Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Life After Debt Consolidation: 10 Smart Money Habits to Stay Out of High-Interest Credit Card Debt

Table of Contents

- 1. Understand the cost of “convenience” debt

- 2. Replace revolving debt with planning

- 3. Stop using credit cards as a cash flow tool

- 4. Automate the right things (not just minimum payments)

- 5. Audit lifestyle inflation

- 6. Create a personal “borrowing standard”

- 7. Monitor credit utilization

- 8. Plan for irregular income

- 9. Conduct a quarterly debt review

- 10. Remember: Debt consolidation is a reset, not a cure

- FAQs

- Check my rate

Carrying a credit card balance doesn't mean you're struggling. For many high earners, it's a byproduct of lifestyle timing, uneven cash flow, or sheer convenience rather than a lack of income.

A debt consolidation personal loan can reset the structure of your debt by lowering interest rates and simplifying repayment. But protecting that progress—whether you’re actively paying down your loan or continuing to use credit cards responsibly—requires the right financial habits.

These 10 strategies are designed for life after consolidation. They help you avoid high-interest credit card debt, strengthen liquidity, and turn a financial reset into lasting wealth.

1. Understand the real cost of “convenience” debt

Credit card interest is a wealth leak (not a necessity)

Carrying high-interest credit card debt is often framed as temporary or convenient, but the math tells a different story.

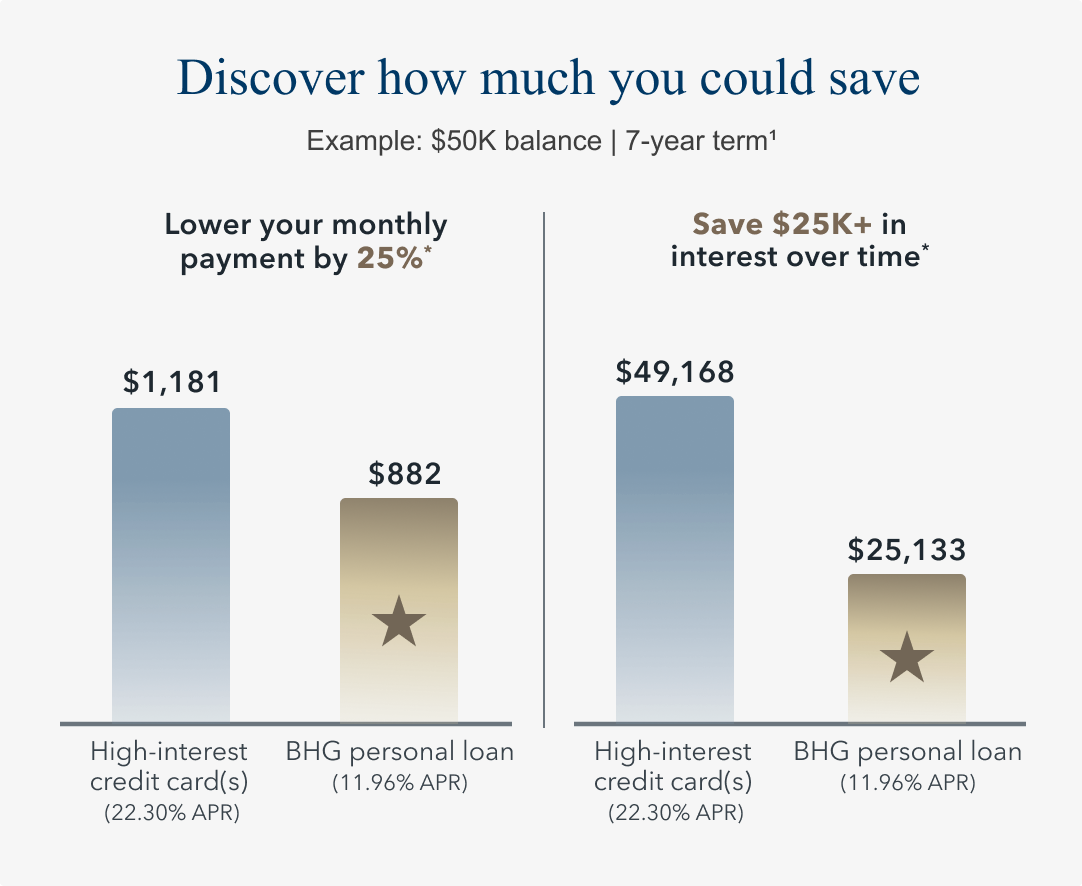

A $50,000 credit card balance at 22% APR can cost over $49,000 in interest alone—money that leaves your balance sheet without building anything. Structured through a personal loan at a significantly lower fixed rate, that same debt costs a fraction and comes with a clear payoff date.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $50,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,181 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $882 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

The monthly and total interest savings created by consolidation can now work for you by being added to an investment portfolio, funding a real estate or passive-income venture, or kept in a high-yield account to compound over time. Every month you allow a revolving balance to rebuild, you reverse that progress.

Action steps:

- Pull your credit card statements and calculate the total interest you paid over the last 12 months

- Assign that number a purpose: what wealth-building category would you redirect it to?

2. Replace revolving debt with structured liquidity planning

Build a “liquidity buffer,” in addition to a regular emergency fund

High earners often rely on cards because income doesn’t always align with expense timing. After consolidation, the goal is to prevent those timing gaps from pushing you back into revolving debt.

A recent BHG Financial Survey found that 73% of six-figure households feel they have the right amount—or more than they’ll need—saved for an emergency fund. Yet fewer people (56%) feel confident their savings could cover a major expense like a wedding, emergency surgery, or home repair.

That gap highlights the difference between emergency savings and liquidity. A liquidity buffer is built for real-world expenses that are irregular but predictable over time (tax estimates, home repairs, tuition timing, or medical costs). Aim for three to six months of fixed obligations in a dedicated, accessible account, separate from long-term investments. From there, layer in additional cash to absorb the unexpected without reaching for a credit card.

Action steps:

- Open a high-yield savings account specifically for liquidity and cash reserves

- Automate a transfer after each paycheck; target one month of fixed obligations within 90 days

3. Stop using credit cards as a cash flow tool

Credit cards should be a payment method, not a financing strategy

There's an important distinction between using a credit card to pay for something and using it to fund something. Transactional use, where the charge is covered by money already in your account, costs nothing and may earn perks and rewards. Borrowing use, where the balance carries month to month, reintroduces interest you’ve already worked to eliminate through consolidation.

High earners often justify balances while waiting on bonuses, commissions, or equity payouts. But if the cash isn’t available today, the purchase is still financed—often at premium rates that undermine your post-consolidation progress.

Action steps:

- Set a rule: any charge on a credit card must be covered by cash currently in your account

- If the cash isn't there, wait 72 hours before purchasing to avoid impulse or discretionary debt

Cleaning up your financial picture in advance gives you a competitive edge. By consolidating balances, you can lower your credit utilization ratio, which can improve your credit score over time and give you better borrowing power to pursue large investments or major life goals.

See financing options that support credit-smart decisions

Safely explore a personalized estimate in seconds

4. Automate the right things (not just minimum payments)

Automate loan payments, investments, and full statement balances

After consolidation, automation should reinforce discipline—not quietly enable old habits. Ideally, most high-interest cards are already paid off, allowing you to automate your personal loan payment and redirect cash flow toward savings and investments.

If you continue using credit cards for transactional purposes, automation should ensure balances are paid in full each statement cycle. When used to automate only minimum payments, it allows interest to rebuild debt. Instead, automate paying the full statement balance so you keep cards interest-free while preserving rewards and convenience. If needed, split payments into two payments per month to smooth cash flow

Pair this with automated transfers to savings or investments, so lifestyle spending doesn’t come before wealth-building.

Action steps:

- Review autopay settings on all recurring payments this week (credit cards, loans, subscriptions)

- Schedule at least one automated transfer to a wealth-building or liquidity account

5. Audit lifestyle inflation

High income doesn’t justify inefficient spending

Lifestyle upgrades happen gradually—a new subscription added, a ballooning dining budget, a bigger tuition payment. None of this is problematic—unless it’s funded with revolving debt you’ve already worked to eliminate.

When income rises, expenses tend to rise with it, and the gap between what you earn and what you keep can quietly narrow. A periodic audit helps surface where spending growth may be outpacing cash flow, forcing credit cards back into the picture.

Action steps:

- Identify three recurring expenses that increased over the past 12 months

- For each one, ask: Is this cash-flow funded, or reintroducing debt?

6. Create a personal “borrowing standard”

Define when debt is strategic—and when it isn’t

Not all debt is equal, and high earners benefit from having a clear internal framework for when borrowing makes sense.

Strategic debt has a defined purpose and measurable return—such as a debt consolidation personal loan that reduces your rate and simplifies repayment, or a real estate investment, or an asset acquisition. Non-strategic debt funds consumption: a vacation charged to a card with no repayment plan, or a discretionary purchase that exceeds current cash flow.

Getting clear on the distinction can help keep your spending intentional.

Action steps:

- Write two to three sentences defining your personal borrowing standard

- Before financing any purchase, ask whether it meets that standard—if it doesn't, don't finance it

7. Monitor credit utilization even with excellent credit

Keep utilization below 30% (ideally below 10%)

High earners often qualify for premium cards and high limits—but just because you can carry larger balances doesn’t mean you should. Debt consolidation can improve your credit score by lowering utilization. In fact, most BHG debt consolidation borrowers improve their FICO score by more than 30 points within a few months of funding.

Even if your score remains strong post-consolidation, racking up charges that increase utilization can signal risk to underwriters. If you anticipate applying for a mortgage or major financing in the next 12 to 24 months, keep your credit utilization low to protect your future borrowing power.

Action steps:

- Set calendar reminders to check balances mid-cycle, not just at statement close

- Pay down balances before the statement date if utilization is trending above 30%. Timing your credit card payments can help protect your score.

Most borrowers who consolidate debt through BHG improve their FICO score by 30 points or more within a few months of funding.*

8. Plan for irregular income (bonuses, commissions, equity events)

Don’t spend expected income before it arrives

Variable income introduces risk if it’s spent before it’s earned. Bonuses can change, and markets can fluctuate. Equity compensation, commissions, and year-end distributions all carry similar uncertainty. A simple allocation framework closes this gap and prevents balances from creeping back.

Action steps:

When a bonus or irregular payment arrives, consider a straightforward split:

- 50% toward liquidity reserves or paying off existing debt

- 30% into investments or retirement accounts

- 20% available for discretionary spending

9. Conduct a quarterly debt review

Treat personal finances like a balance sheet review

Businesses review their financial position every quarter; high earners should, too. A 30-minute quarterly check-in creates accountability and surfaces problems before they compound.

The questions don't need to be complicated. Ask:

- Are any balances revolving?

- Did lifestyle outpace cash flow?

- Is liquidity improving?

Action steps:

Block 30 minutes on your calendar at the end of each quarter

- Review credit card balances, liquidity account balance, any new recurring expenses, and progress toward financial goals

10. Remember: Debt consolidation is a reset, not a cure

Structure solves math, but habits solve patterns

A debt consolidation personal loan delivers real value: lower interest, one predictable payment, and a clear path forward. That’s measurable progress.

But the loan doesn't change how income flows or how expenses are funded. If old behaviors return, balances will follow. Long‑term success comes from disciplined liquidity management and strong financial habits after debt consolidation.

Ready to reset your debt structure? Explore your BHG Financial personal loan options designed for high-earning professionals and estimate your monthly payment in seconds—with no impact on your credit score.1

See what structured financing looks like

Get a personalized loan estimate in seconds †

† This is not a guaranteed offer of credit and is subject to credit approval.

FAQs about debt consolidation and staying debt-free

Will debt consolidation improve my credit score?

It can, yes. When you use a debt consolidation personal loan to pay off cards reduces credit utilization, which is one of the most heavily weighted factors in your score. You may also benefit from having a more diverse credit mix. The improvement isn't instant—give it one to two billing cycles to reflect—but for most borrowers with high utilization, the impact is positive. Most BHG debt consolidation borrowers improve their FICO score by more than 30 points within a few months of funding.

How do I avoid running up credit cards again after consolidation?

The most effective approach is structural: keep the cards open (closing them can hurt utilization and average account age), but remove them from your default payment methods for large or discretionary purchases. Pair that with a liquidity buffer so you're not turning to credit during timing gaps between income and expenses.

Is carrying a credit card balance ever strategic?

Rarely. Promotional 0% APR windows with a clear payoff plan can work for smaller balances with a clear payoff plan. But for most high earners, the cost of revolving debt at standard APRs far outweighs the convenience. If you’re borrowing for liquidity needs, a structured personal loan at a fixed rate is typically a more efficient solution than a revolving credit card balance.

What’s the best way to manage cash flow with high income but low liquidity?

Start by separating your operating cash from your investment accounts and long-term assets. A dedicated liquidity buffer—three to six months of fixed obligations in a high-yield account—gives you a cushion that doesn't require reaching for a credit card when expenses and income don't align. For larger one-time needs, a personal loan with a fixed rate and predictable payments can be more cost-effective than carrying a revolving balance and is a more flexible option than liquidating investments.

Check my rate

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Not all solutions, loan amounts, rates or terms are available in all states.

1 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

No application fees, commitment, or impact on personal credit to estimate your payment.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829