Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Should You Dip Into Savings or Use a Loan? How to Decide

Every now and then, you might need the funds to consolidate debt, pay a medical bill, or cover another planned or unexpected expense. While you may pull cash from your savings, you can also take out a personal loan.

The ideal choice depends on a number of factors, including your financial situation, goals, and personal preferences. Let’s dive deeper into both options so you can make the most informed decision for your unique situation.

The reality of savings—even for high earners

Being a high earner doesn’t necessarily mean you have a hefty savings account in place. In fact, only 25% of those earning $100,000 feel they have enough savings to cover three months of expenses, according to a recent Economic Well-Being Report from the Federal Reserve.

A survey of BHG Financial customers revealed that 68% of those earning $100,000 or more have $10,000 or less available in their checking and savings accounts. So, what’s the reason behind the lower savings and lack of financial confidence for high earners?

Even if you make six figures, financial stress still exists; it just looks different. There’s pressure to support others (parents, kids, etc.) while also juggling higher everyday expenses like mortgages, school tuition, and lifestyles. Many higher earners are low on liquidity, making it harder for them to finance unexpected expenses.

When tapping savings makes sense

In some cases, it’s a good idea to leverage the savings you’ve worked so hard to collect. By doing so, you can:

Avoid borrowing cost

The general rule of thumb is to save at least three-to-six months of living expenses reserved for emergencies—and even more if you’re an entrepreneur, self-employed, or have an unpredictable income stream.

If you’re confident your expenses won’t deplete this amount, you could use your savings to cover it. Otherwise, it may be better to keep your savings intact and find alternative financing options.

Enjoy immediate, no-cost access

When you use your savings for an expense, you avoid the additional costs that usually come with loans and credit cards, such as interest and fees. If you have a small or one-off expense that won’t derail your financial cushion, paying for it with your savings could save you thousands of dollars in the long run.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

When a loan is the smarter move

“A loan can be a useful tool, but you must know when to deploy that tool. A hammer is a useful tool, but I don’t use it to replace a light bulb, I prefer a ladder,” says Den Murley, certified financial planner at Belonging Wealth Management.

Here are a few ways to decide if a personal loan is the better option for you compared to using savings or credit cards:

Preserve long-term reserves

If you opt for a personal loan, you won’t have to deplete your cash reserves to fund an expense. Plus, as a borrower with good credit, you may be able to get a personal loan with a competitive interest rate.

Balanced cash flow

One benefit of a personal loan is the predictable repayment schedule. Most unsecured loans have fixed monthly payments that help you stick to a budget. If you have to pay for something with financing, a fixed-rate installment loan may feel safer than other options like credit cards where the APR and repayment schedule can vary.

Lower interest than credit cards

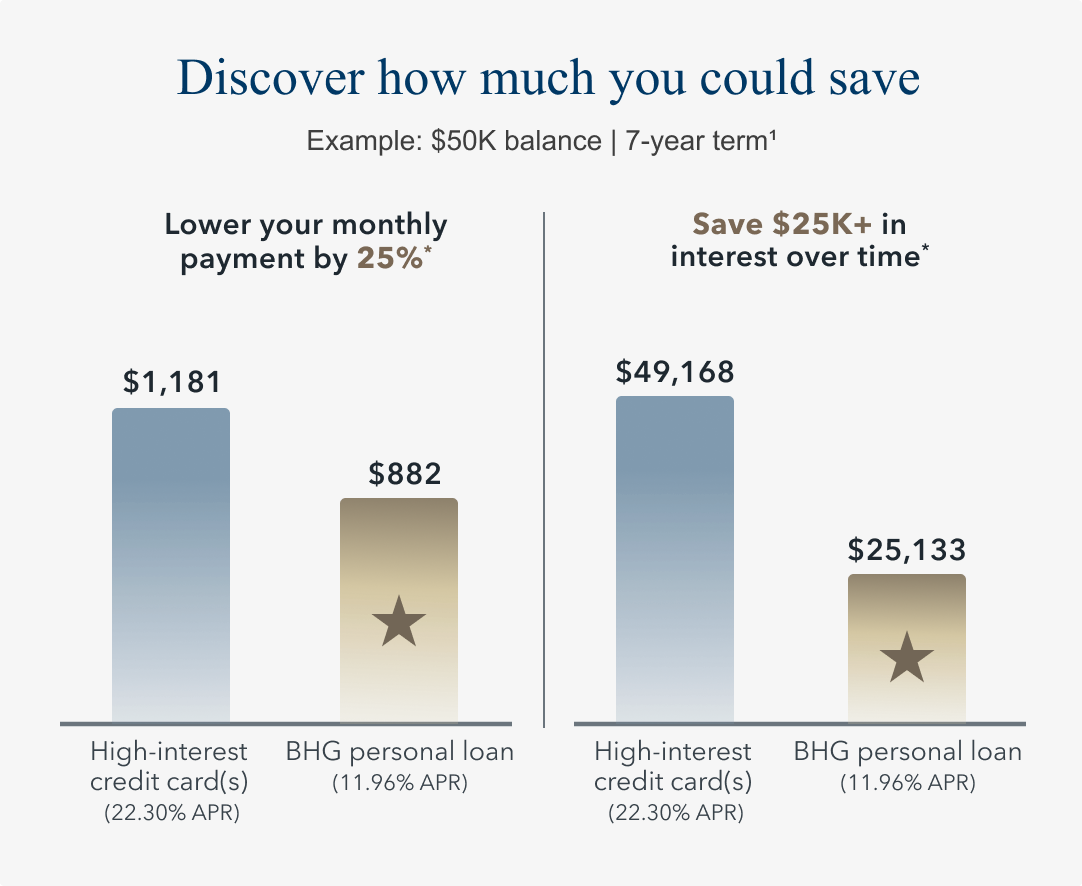

Personal loan APRs tend to be lower than credit cards. The average credit card APR is just under 22%, according to the Federal Reserve Bank of St. Louis, and the average personal loan APR for those with prime credit is about 11% to 15%. A lower, fixed-rate loan saves you a great deal of interest, helping you keep your savings in good shape.

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $50,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,181 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $882 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

FYI: BHG Financial’s personal loans for debt consolidation are a great option for those struggling with high-interest credit card debt. Consolidate multiple debts into a new loan with better terms, including a fixed rate, a flexible repayment period, and one low monthly payment.

The data-driven decision framework for choosing

Follow these steps to help you determine whether you should tap into your savings or take out a loan instead.

1. Evaluate your buffer

Audit the amount in your savings accounts, as well as your current and upcoming financial obligations, to determine whether you can afford to withdraw some or all of it.

If dipping into savings would risk your emergency fund, a personal loan may be a better way to fund your expenses and maintain your savings.

2. Calculate real cost

Compare a loan’s interest and fees to the cost of not having enough cash on hand or a financial cushion. Prequalifying can help you see if the loan terms would be favorable. If the benefits outweigh the risks, it may be worth considering.

3. Prioritize peace of mind

Consider how each option will affect your stress levels. For some, using savings feels safer than the multi-year commitment required to repay a loan. For others, a personal loan is less stressful for depleting cash reserves. Choose the approach that feels right for you.

“Whatever option you choose shouldn’t keep you up at night,” says Murley.

4. Review your goals

Lastly, think about what you hope to achieve financially.

“Ask yourself, ‘Will future me appreciate what current me is doing?’ This is a favorite question I like to ask myself. It’s important to balance your current self with your future self before you make any financial decision like pulling from savings or taking out a loan,” says Murley.

Why BHG Financial’s personal loan works for high earners

If you’re a professional or business owner with a high income, the BHG unsecured personal loan should be on your radar. You can borrow up to $250,0001 with no collateral required, so your savings and investments remain untouched. Plus, extended repayment terms up to 10 years1,2 help keep your monthly payments low and protect your cash flow.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Final takeaway: Choose based on context, not cost alone

Using your savings makes the most sense for manageable, one-off costs. When larger, strategic, or unexpected expenses pop up, a personal loan is likely your best bet. You’ll protect your liquidity and ensure financial flexibility while empowering yourself to live fully without compromise.

Ready to explore the possibilities? BHG can help. See your personalized offers in just seconds without any impact to your credit.3,4

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 This is not a guaranteed offer of credit and is subject to credit approval.

4 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

No application fees, commitment, or impact on personal credit to estimate your payment.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829