Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

How Consolidating Debt Can Free Up Cash for Bigger Goals

If you’re a successful professional with high-interest credit card debt, hitting your financial milestones can feel harder than it should. Debt can stand in the way of retiring early, funding your child’s education, renovating your home, and/or traveling the world.

Here’s the good news: debt consolidation for high earners offers a way to simplify repayment, free up cash flow, and redirect your income toward what matters most. By using a personal loan for goals instead of watching money vanish into compounding interest, you create financial breathing room and a clear path forward.

Let’s dive deeper into the hidden cost of high-interest debt for six-figure earners and why debt consolidation can be a powerful tool for overcoming it.

Why income alone doesn’t guarantee financial flexibility

While earning six figures is a significant accomplishment, it doesn’t mean you’re immune to financial hurdles. In fact, Consumer Financial Protection Bureau’s Economic Well-Being report reveals that 12.1% of households with incomes above $125,000 struggled to pay bills in the last year.

So, what’s the reasoning behind this? Unexpected expenses, higher taxes, inflation, and the rising cost of living can all cause you to accumulate debt.

Additionally, you may have volatile or uneven income. Bonuses, commissions, stock or equity grants may come in or vest only once or a couple of times a year. So, while income may be high, the week-to-week or month-to-month liquidity can be strained, which can necessitate the use of credit cards or other consumer debt vehicles to pay expenses.

Interest and minimum payments drain progress

When you’re carrying balances on credit cards, high APRs can quietly drain your income. Many cards charge 18% to 25% interest—or more. If you’re only making minimum payments, compounding interest can stall your momentum. Instead of reducing what you owe, much of your payment goes toward servicing interest charges.

Over time, this cycle forces you to allocate money that could otherwise be directed toward building wealth or increase your savings rate.

What debt consolidation can do for your cash flow

Debt consolidation can have a positive effect on your monthly cash flow, freeing up your funds for the money moves that are important to you.

Lower monthly payments with a fixed rate

By consolidating multiple debts into one fixed-rate personal loan, you reduce the number of payments you need to make each month. This strategy helps simplify your finances and save on interest over time. By stretching repayment over a longer term, you can often lower the amount you owe monthly, giving you more breathing room in your budget.

Less interest = more liquidity

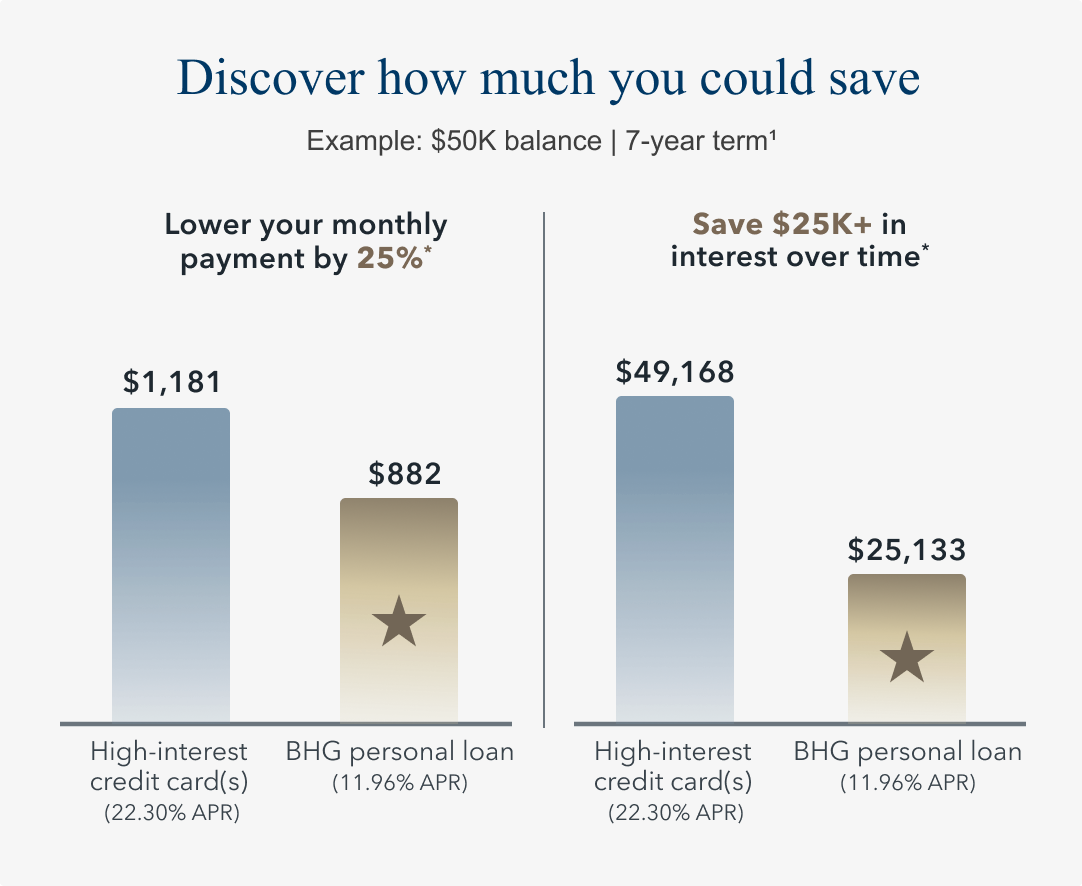

The less you spend on interest, the more funds you’ll have at your disposal. For example, let’s say you’re carrying $50,000 across several credit cards at 18% to 25% APR. By consolidating into a fixed-rate personal loan at a much lower rate, you could save hundreds per month and thousands of dollars in interest over the life of the loan.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $50,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,181 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $882 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

Freeing up cash flow for wealth-building moves

Imagine what you can do with the additional cash flow you gain through debt consolidation. You can boost your emergency fund, maximize your 401(k) contributions, and/or expand your real estate portfolio. All these strategies may improve your long-term wealth.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Why high earners choose BHG’s personal loan for debt consolidation

While there are many debt consolidation loans on the market, BHG Financial's personal loan for debt consolidation stands out. Here’s why:

Tailored for professionals with strong credit

Our debt consolidation loans are specifically designed for professionals with strong credit and professional stability. We understand that you may have a more complex financial situation with unique needs. Our team of U.S.-based loan experts can help you choose a financing solution that aligns with your circumstances and financial goals.

Larger loan amounts and longer terms

High earners often carry higher balances. Where other lenders cap borrowing amounts to $50,000 or $100,000, BHG offers loans up to $250,0001 with terms up to 10 years.1,2 This is ideal if you’d like to consolidate large debt balances without putting strain on your monthly budget.

Speed and privacy matter to high performers

BHG Financial understands that you lead a busy life, in and out of the office. That’s why we allow you to prequalify online using our secure systems without impacting your credit score.3

If you decide to formally apply, you may get approved in as few as 24 hours and receive funding in as little as five days.4

Turning cash flow into opportunity

Reallocating money toward bigger ambitions

Freeing up cash isn’t just about day-to-day comfort—it’s about creating the capacity to fund bigger life moves. Whether you want to build long-term wealth, pursue an entrepreneurial venture, cover your child’s college, retire early, or anything in between, debt consolidation can help you get there.

Using momentum to build net worth

Paying off debt strategically can also boost your credit score by lowering utilization and strengthening your payment history. What’s more, better credit may unlock better borrowing options in the future.

A smarter way to grow, not just a way out of debt

High earners are increasingly using consolidation as a solution to get ahead rather than “catch up.” Not only can you leverage it to pay off high-interest debt, you can restructure your finances in a way that helps you manage money and position yourself for growth.

Is debt consolidation right for you?

Just like any other financial tool, you should consider debt consolidation carefully. Before you move forward with this strategy, make sure you’re a good candidate for it.

Questions to ask before you consolidate

If you answer “yes” to any or all these questions, debt consolidation may be right for you:

- Do you have multiple high-interest debts with APRs greater than 20%?

- Do you have a “good” or “excellent” credit score?

- Are monthly payments limiting your ability to invest or save?

- Would one lower, fixed payment reduce stress and create more breathing room?

- Are you looking for a streamlined, structured approach to paying off debt?

- Are you ready to take control of your spending habits?

When BHG’s loan makes the most sense

A BHG debt consolidation loan can be a smart move if you’re juggling significant high-rate debt from credit cards and other loans, and want a structured, predictable way to pay it off. BHG’s personal loans for debt consolidation have flexible terms that help create financial flexibility and improve liquidity.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Final thoughts: Free up cash, fund what matters most

Consolidating debt as a high earner isn’t about cutting back—it’s about positioning your finances for growth. Leverage it to build a stable financial foundation that allows you to enjoy your current lifestyle while working towards the future of your dreams.

Ready to make your income work harder for you? See what you qualify for with a BHG personal loan—no impact to your credit score.3

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

4 This is not a guaranteed offer of credit and is subject to credit approval.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829