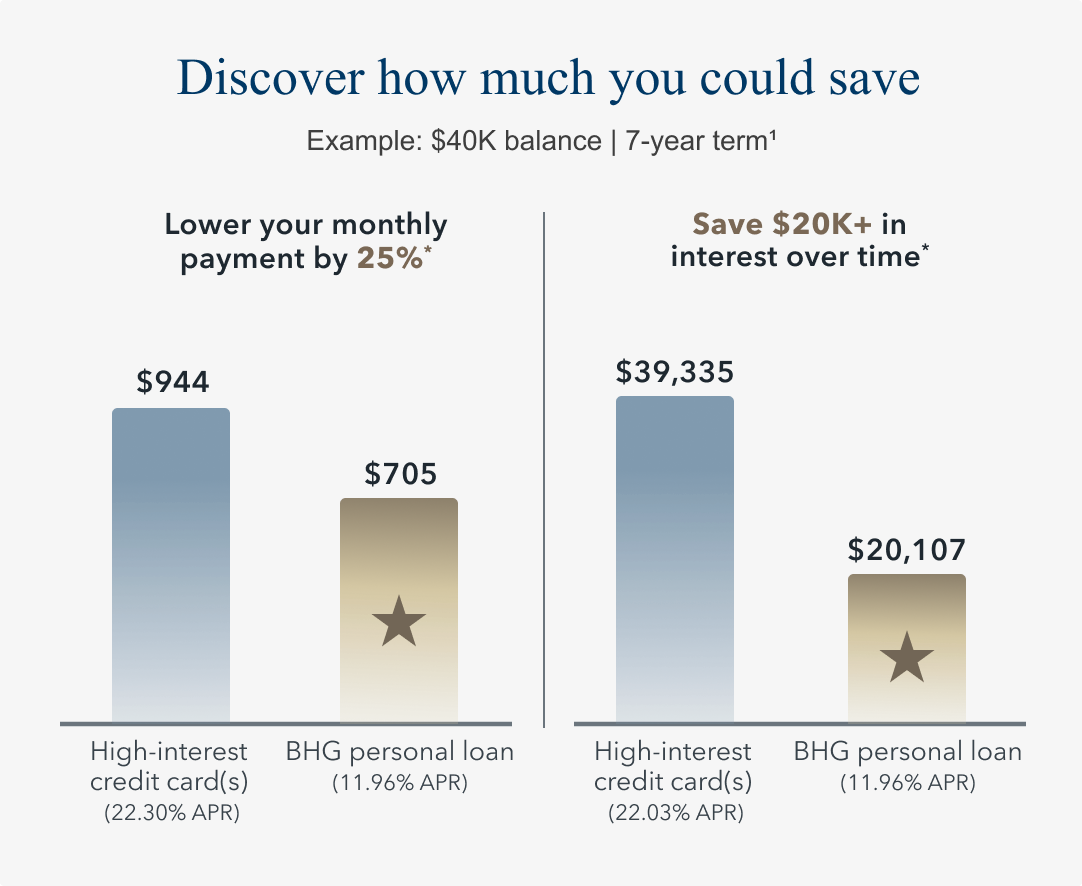

* Potential savings based off comparing repayment of a $40,000 balance over 7 years on both a credit card with a minimum monthly payment of $944 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $705 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

FYI: BHG Financial’s debt consolidation loans go as high as $250,0001 and have flexible terms up to 10 years,1,2 helping you refinance large amounts of credit card debt for a low monthly payment.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

What are the benefits of using a personal loan for credit card refinancing?

Choosing a personal loan for credit card debt consolidation can offer several advantages, including:

- Competitive interest rates: If you have good or excellent credit, personal loans can have lower rates than credit card interest rates. This means you’ll pay less interest over time, potentially helping you pay off debt faster.

- Potential to lower credit utilization ratio: Paying off high credit card balances with a personal loan can significantly lower your credit utilization ratio, which is the amount of credit you’re using compared to your total available credit. Your utilization ratio is a key factor for determining your credit score.

- Clear repayment timeline: Personal loans have a set repayment term so you know exactly when your debt will be paid off. Your interest rate is also fixed, meaning you’ll only need to manage one predictable monthly loan payment.

- Larger loan amounts: You can apply for a loan amount that’s enough to cover the balance of the credit cards you want to refinance. For example, BHG Financial offers loan amounts up to $250,000,1 which is higher than what some other lenders offer.

To truly maximize the benefits of a personal loan, it’s essential to partner with a trusted lender like BHG. With tailored consolidation loan options, competitive rates, and exceptional service, BHG makes it easy to manage your debt and stay in control of your financial goals.

What are the alternatives to personal loans for refinancing credit card debt?

While personal loans are a popular credit card refinancing option, there are alternatives to consider:

1. Balance transfer credit cards

You can combine existing credit card balances into one with a 0% or low introductory APR using a balance transfer card (just make sure you stay within the card’s transfer limit). Here, you’ll save money on interest while you work to pay off the balance in full. However, some credit card issuers charge a balance transfer fee ranging from 3% to 5%. And introductory periods have expiration dates—if you do not pay off the balance before the end of that period, you will be subject to the card’s standard variable interest rate.

2. Credit repayment strategies

The debt snowball and avalanche methods are two popular ways to attack credit card debt at a reasonable pace without exhausting your finances. Using the debt snowball method, you pay off your smallest debt first, regardless of the interest rate, before tackling larger balances. This strategy helps you build momentum with quick wins.

Paying off debt with the avalanche method involves prioritizing the debts with the highest interest rate, a strategy that helps you minimize the amount of interest paid over time, thus reducing the total cost of your debt.

Of course, any time you can pay more than the minimum card payment, you should. This allows you to allocate more funds to the principal balance, which helps you pay it down faster while also saving on interest. Review your monthly budget and identify areas where you can cut back spending, so you can use that money to make more progress toward becoming debt-free.

Credit card refinancing FAQ

Can refinancing credit card debt with a personal loan improve my credit score?

Yes, it can. When you use a personal loan for credit card debt consolidation, it can improve your credit utilization ratio. The amount of credit you use goes down as you pay off revolving debt like high card balances, which can lead to a better credit score. Also, maintaining a history of on-time payments on your loan can positively impact your score over time.

What is the difference between credit card refinancing and debt consolidation?

While the terms are often used interchangeably, credit card refinancing specifically refers to replacing your existing credit card debt with a new form of credit. Debt consolidation is a broader term that encompasses combining multiple debts into a single loan, which can include credit cards, personal loans, or other types of debt. Using a personal loan for credit card debt is one way to refinance debt using the debt consolidation method.

Are there risks associated with using personal loans for credit card refinancing?

While personal loans offer many benefits, it’s important to consider the potential drawbacks that could impact your overall cost. Interest rates are primarily determined by credit score, and even a small change in the rate you’re approved for could significantly increase or decrease the cost of the loan. Some lenders may also charge a one-time origination fee to take out a personal loan. If you decide to refinance your debt with a personal loan, stick to a budget so you don’t overspend and fall back into the same debt cycle.

How do I qualify for a personal loan to refinance my credit card debt?

To qualify for a personal loan, lenders will look for strong financial indicators, such as a good credit score and verifiable income and employment history. Consideration is also given to your debt-to-income ratio (DTI). These eligibility factors indicate that you have a history of responsible money management, which gives lenders confidence that you can afford to take on an additional loan.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

How BHG can help you refinance credit cards

At BHG Financial, we believe financing should fit seamlessly into your life and goals. That’s why we offer personal loans tailored to your needs, with amounts up to $250,0001 and flexible terms of up to 10 years.1,2 Consolidate your high-interest credit card debt with a BHG loan designed to help you move forward confidently.

Plus, you’ll enjoy dedicated, U.S.-based concierge service that works around your schedule—because your time is valuable. Ready to see what’s possible? Use our quick and easy payment estimator to get your personalized loan estimate in just seconds.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

Annual percentage rates (APRs) for personal loans range from 6.49% to 28.89%, with terms from 2 to 10 years.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

No application fees, commitment, or impact on personal credit to estimate your payment.

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829