Personal loans

Customized financing to consolidate high-interest debt and unlock financial flexibility.

About BHG

Programs

Is It Smart to Refinance Your Personal Loan and Consolidate Credit Cards at the Same Time?

Managing multiple debts isn’t just stressful—it can also be expensive. If you’re carrying both a personal loan and several credit card balances, you might think you have to prioritize one over the other to get back on track.

The good news? You don’t have to choose between refinancing an existing personal loan or consolidating high-interest credit cards. When done strategically, refinancing and consolidating together can simplify your finances, lower your monthly payments, and free up cash flow.

Key takeaway

Refinancing a loan and consolidating credit cards are two distinct actions, but they can be combined into a single, streamlined solution: a personal loan for debt consolidation. For borrowers with strong credit and stable income, bundling both into one loan can make sense—but the timing, loan structure, and lender offerings must all align with your needs.

Why high earners reevaluate debt

Managing complexity, not just cost

High-income professionals often juggle more than one type of debt. Between personal loans, multiple credit cards, and ongoing household expenses, keeping track of it all can be challenging.

For many, the real goal isn’t just lowering interest—it’s having predictable payments and clearer cash flow. Imagine turning five different due dates into one fixed payment you can plan around. That simplicity can be just as valuable as the savings.

Timing is key

Deciding when to act is critical. Life milestones—like welcoming a new child, changing careers, or making a major investment—can all make it the right moment to revisit your debt strategy.

But so can the economy. When the prime rate is high and fluctuating, variable-rate debt like credit cards can feel unstable. Moving to a fixed-rate personal loan brings more certainty and ensures predictability.

- Rising APRs: With today’s elevated and unpredictable prime rate, carrying variable-rate credit card balances is riskier than ever.

- Life transitions: Buying a home or sending a child to college can justify restructuring debt to free up liquidity.

- Market windows: If personal loan rates dip or your credit profile has improved since your last loan, refinancing and consolidating at the same time may make sense.

What does it mean to refinance and consolidate together?

Refinancing a personal loan

Refinancing a loan means replacing your current loan with a new one—ideally at a lower rate or longer term. Why would you do this?

- It frees up monthly cash flow by reducing your required payment.

- It lessens total interest paid over the life of the loan if you secure a lower rate and keep the term the same or shorter.

Consolidating credit cards

Consolidating credit cards means rolling multiple high-interest balances into one fixed-rate personal loan. This move:

- Simplifies payments by giving you only one bill to track.

- May lower monthly debt payments, particularly if your current credit card APRs are very high (which is increasingly common).

Doing both in one move

When you refinance and consolidate at the same time, you can use the new, larger personal loan to pay off multiple high-interest credit cards and any existing personal loans.

This strategy allows you to reset your entire debt picture in one go, combining multiple debts into a single, predictable payment.

FYI:

This approach works best when you qualify for a lender offering large loan amounts. For example, BHG Financial provides personal loans for debt consolidation up to $250,000,1 allowing qualified borrowers to consolidate substantial debts and still have funds left for other goals—whether that’s a major purchase or a financial cushion.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Pros of doing both at once

1. Simplified debt management

Instead of tracking multiple loans and cards, you’ll have just one fixed payment. This makes budgeting easier, reduces the likelihood of missed payments, and allows you to automate repayments.

2. Potential to reduce interest

Credit card APRs average around 24%. However, a well-qualified borrower may be able to lock in a fixed-rate personal loan at 10% to 15%. Refinancing your existing loan while consolidating credit card balances could result in significant monthly savings.

3. Liquidity and breathing room

Extending the term of your new loan may lower your monthly payment—even if the interest rate stays the same. That breathing room can make a big difference when handling tax season, capitalizing on an investment opportunity, or preparing for emergencies.

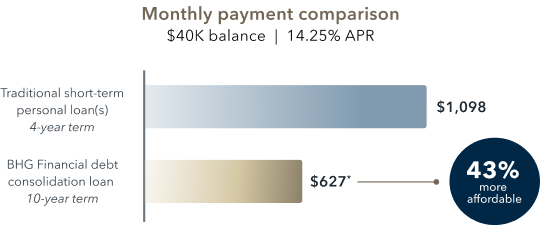

The image below shows how extending your loan terms can reduce payments:

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* BHG monthly payment based on BHG’s minimum available APR for a 10-year term, which is 14.25% as of 05/13/26 and includes an origination fee. Your actual loan size, loan term, and monthly payment amount may vary based on your individual credit profile and other information provided in your loan application. Terms subject to credit approval.

FYI: BHG personal loans come with industry-leading repayment timelines—choose terms up to 10 years1,2 and unlock affordable fixed monthly payments.

4. One credit inquiry, one application

With the right lender, you won’t need separate applications. You can refinance your personal loan and consolidate credit cards in one step, which helps reduce paperwork. Plus, there is no impact on your credit for estimating a payment.4

Potential cons and cautions

1. Extending the debt timeline

A lower monthly payment often comes with a longer repayment term—but that’s not always a bad thing. The key is finding the right balance between immediate relief and long-term cost. Extending the term can create valuable breathing room for other financial goals, especially if the interest rate improves.

When consolidating, assess your budget to see what’s sustainable month to month, then aim for a repayment plan that reduces pressure now without adding unnecessary interest later.

2. Risk of “reloading” credit cards

Consolidation works best when paired with a disciplined repayment plan. After using a personal loan to pay off your credit card balances, you'll have accounts with a zero balance. If you don’t address the habits behind the original credit card debt, those balances may build back up, leaving you with the new personal loan and new high-interest credit card debt.

3. Qualification matters

Lenders reserve the best rates for borrowers with strong credit—usually a FICO score of 720 or higher. If your score has dipped or your income doesn’t support a larger loan, you may still qualify, but the terms may not be as favorable.

Read more:

The Best Personal Loans for Prime Credit Borrowers with Debt | BHG Financial

When it’s a smart move

|

Scenario |

Recommendation |

|---|---|

|

Strong credit score (700+) and solid income |

Consolidation may be a smart option for securing a low, fixed APR |

|

High monthly payments straining liquidity |

Consolidation will create predictable payments for better financial planning |

|

Planning for additional large expenses |

Consolidation may free up cash flow |

|

Poor credit or unstable income |

Proceed cautiously; compare APR and terms first |

|

Already close to paying off personal loan |

Better to finish current loan, then consolidate separately |

Why BHG personal loans are ideal for this strategy

As a high-earning professional with a strong credit profile, you require a partner who understands the complexity of your finances and offers solutions tailored to your success. BHG Financial specializes in large, flexible, unsecured financing, which is perfectly suited for refinancing and consolidation.

- Largest unsecured loans: We offer loan amounts up to $250,0001, easily covering a sizable existing loan and multiple credit card balances.

- Predictable payments: You get fixed interest rates for the life of the loan—no surprises.

- Flexible terms: Repayment terms are available up to 10 years,1,2 allowing you to choose a monthly payment that optimizes your cash flow.

- Designed for success: Our loans are tailored to professionals with strong credit profiles and proven income.

- Speed and efficiency: We offer fast approvals—in as little as 24 hours3—so you can take back control quickly.

Example: A physician carrying a $50,000 personal loan at 12% and $25,000 in credit card debt at 24% could roll both into one BHG personal loan at a lower blended rate and longer term. The result: one predictable monthly payment, potentially hundreds in monthly savings, and freed-up cash for other priorities.

|

|

Balance |

APR |

Monthly payment |

Interest paid over 7 years1 |

|---|---|---|---|---|

|

High-interest credit card(s) |

$50,000 |

22.30% |

$1,181 |

$49,168 |

|

$50,000 |

11.96% |

$882 |

$24,052 |

|

|

|

|

Estimated savings on credit card interest with BHG |

$25,116* |

Advertised rates are subject to change without notice.

Monthly payment is a representative example and for illustrative purposes only.

* Potential savings based off comparing repayment of a $50,000 balance over 7 years on both a credit card with a minimum monthly payment of $1,181 and APR of 22.30% (average consumer credit card APR per The Federal Reserve as of 04/01/26), with the assumption no additional draws on the line are made during this time; and a BHG Personal Loan with a minimum monthly payment of $882 and minimum available APR for a 7-year term, which is 11.96% as of 05/05/26 and includes an origination fee.

See your offer † real fast

Just a few easy steps to get prequalified!

† This is not a guaranteed offer of credit and is subject to credit approval.

Final takeaway: Bundling may boost efficiency

Refinancing and consolidating at the same time isn’t for everyone, but for high earners with strong credit, it can be a powerful strategy. If your goal is to make fewer payments, get lower rates, and have more control over your financial future, bundling could be the smartest next step.

And with lenders like BHG Financial specializing in large, unsecured fixed-rate personal loans tailored to professionals, you don’t have to navigate the process alone.

Ready to see what’s possible? Use our quick and easy payment estimator to get your personalized loan offer in just seconds.3

Not all solutions, loan amounts, rates or terms are available in all states.

1 Terms subject to credit approval upon completion of an application. Loan sizes, interest rates, and loan terms vary based on the applicant's credit profile. Not all applicants will qualify for the lowest rate.

2 Personal Loan Repayment Example: A $60,000 personal loan with a 7-year term and an APR of 17.06% would require 84 monthly payments of $1,191.38.

3 This is not a guaranteed offer of credit and is subject to credit approval.

4 There is no impact on your credit for applying. For personal loans, a complete credit history, which will appear as an inquiry on your credit report, will be performed upon acceptance and funding of the loan and may impact your credit.

Consumer loans funded by Pinnacle Bank, a Tennessee bank, or County Bank. Equal Housing Lenders. ![]()

For California Residents: Personal loans made or arranged pursuant to a California Financing Law license - Number 603G493.

Bankers Healthcare Group, LLC d/b/a BHG Financial NMLS ID# 2040829