Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Loan to Consolidate Other Loans: What You Need to Know

Juggling different bills, due dates, and interest rates can feel like a never-ending cycle, leaving you stressed and overwhelmed. If you find yourself in this situation, a debt consolidation loan could be a helpful tool for regaining control of your finances.

Below, we'll explain how consolidating loans can help you manage and eliminate debt efficiently, setting you on the path to better financial balance.

Key Considerations

- Debt consolidation loans combine multiple debts into one manageable monthly payment, simplifying your finances.

- Consolidation loans can potentially lower your interest rate.

- Understand the relationship between consolidation and credit score to ensure your actions have a positive long-term effect on your score and financial wellbeing.

What is a loan to consolidate other loans?

A loan to consolidate other loans, also called a debt consolidation loan, is a type of personal loan that combines multiple existing debts with varying annual percentage rates (APRs) into one loan with a fixed monthly payment. This can be a smart move if you're looking to streamline your payments and potentially save money on interest, especially if your current debts have high interest rates.

How does loan consolidation work?

Loan consolidation is a fairly straightforward process that typically involves getting a personal loan for debt consolidation. Here, the lender gives you a lump sum of money to pay off your existing debts. Instead of paying multiple creditors each month, you’ll owe one larger amount to the new lender, which you will repay through fixed monthly payments over a set period of time.

While you can also use balance transfer cards to consolidate debt, they may not be the best option if you have a significant amount of debt. Balance transfers come with limits on the amount that can be transferred and a short, no-interest promotional period.

FYI: BHG Financial offers personal loans for debt consolidation with amounts up to $250,0001 and extended, flexible terms of up to 10 years.1,2

What types of debt can you consolidate?

All types of unsecured debt, as well as certain types of secured debt, are often eligible for debt consolidation. Generally, people opt to merge multiple loans into one when they have multiple types of high-interest debt and they are looking for easier debt management.

Here's a look at some of the types of debt you can consolidate:

- Education loans

- Other personal loans

- Credit cards with high balances

- Medical bills

- Business debt

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

What are the pros and cons of loan consolidation?

|

Pros of consolidation |

Cons of consolidation |

|---|---|

|

One monthly payment is easier to manage than multiple. |

If the new loan has a longer repayment term, you could pay more interest over time. |

|

Potentially lower rates than your existing debts, saving you money. |

Typically, only prime borrowers secure the lowest interest rates on consolidation loans. |

|

Fixed-rate loans offer consistent monthly payments, making budgeting easier. |

Consolidation loans may come with origination fees. |

|

Paying off high credit card balances can help improve your credit utilization ratio, and in turn, positively impact your credit score. |

Consolidation doesn’t resolve underlying financial problems. If you don’t adjust your spending habits, you could accumulate debt again. |

One of the biggest benefits of a debt consolidation loan is the simplicity it brings. Instead of remembering multiple due dates and minimum payments for various debts, you have just one predictable monthly payment. This can make budgeting much easier and reduce the likelihood of missing a payment, which can result in late fees and damage to your credit.

Consolidating generally only makes sense if you can secure a lower interest rate than your existing debts, allowing you to save interest over time and allocate a larger portion of your monthly payment to the principal.

Making on-time payments on your new loan can also improve your credit score over time by establishing a credit history and reducing your credit utilization ratio.

A solid budget and financial discipline can help ensure the impact of loan consolidation on your credit is positive. With a stronger credit score and better borrowing power, you could save money on other future purchases, like mortgages and cars, which may also have lower rates.

That said, it’s important to consider the costs of borrowing before taking out the loan to ensure it’s something you can afford. Debt consolidation loans may come with upfront fees, such as origination fees. These can add to the overall cost of the loan, so it's important to understand all charges before you commit.

How does BHG Financial support debt consolidation?

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

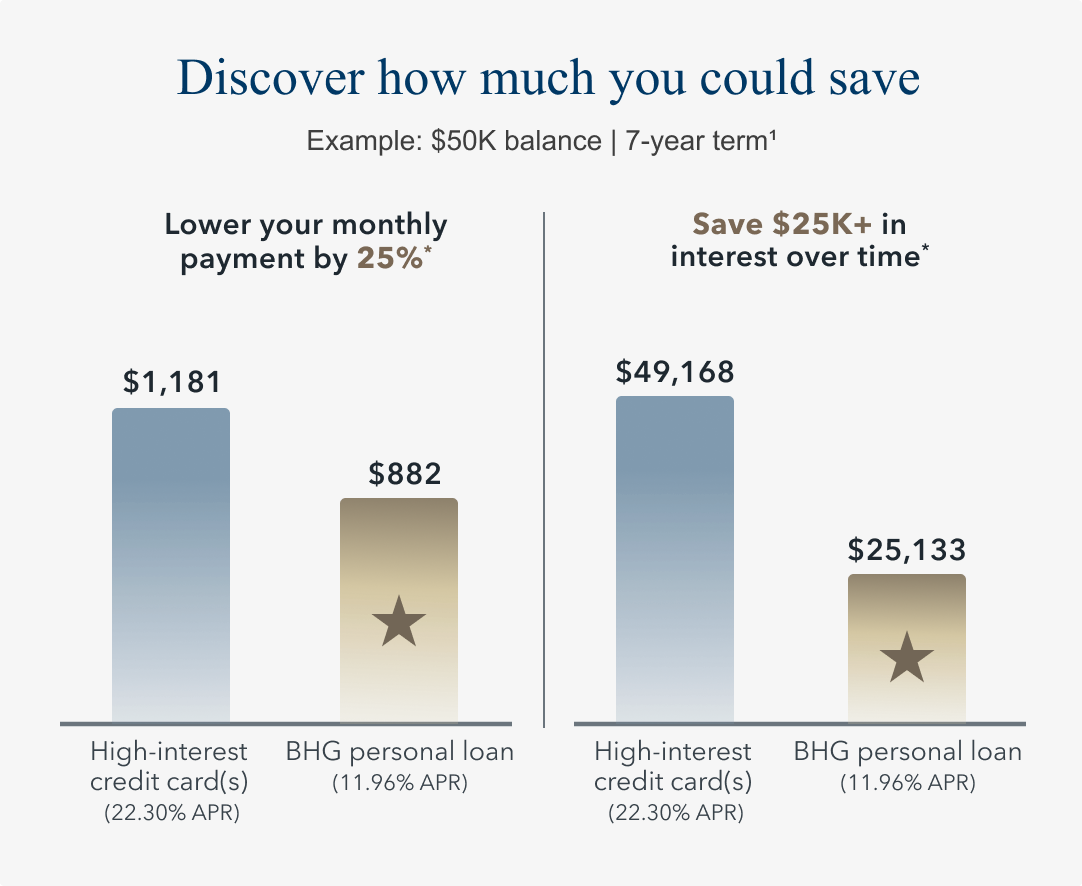

* Potential savings based off comparing repayment of a $50,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,181 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $882 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

BHG Financial understands the stress of managing multiple types of debt and selecting the right solution for your financing needs. That’s why we offer personal loans for debt consolidation specifically designed to consolidate large amounts of existing debt.

- Flexible repayment terms: BHG personal loans come with extended repayment terms of up to 10 years.1,2 Our loan experts will work with you to establish repayment terms that fit your budget and help keep payments manageable.

- Higher loan amounts: Most lenders offer personal loans for debt consolidation up to $100,000, but BHG can fund larger loan amounts up to $250,000.1

- Streamlined application process: Our application process is fast and efficient, allowing you to receive the funds you need quickly. You can prequalify online in minutes, and it will not impact your credit score.3

Our reputation speaks for itself. In fact, BHG’s tailored loan options and concierge loan service have earned us more than 3,900 5-star reviews on Trustpilot.

Ready to see how BHG can help you consolidate multiple loans? Use our quick and easy payment estimator to get your personalized loan estimate in just seconds.4

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Loan to consolidate other loans FAQ

Does a debt consolidation loan hurt your credit?

When you apply for a debt consolidation loan, lenders will initiate a hard inquiry, which can result in a small, temporary dip in your credit score. However, the long-term impact of loan consolidation on credit can be positive, provided you maintain disciplined financial habits. If you use the loan to pay off high-interest credit card debt, it can help lower your credit utilization ratio and potentially improve your credit score. Additionally, making consistent on-time payments on your new consolidation loan will establish a positive payment history, another key factor in determining your credit score.

How much can I save by consolidating my loans?

The amount you can save by consolidating your loans depends on several factors, including the interest rates of your new consolidation loan and the repayment term you choose. If your new loan has a significantly lower interest rate than your existing debt, you can save a considerable amount on interest charges over time. BHG allows you to prequalify and compare loan offers without affecting your credit score.3

Can I consolidate both personal and credit card debt?

Absolutely! A personal loan for debt consolidation is commonly used to merge various types of unsecured debts, like personal loans, credit card debts, and medical bills, into one payment.

What’s the difference between consolidation and refinancing?

While related, consolidation and refinancing are commonly used to potentially secure better rates or loan terms, they are not quite the same. Consolidation involves combining multiple existing debts into a single new loan, typically to simplify payments and potentially secure a lower interest rate. Refinancing typically involves taking out a new loan to replace a single existing loan—like when you refinance your mortgage to get a lower interest rate or a shorter loan term.

Is there a limit to how many loans I can combine?

You can generally combine as many eligible unsecured debts as you wish, as long as the total amount you need to borrow fits within the lender's loan limits and you qualify based on your creditworthiness and income. Lenders like BHG Financial offer high loan amounts up to $250,000,1 which can accommodate a significant number of existing debts for those with substantial income.

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

4 This is not a guaranteed offer of credit and is subject to credit approval.

No application fees, commitment, or impact on personal credit to estimate your payment.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829